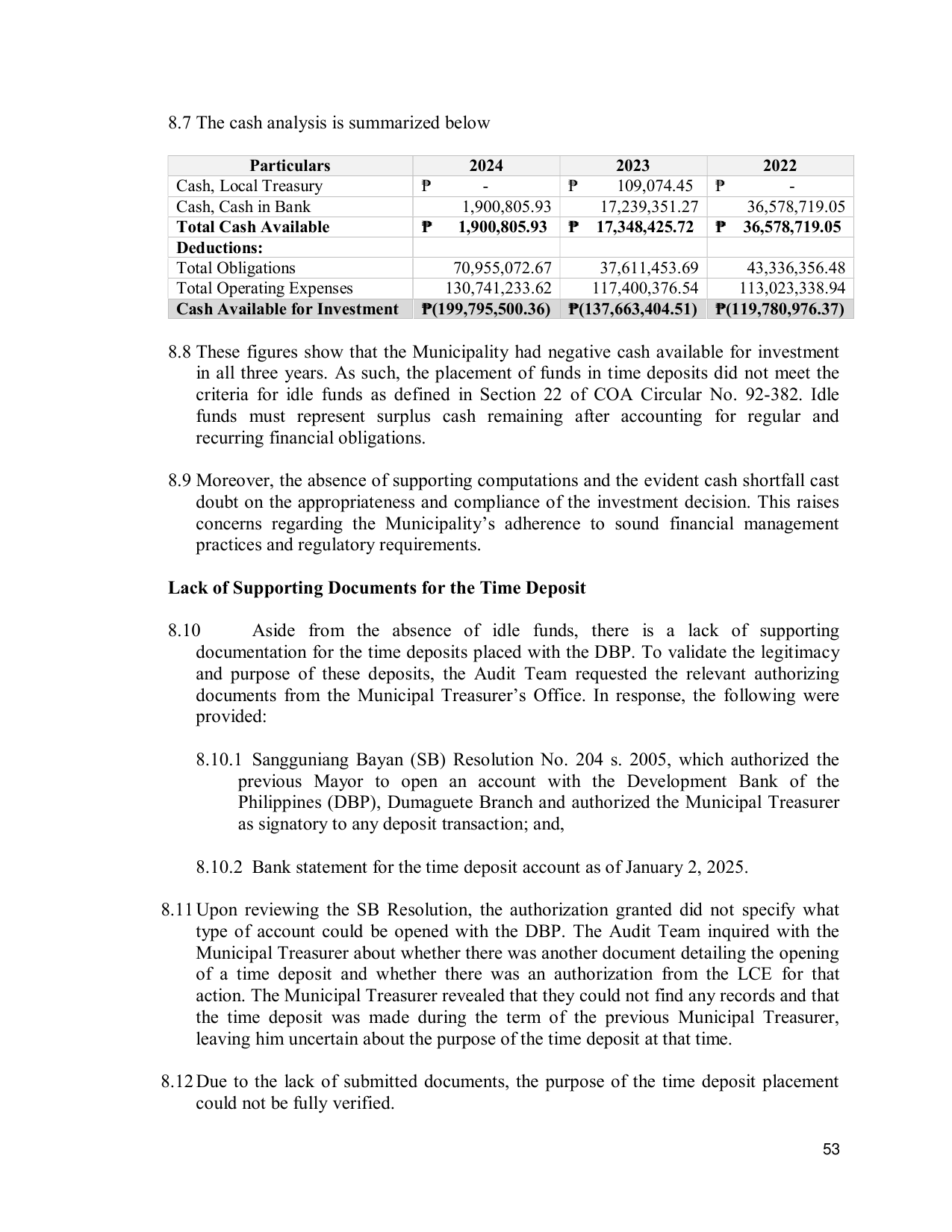

8.7 The cash analysis is summarized below

Particulars 2024 2023 2022

Cash, Local Treasury ₱ - ₱ 109,074.45 ₱ -

Cash, Cash in Bank 1,900,805.93 17,239,351.27 36,578,719.05

Total Cash Available ₱ 1,900,805.93 ₱ 17,348,425.72 ₱ 36,578,719.05

Deductions:

Total Obligations 70,955,072.67 37,611,453.69 43,336,356.48

Total Operating Expenses 130,741,233.62 117,400,376.54 113,023,338.94

Cash Available for Investment ₱(199,795,500.36) ₱(137,663,404.51) ₱(119,780,976.37)

8.8 These figures show that the Municipality had negative cash available for investment

in all three years. As such, the placement of funds in time deposits did not meet the

criteria for idle funds as defined in Section 22 of COA Circular No. 92-382. Idle

funds must represent surplus cash remaining after accounting for regular and

recurring financial obligations.

8.9 Moreover, the absence of supporting computations and the evident cash shortfall cast

doubt on the appropriateness and compliance of the investment decision. This raises

concerns regarding the Municipality’s adherence to sound financial management

practices and regulatory requirements.

Lack of Supporting Documents for the Time Deposit

8.10 Aside from the absence of idle funds, there is a lack of supporting

documentation for the time deposits placed with the DBP. To validate the legitimacy

and purpose of these deposits, the Audit Team requested the relevant authorizing

documents from the Municipal Treasurer’s Office. In response, the following were

provided:

8.10.1 Sangguniang Bayan (SB) Resolution No. 204 s. 2005, which authorized the

previous Mayor to open an account with the Development Bank of the

Philippines (DBP), Dumaguete Branch and authorized the Municipal Treasurer

as signatory to any deposit transaction; and,

8.10.2 Bank statement for the time deposit account as of January 2, 2025.

8.11 Upon reviewing the SB Resolution, the authorization granted did not specify what

type of account could be opened with the DBP. The Audit Team inquired with the

Municipal Treasurer about whether there was another document detailing the opening

of a time deposit and whether there was an authorization from the LCE for that

action. The Municipal Treasurer revealed that they could not find any records and that

the time deposit was made during the term of the previous Municipal Treasurer,

leaving him uncertain about the purpose of the time deposit at that time.

8.12 Due to the lack of submitted documents, the purpose of the time deposit placement

could not be fully verified.

53