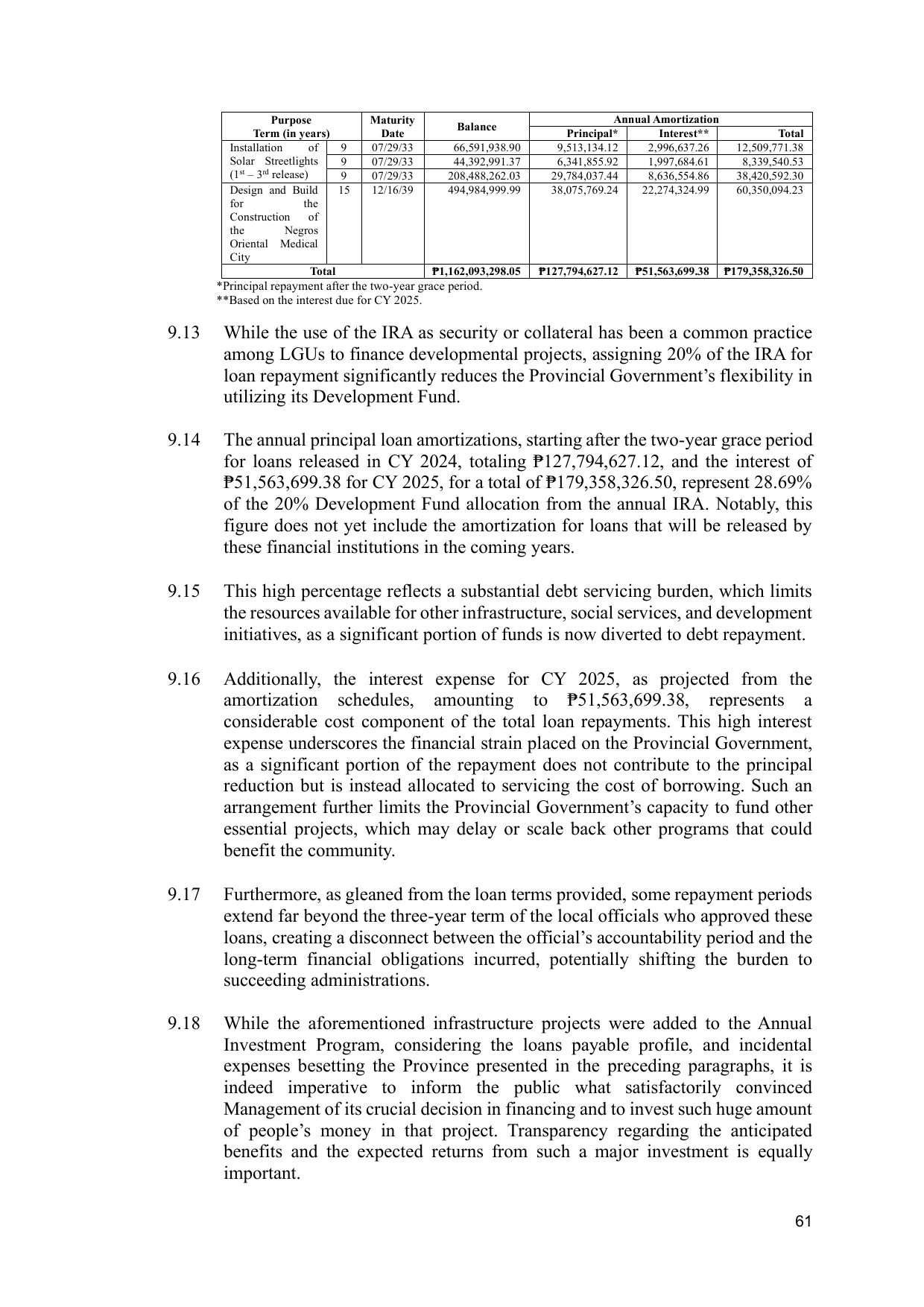

Purpose Maturity Annual Amortization

Balance

Term (in years) Date Principal* Interest** Total

Installation of 9 07/29/33 66,591,938.90 9,513,134.12 2,996,637.26 12,509,771.38

Solar Streetlights 9 07/29/33 44,392,991.37 6,341,855.92 1,997,684.61 8,339,540.53

(1st – 3rd release) 9 07/29/33 208,488,262.03 29,784,037.44 8,636,554.86 38,420,592.30

Design and Build 15 12/16/39 494,984,999.99 38,075,769.24 22,274,324.99 60,350,094.23

for the

Construction of

the Negros

Oriental Medical

City

Total ₱1,162,093,298.05 ₱127,794,627.12 ₱51,563,699.38 ₱179,358,326.50

*Principal repayment after the two-year grace period.

**Based on the interest due for CY 2025.

9.13 While the use of the IRA as security or collateral has been a common practice

among LGUs to finance developmental projects, assigning 20% of the IRA for

loan repayment significantly reduces the Provincial Government’s flexibility in

utilizing its Development Fund.

9.14 The annual principal loan amortizations, starting after the two-year grace period

for loans released in CY 2024, totaling ₱127,794,627.12, and the interest of

₱51,563,699.38 for CY 2025, for a total of ₱179,358,326.50, represent 28.69%

of the 20% Development Fund allocation from the annual IRA. Notably, this

figure does not yet include the amortization for loans that will be released by

these financial institutions in the coming years.

9.15 This high percentage reflects a substantial debt servicing burden, which limits

the resources available for other infrastructure, social services, and development

initiatives, as a significant portion of funds is now diverted to debt repayment.

9.16 Additionally, the interest expense for CY 2025, as projected from the

amortization schedules, amounting to ₱51,563,699.38, represents a

considerable cost component of the total loan repayments. This high interest

expense underscores the financial strain placed on the Provincial Government,

as a significant portion of the repayment does not contribute to the principal

reduction but is instead allocated to servicing the cost of borrowing. Such an

arrangement further limits the Provincial Government’s capacity to fund other

essential projects, which may delay or scale back other programs that could

benefit the community.

9.17 Furthermore, as gleaned from the loan terms provided, some repayment periods

extend far beyond the three-year term of the local officials who approved these

loans, creating a disconnect between the official’s accountability period and the

long-term financial obligations incurred, potentially shifting the burden to

succeeding administrations.

9.18 While the aforementioned infrastructure projects were added to the Annual

Investment Program, considering the loans payable profile, and incidental

expenses besetting the Province presented in the preceding paragraphs, it is

indeed imperative to inform the public what satisfactorily convinced

Management of its crucial decision in financing and to invest such huge amount

of people’s money in that project. Transparency regarding the anticipated

benefits and the expected returns from such a major investment is equally

important.

61