2.10 We further recommended and the Provincial Accountant agreed that,

following the physical inventory and reconciliation of records, depreciation

expenses be recomputed separately for each road component and any

necessary adjustments be reflected in the books of accounts to ensure

compliance with IPSAS 17 and COA Circular No. 2015-008.

Unreliable Inventory Balance Due to Incomplete Records and Dormant Accounts

3. The reliability of the inventory accounts totaling ₱557,966,849.17 could not be

ascertained due to the absence of Supplies Ledger Cards, the inclusion of negative

balances amounting to ₱623,726.29, and the presence of dormant accounts totaling

₱22,200,675.08, which are inconsistent with paragraph 76 of IPSAS 1, thus

affecting the fair presentation of the account balances in the financial statements.

3.1 Paragraph 76 of IPSAS 1 states that an asset should be classified as a current

asset if it is expected to be realized, sold, or consumed in the normal course of

the entity’s operating cycle, or if it is held for trading purposes or for the short-

term and expected to be realized within twelve months of the reporting date.

3.2 Additionally, paragraph 79 of the Standard specifies that current assets include

inventories that are either realized, consumed, or sold as part of the entity’s

normal operating cycle, even if they are not expected to be realized within

twelve months of the reporting date.

3.3 In this regard, COA Circular No. 2023-008, issued on August 17, 2023, provides

the guidelines and procedures for the proper disposition of dormant accounts,

amending COA Circular No. 2016-005 dated December 19, 2016. One of the

primary reasons for this issuance is that the Annual Financial Reports of

government agencies have highlighted a significant volume of dormant

accounts. Additionally, the details and validity of these accounts cannot be fully

verified due to the lack of supporting records or documents and insufficient

knowledge among the current accounting personnel, which affects the fair

presentation of the financial statements.

3.4 Item 5.6 of COA Circular No. 2023-008, dated August 17, 2023, defines

dormant accounts as individual or group of account balances within the general

ledger that have remained non-moving or inactive for ten (10) years or more

from the last transaction recorded in the books.

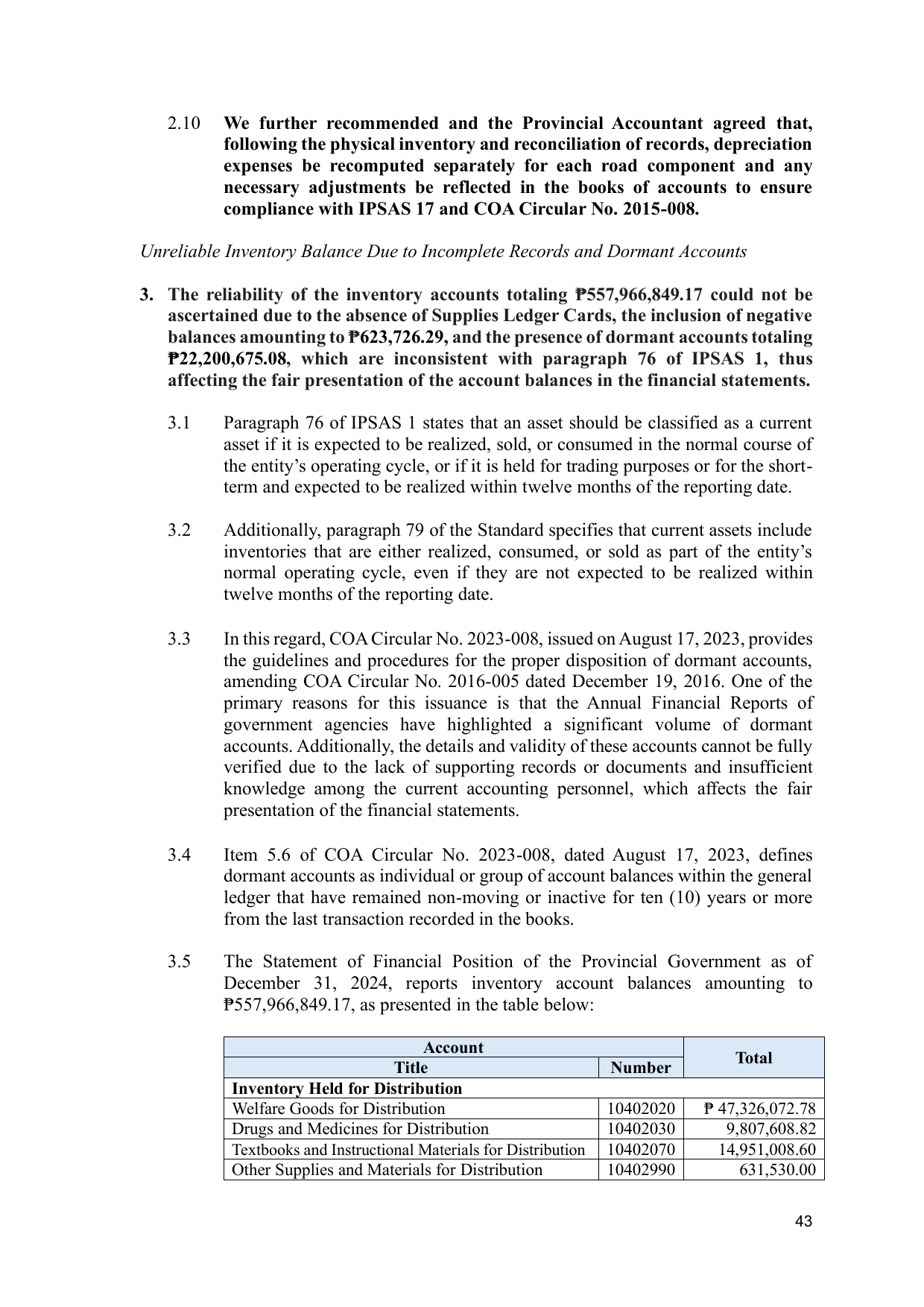

3.5 The Statement of Financial Position of the Provincial Government as of

December 31, 2024, reports inventory account balances amounting to

₱557,966,849.17, as presented in the table below:

Account

Total

Title Number

Inventory Held for Distribution

Welfare Goods for Distribution 10402020 ₱ 47,326,072.78

Drugs and Medicines for Distribution 10402030 9,807,608.82

Textbooks and Instructional Materials for Distribution 10402070 14,951,008.60

Other Supplies and Materials for Distribution 10402990 631,530.00

43