2015, and COA Circular No. 2020-006 dated January 31, 2020, to ensure

that all road network assets are accurately reflected in the financial

statements and comply with established accounting and reporting

standards.

Unreliable Computation of Accumulated Depreciation Expense for Road Networks

2. The depreciation expense for the Road Network, with an accumulated

depreciation balance of ₱471,365,166.38, was calculated using a uniform estimated

useful life of ten years and a 10% salvage value for the total cost rather than for

each road component, contrary to COA Circular No. 2015-008 and paragraph 73

IPSAS 17, thus raising concerns about the reliability of the balance and resulting

in an undetermined amount of discrepancy.

2.1 Items IV and V of COA Circular No. 2015-008 dated November 23, 2015

provide, among others, that the components of local roads should be segregated,

and the cost of each component must be recognized individually. Accordingly,

separate subsidiary ledgers must be maintained for the road and its components,

namely: (a) road lot, (b) road pavement, (c) drainage and slope protection

structures and (d) other miscellaneous structures. Each depreciable component

of the road network, except for the road lot component, shall be depreciated

separately using the straight-line method of depreciation. In addition, no

residual value shall be applied to the depreciable components of the road

network system. The useful life of the local roads should be determined based

on the range prescribed by COA, taking into account factors such as design,

users, and volume of usage.

2.2 Additionally, paragraph 73 of the IPSAS 17 defines the useful life of an asset in

terms of its expected utility to the entity. Estimating the useful life of an asset

involves judgment based on the entity’s experience with similar assets.

2.3 To support the development of local road asset management and ensure that

accounting practices in local government units align with IPSAS, the

Department of the Interior and Local Government (DILG) issued Memorandum

Circular No. 2020-155 dated November 16, 2020, on the adoption of the Local

Road Asset Management Manual (LRAMM).

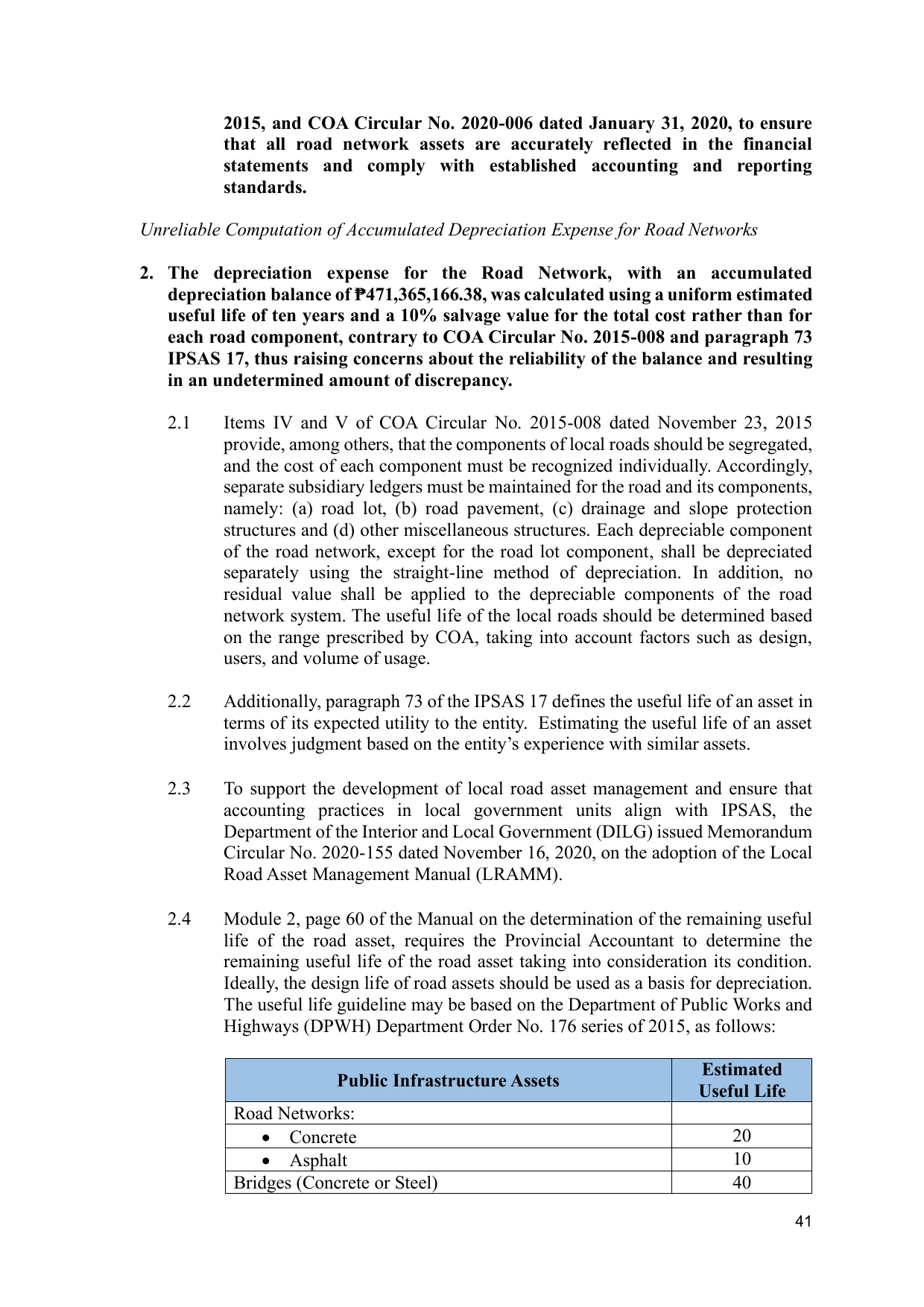

2.4 Module 2, page 60 of the Manual on the determination of the remaining useful

life of the road asset, requires the Provincial Accountant to determine the

remaining useful life of the road asset taking into consideration its condition.

Ideally, the design life of road assets should be used as a basis for depreciation.

The useful life guideline may be based on the Department of Public Works and

Highways (DPWH) Department Order No. 176 series of 2015, as follows:

Estimated

Public Infrastructure Assets

Useful Life

Road Networks:

• Concrete 20

• Asphalt 10

Bridges (Concrete or Steel) 40

41