Time Deposit

8. The Municipality inappropriately invested a total of ₱16,623,828.41 in time deposits

without proper compliance with COA Circular No. 92-382, as the funds under the

General Fund (GF) did not qualify as idle and documentary support was lacking,

thereby rendering its propriety doubtful.

8.1 Section 21 of COA Circular No. 92-382 dated July 3, 1992, states that provinces,

cities, and municipalities may deposit idle funds from the General Fund into time

deposit accounts with authorized depository banks, subject to prior authorization from

the local sanggunian and the approval of the local chief executive (LCE).

8.2 Moreover, Section 22 of the Circular defines idle funds in excess of normal operating

requirements as the level of funds an entity can freely invest in government securities

and/or fixed-term deposits. This determination should account for provisions needed

to cover regular and recurring operating expenses, such as salaries and wages, repairs

and maintenance, inventories and supplies, debt servicing, and other obligations

within the context of the entity’s cash operating cycle. Notably, unremitted national

collections and funds earmarked for obligations to government corporations or

cooperatives shall not be considered part of the idle funds of local government units.

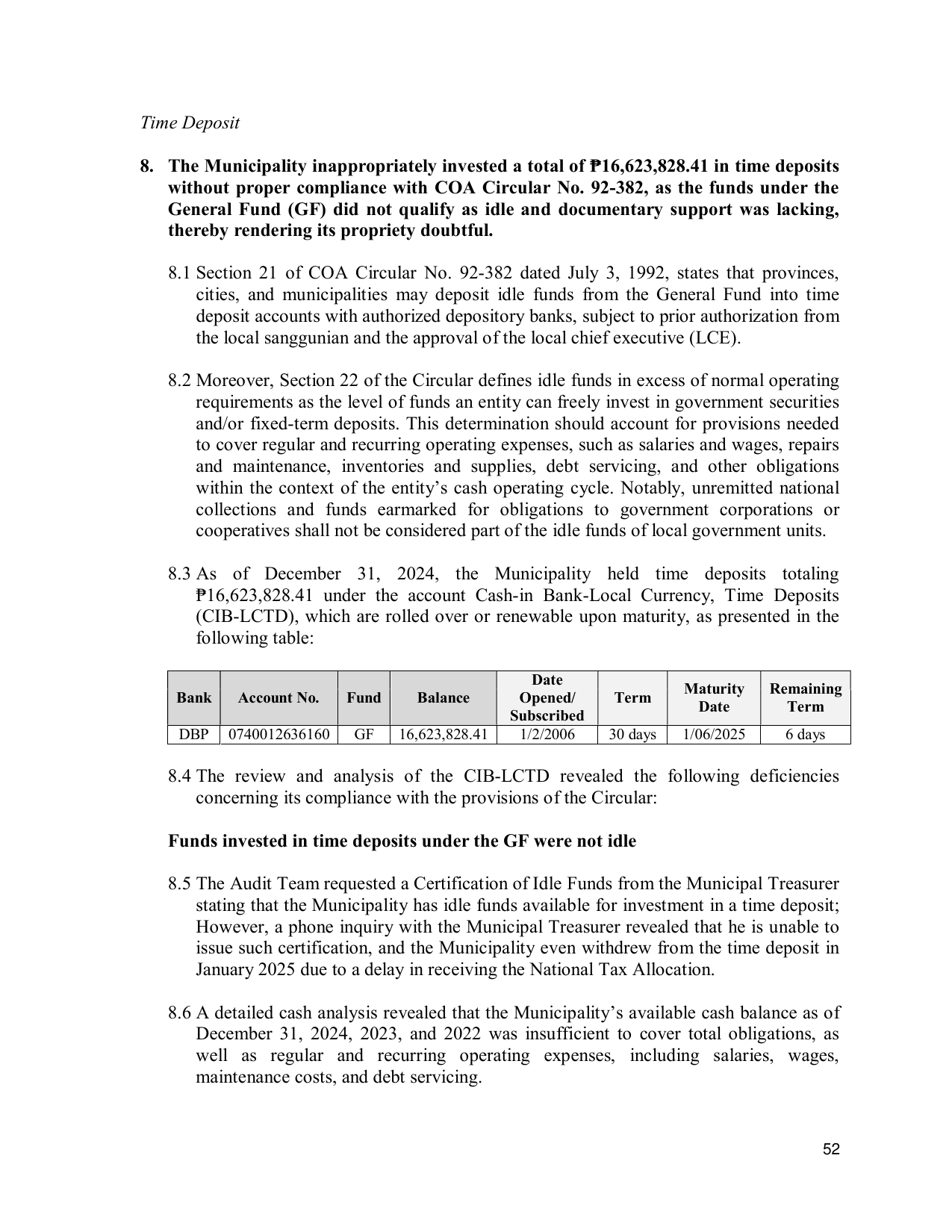

8.3 As of December 31, 2024, the Municipality held time deposits totaling

₱16,623,828.41 under the account Cash-in Bank-Local Currency, Time Deposits

(CIB-LCTD), which are rolled over or renewable upon maturity, as presented in the

following table:

Date

Maturity Remaining

Bank Account No. Fund Balance Opened/ Term

Date Term

Subscribed

DBP 0740012636160 GF 16,623,828.41 1/2/2006 30 days 1/06/2025 6 days

8.4 The review and analysis of the CIB-LCTD revealed the following deficiencies

concerning its compliance with the provisions of the Circular:

Funds invested in time deposits under the GF were not idle

8.5 The Audit Team requested a Certification of Idle Funds from the Municipal Treasurer

stating that the Municipality has idle funds available for investment in a time deposit;

However, a phone inquiry with the Municipal Treasurer revealed that he is unable to

issue such certification, and the Municipality even withdrew from the time deposit in

January 2025 due to a delay in receiving the National Tax Allocation.

8.6 A detailed cash analysis revealed that the Municipality’s available cash balance as of

December 31, 2024, 2023, and 2022 was insufficient to cover total obligations, as

well as regular and recurring operating expenses, including salaries, wages,

maintenance costs, and debt servicing.

52