)

Reason for

Agency Action Plan (for Partially Implemented and Not Implemented Laem cnt Par ial/Delay/No Action Taken/Action

Recommendations) fon Implementation, to be Taken.

if applicable

Audit Observations Audit Recommendations | Action Plan/ Target

Remarks Implementation

This coluntn shall be filled out by the eee ent Date

agency, detailing the appropriate Rex ousible

course of action on the audit Ps

observation identified. [From [to _|

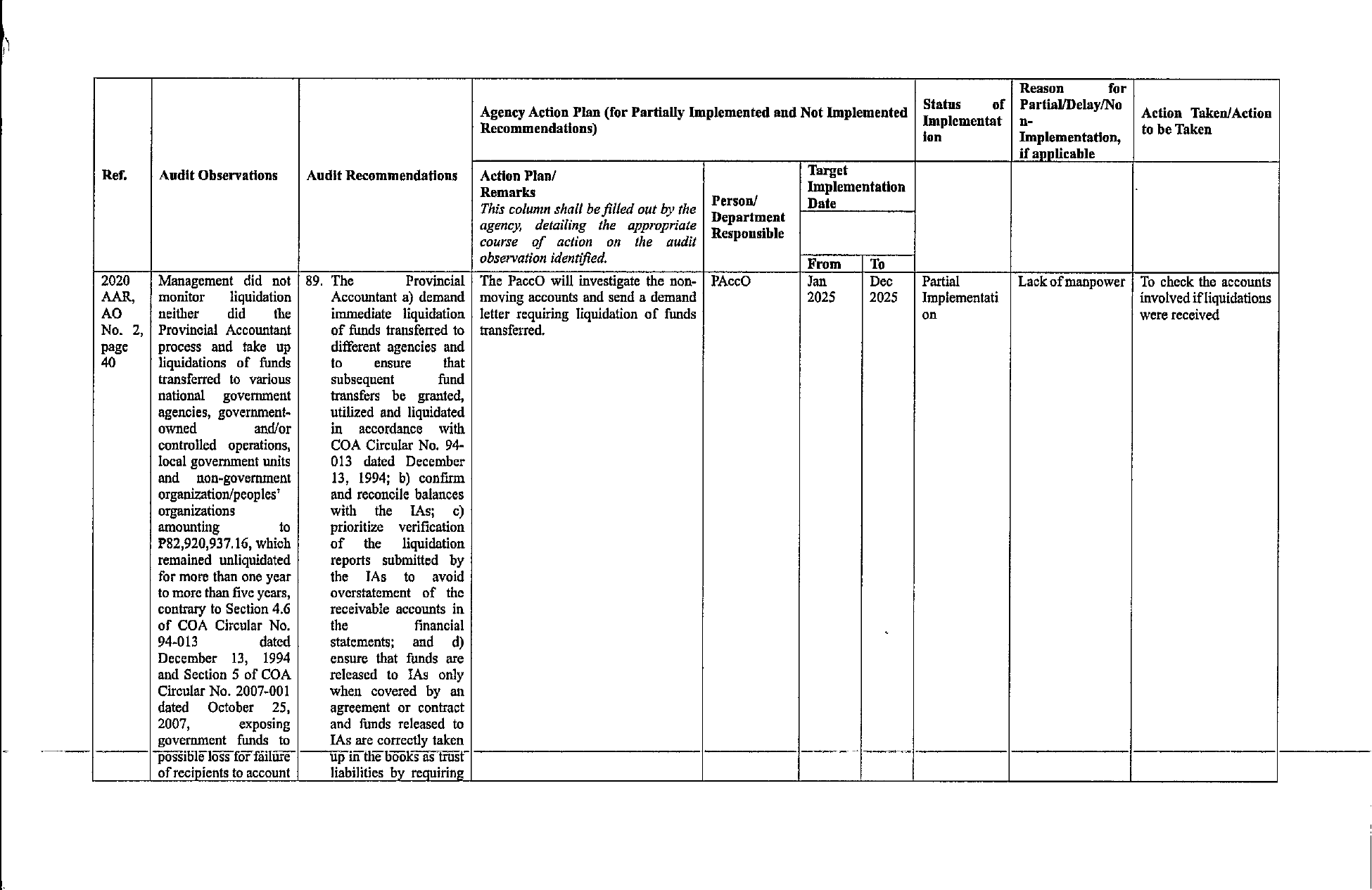

2020 Management did not | 89. The Provincial | The PaccO will investigate the non- | PAccO Jan Dec Partial Lack of manpower } To check the accounts

AAR, | monitor liquidation Accountant a) demand | moving accounts and send a demand 2025 2025 | Imptementati involved if liquidations

AO neither did the immediate liquidation | letter requiring liquidation of funds on were received

No. 2, | Provincial Accountant of funds transferted to | transferred.

page Process and take up different agencies and

40 liquidations of funds to ensure that

transferred to various subsequent fund

national = government transfers be granted,

agencies, government- utilized and liquidated

owned and/or in accordance with

controlled operations, COA Circular No. 94-

local government units 013 dated December

and noa-government 13, 1994; b) confirm

organization/peoples’ and reconcile balances

organizations with the TAs; o)

amounting to prioritize verification

P82,920,937.16, which of the liquidation

remained unliquidated reports submitted by

for more than one year the IAs to avoid

to more than five years, overstatement of the

contrary to Section 4.6 receivable accounts in

of COA Circular No. the financial .

94-013 dated statements; and d)

December 13, 1994 ensure that funds are

and Section 5 of COA released to IAs only

Circular No. 2007-001 when covered by an

dated October 25, agreement or contract

2007, exposing and funds released to

government funds to TAs are cortectly taken

T ~~" possible loss for failire | “ipin tlie books as ‘trust I

of recipients to account liabilities by requiring