5.1. Section 4(6) of P.D. No. 1445 basically requires that “Claims against government

funds shall be supported with complete documentation.”

5.2. Section 98 thereof likewise requires that any unliquidated balances of accounts

payable in the books may be reverted to the unappropriated surplus of the GF,

provided that these have been outstanding for two years or more and against which

no actual claims, administrative or judicial, have been filed or which are not covered

by perfected contracts on record.

5.3. Further, Section 110 thereof states the objectives of government accounting, primary

of which is to provide sufficient and relevant information for guidance in the receipt,

disposition and utilization of funds and property, thus, as emphasized in Section 111,

it is necessary that these accounts be kept in such detail so as to provide the needed

information vital to effective decision-making by Management.

5.4. Moreover, Section 04.s, Chapter 2 of the NGAS Manual for LGUs, Volume I,

provides that, “Liability shall be recognized at the time goods and services are

accepted or rendered and supplier/creditor bills are received.”

5.5. In accounting, Accounts Payable is classified under Current Liabilities, which means

that these obligations are due to be settled or liquidated within the current operating

cycle of the agency. Considering that Accounts Payable are normally booked at the

end of the current year, the accounts are expected to be paid within the next CY.

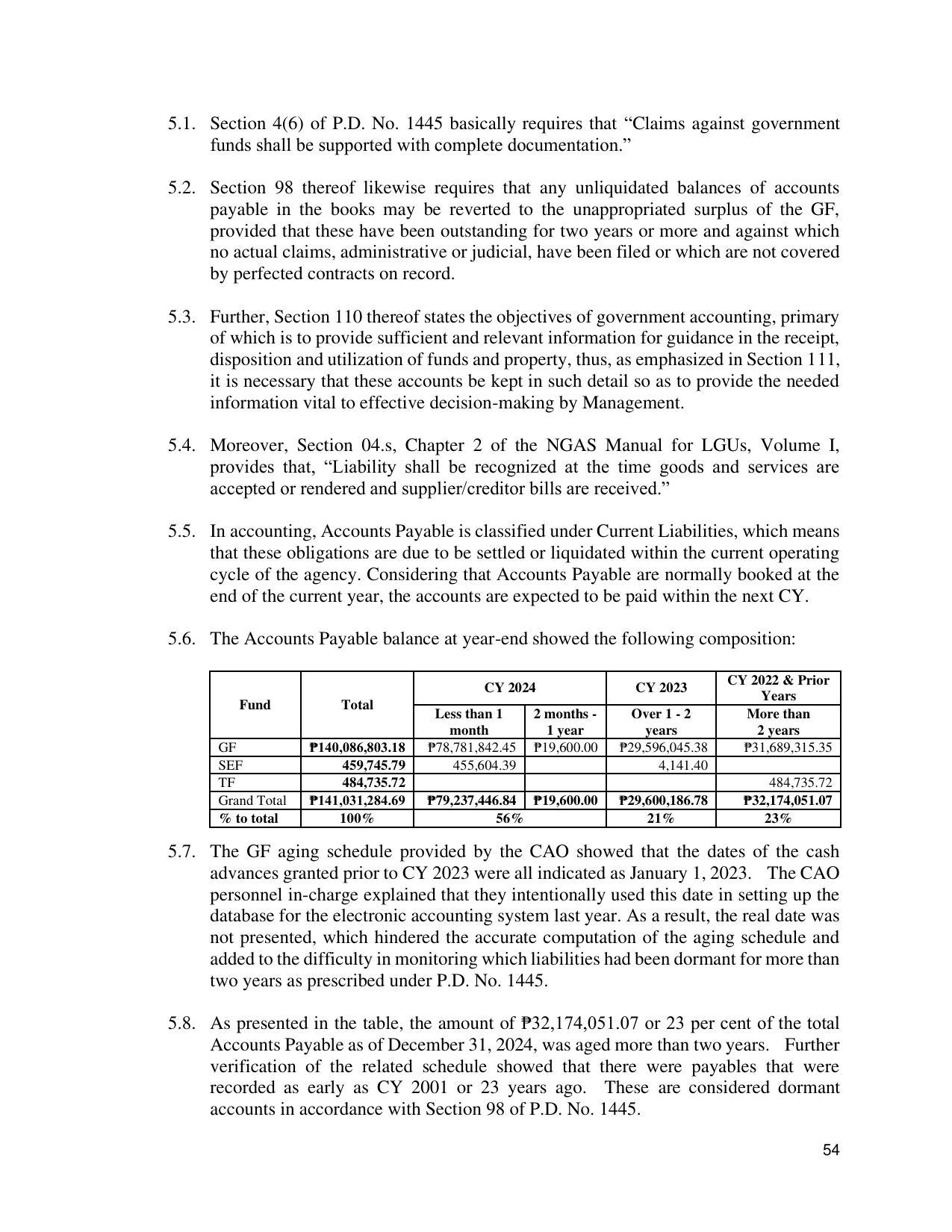

5.6. The Accounts Payable balance at year-end showed the following composition:

CY 2022 & Prior

CY 2024 CY 2023

Years

Fund Total

Less than 1 2 months - Over 1 - 2 More than

month 1 year years 2 years

GF ₱140,086,803.18 ₱78,781,842.45 ₱19,600.00 ₱29,596,045.38 ₱31,689,315.35

SEF 459,745.79 455,604.39 4,141.40

TF 484,735.72 484,735.72

Grand Total ₱141,031,284.69 ₱79,237,446.84 ₱19,600.00 ₱29,600,186.78 ₱32,174,051.07

% to total 100% 56% 21% 23%

5.7. The GF aging schedule provided by the CAO showed that the dates of the cash

advances granted prior to CY 2023 were all indicated as January 1, 2023. The CAO

personnel in-charge explained that they intentionally used this date in setting up the

database for the electronic accounting system last year. As a result, the real date was

not presented, which hindered the accurate computation of the aging schedule and

added to the difficulty in monitoring which liabilities had been dormant for more than

two years as prescribed under P.D. No. 1445.

5.8. As presented in the table, the amount of ₱32,174,051.07 or 23 per cent of the total

Accounts Payable as of December 31, 2024, was aged more than two years. Further

verification of the related schedule showed that there were payables that were

recorded as early as CY 2001 or 23 years ago. These are considered dormant

accounts in accordance with Section 98 of P.D. No. 1445.

54