5.9. Our inquiry disclosed that all documents pertaining to CY 2024 and prior years’

obligations that were processed for payment have already been paid and that the City

is no longer in possession of unpaid vouchers/invoices pertaining to prior years’

accounts.

5.10. As these may no longer represent valid claims given the length of time that has

elapsed, continued reporting thereof as liabilities adversely affected the fairness of

the balance of Accounts Payable in the financial statements. Moreover, non-

reversion thereof to the unappropriated surplus precluded the City from having access

to available funds which otherwise could be used for other beneficial purposes.

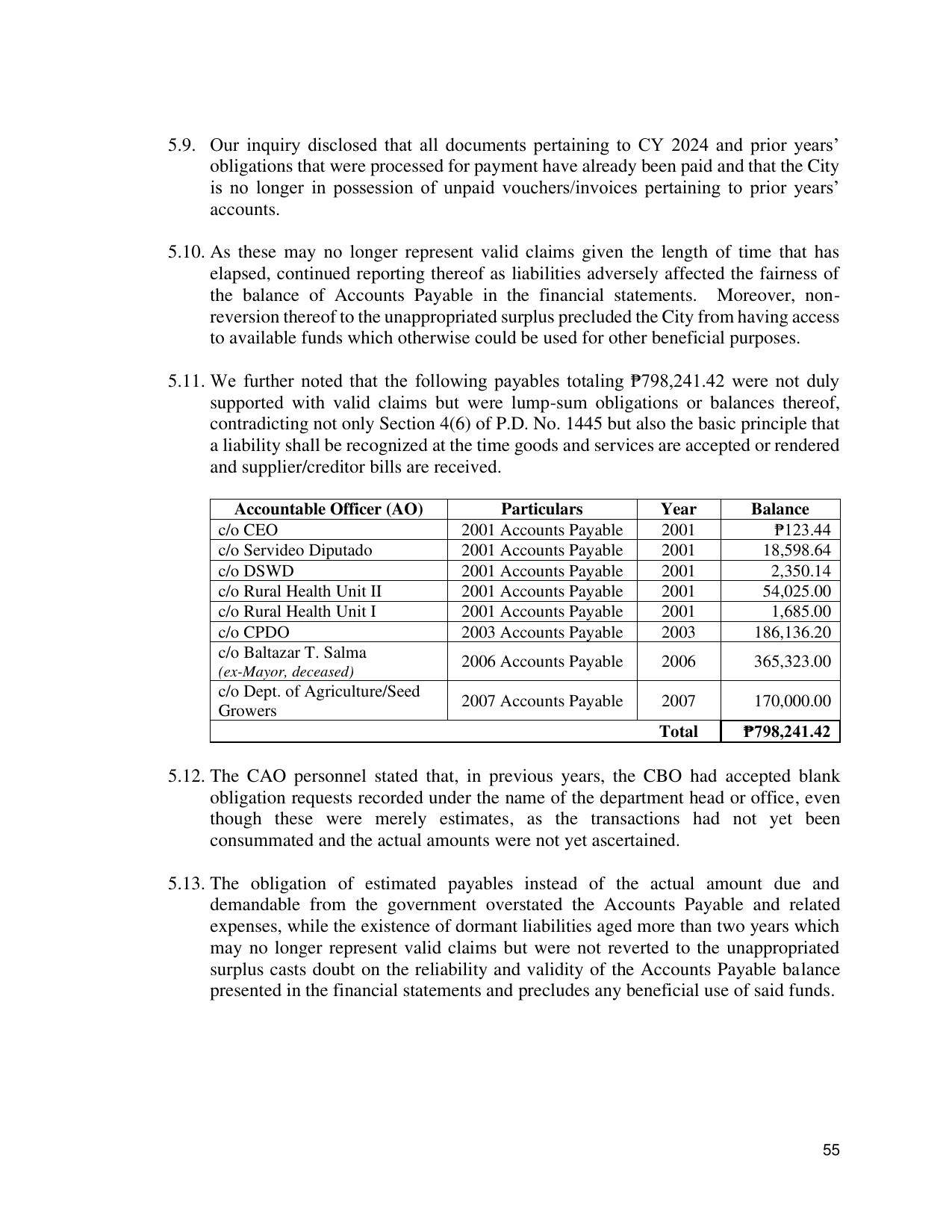

5.11. We further noted that the following payables totaling ₱798,241.42 were not duly

supported with valid claims but were lump-sum obligations or balances thereof,

contradicting not only Section 4(6) of P.D. No. 1445 but also the basic principle that

a liability shall be recognized at the time goods and services are accepted or rendered

and supplier/creditor bills are received.

Accountable Officer (AO) Particulars Year Balance

c/o CEO 2001 Accounts Payable 2001 ₱123.44

c/o Servideo Diputado 2001 Accounts Payable 2001 18,598.64

c/o DSWD 2001 Accounts Payable 2001 2,350.14

c/o Rural Health Unit II 2001 Accounts Payable 2001 54,025.00

c/o Rural Health Unit I 2001 Accounts Payable 2001 1,685.00

c/o CPDO 2003 Accounts Payable 2003 186,136.20

c/o Baltazar T. Salma

2006 Accounts Payable 2006 365,323.00

(ex-Mayor, deceased)

c/o Dept. of Agriculture/Seed

2007 Accounts Payable 2007 170,000.00

Growers

Total ₱798,241.42

5.12. The CAO personnel stated that, in previous years, the CBO had accepted blank

obligation requests recorded under the name of the department head or office, even

though these were merely estimates, as the transactions had not yet been

consummated and the actual amounts were not yet ascertained.

5.13. The obligation of estimated payables instead of the actual amount due and

demandable from the government overstated the Accounts Payable and related

expenses, while the existence of dormant liabilities aged more than two years which

may no longer represent valid claims but were not reverted to the unappropriated

surplus casts doubt on the reliability and validity of the Accounts Payable balance

presented in the financial statements and precludes any beneficial use of said funds.

55