Estimated

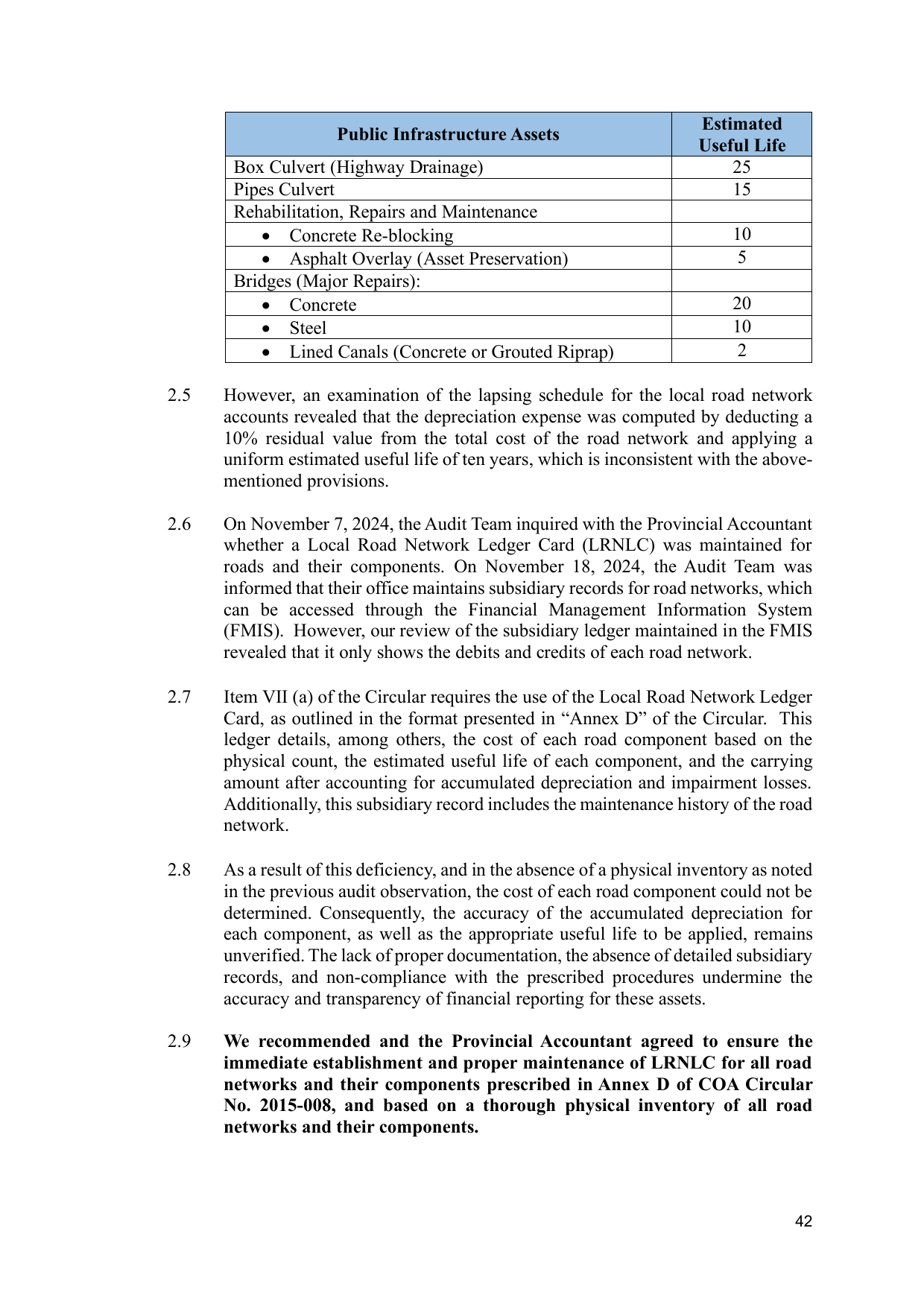

Public Infrastructure Assets

Useful Life

Box Culvert (Highway Drainage) 25

Pipes Culvert 15

Rehabilitation, Repairs and Maintenance

• Concrete Re-blocking 10

• Asphalt Overlay (Asset Preservation) 5

Bridges (Major Repairs):

• Concrete 20

• Steel 10

• Lined Canals (Concrete or Grouted Riprap) 2

2.5 However, an examination of the lapsing schedule for the local road network

accounts revealed that the depreciation expense was computed by deducting a

10% residual value from the total cost of the road network and applying a

uniform estimated useful life of ten years, which is inconsistent with the above-

mentioned provisions.

2.6 On November 7, 2024, the Audit Team inquired with the Provincial Accountant

whether a Local Road Network Ledger Card (LRNLC) was maintained for

roads and their components. On November 18, 2024, the Audit Team was

informed that their office maintains subsidiary records for road networks, which

can be accessed through the Financial Management Information System

(FMIS). However, our review of the subsidiary ledger maintained in the FMIS

revealed that it only shows the debits and credits of each road network.

2.7 Item VII (a) of the Circular requires the use of the Local Road Network Ledger

Card, as outlined in the format presented in “Annex D” of the Circular. This

ledger details, among others, the cost of each road component based on the

physical count, the estimated useful life of each component, and the carrying

amount after accounting for accumulated depreciation and impairment losses.

Additionally, this subsidiary record includes the maintenance history of the road

network.

2.8 As a result of this deficiency, and in the absence of a physical inventory as noted

in the previous audit observation, the cost of each road component could not be

determined. Consequently, the accuracy of the accumulated depreciation for

each component, as well as the appropriate useful life to be applied, remains

unverified. The lack of proper documentation, the absence of detailed subsidiary

records, and non-compliance with the prescribed procedures undermine the

accuracy and transparency of financial reporting for these assets.

2.9 We recommended and the Provincial Accountant agreed to ensure the

immediate establishment and proper maintenance of LRNLC for all road

networks and their components prescribed in Annex D of COA Circular

No. 2015-008, and based on a thorough physical inventory of all road

networks and their components.

42