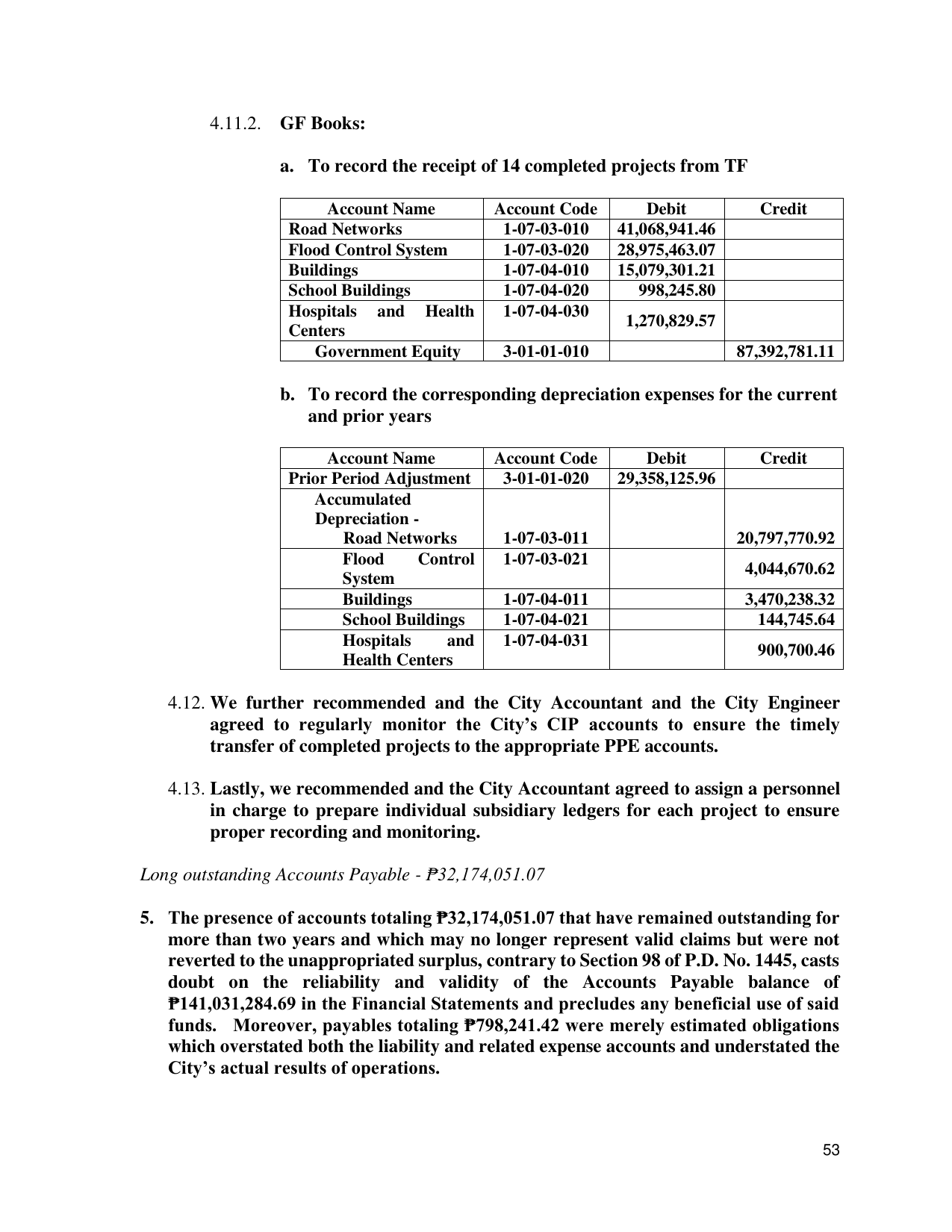

4.11.2. GF Books:

a. To record the receipt of 14 completed projects from TF

Account Name Account Code Debit Credit

Road Networks 1-07-03-010 41,068,941.46

Flood Control System 1-07-03-020 28,975,463.07

Buildings 1-07-04-010 15,079,301.21

School Buildings 1-07-04-020 998,245.80

Hospitals and Health 1-07-04-030

1,270,829.57

Centers

Government Equity 3-01-01-010 87,392,781.11

b. To record the corresponding depreciation expenses for the current

and prior years

Account Name Account Code Debit Credit

Prior Period Adjustment 3-01-01-020 29,358,125.96

Accumulated

Depreciation -

Road Networks 1-07-03-011 20,797,770.92

Flood Control 1-07-03-021

4,044,670.62

System

Buildings 1-07-04-011 3,470,238.32

School Buildings 1-07-04-021 144,745.64

Hospitals and 1-07-04-031

900,700.46

Health Centers

4.12. We further recommended and the City Accountant and the City Engineer

agreed to regularly monitor the City’s CIP accounts to ensure the timely

transfer of completed projects to the appropriate PPE accounts.

4.13. Lastly, we recommended and the City Accountant agreed to assign a personnel

in charge to prepare individual subsidiary ledgers for each project to ensure

proper recording and monitoring.

Long outstanding Accounts Payable - ₱32,174,051.07

5. The presence of accounts totaling ₱32,174,051.07 that have remained outstanding for

more than two years and which may no longer represent valid claims but were not

reverted to the unappropriated surplus, contrary to Section 98 of P.D. No. 1445, casts

doubt on the reliability and validity of the Accounts Payable balance of

₱141,031,284.69 in the Financial Statements and precludes any beneficial use of said

funds. Moreover, payables totaling ₱798,241.42 were merely estimated obligations

which overstated both the liability and related expense accounts and understated the

City’s actual results of operations.

53