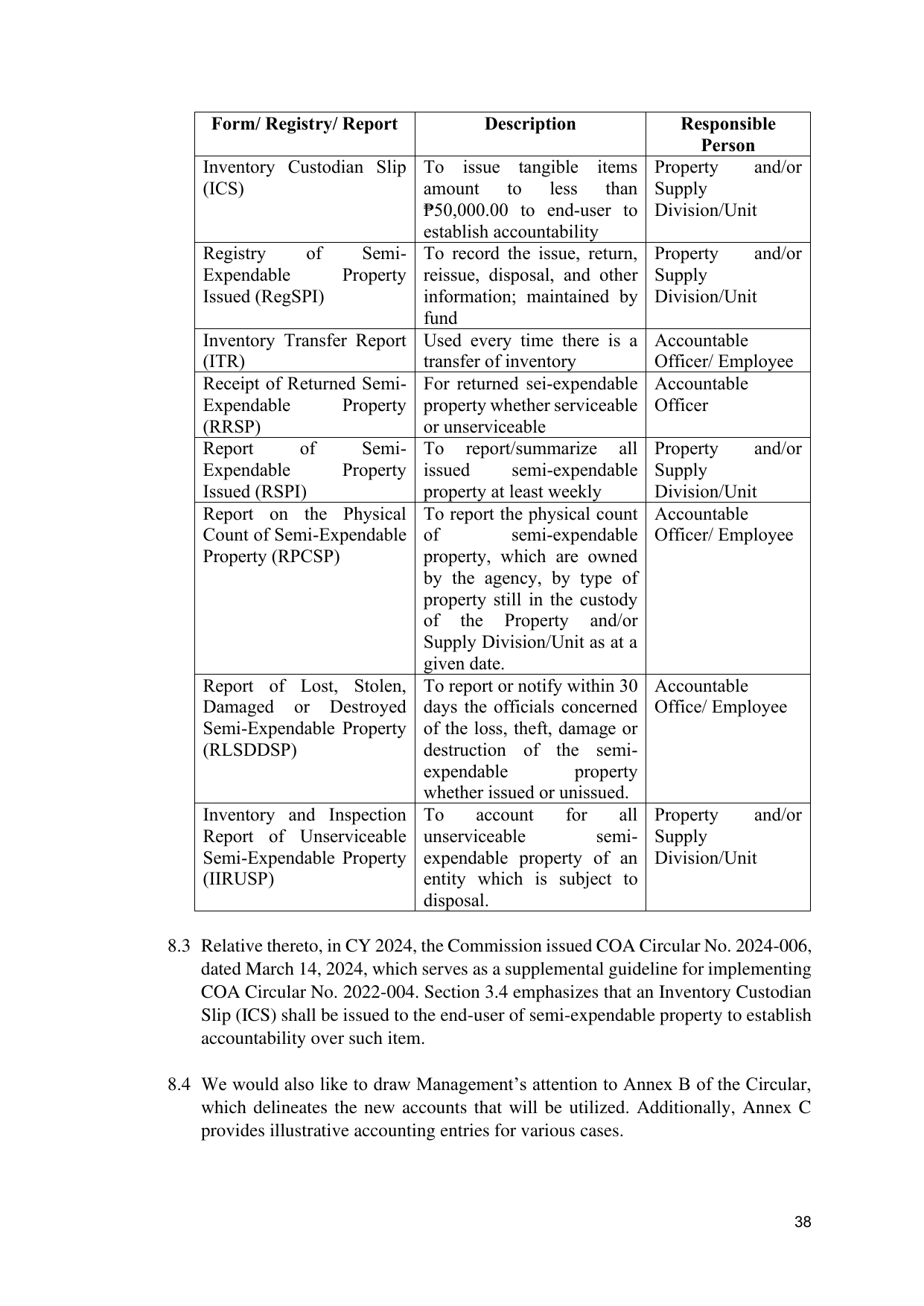

Form/ Registry/ Report Description Responsible

Person

Inventory Custodian Slip To issue tangible items Property and/or

(ICS) amount to less than Supply

₱50,000.00 to end-user to Division/Unit

establish accountability

Registry of Semi- To record the issue, return, Property and/or

Expendable Property reissue, disposal, and other Supply

Issued (RegSPI) information; maintained by Division/Unit

fund

Inventory Transfer Report Used every time there is a Accountable

(ITR) transfer of inventory Officer/ Employee

Receipt of Returned Semi- For returned sei-expendable Accountable

Expendable Property property whether serviceable Officer

(RRSP) or unserviceable

Report of Semi- To report/summarize all Property and/or

Expendable Property issued semi-expendable Supply

Issued (RSPI) property at least weekly Division/Unit

Report on the Physical To report the physical count Accountable

Count of Semi-Expendable of semi-expendable Officer/ Employee

Property (RPCSP) property, which are owned

by the agency, by type of

property still in the custody

of the Property and/or

Supply Division/Unit as at a

given date.

Report of Lost, Stolen, To report or notify within 30 Accountable

Damaged or Destroyed days the officials concerned Office/ Employee

Semi-Expendable Property of the loss, theft, damage or

(RLSDDSP) destruction of the semi-

expendable property

whether issued or unissued.

Inventory and Inspection To account for all Property and/or

Report of Unserviceable unserviceable semi- Supply

Semi-Expendable Property expendable property of an Division/Unit

(IIRUSP) entity which is subject to

disposal.

8.3 Relative thereto, in CY 2024, the Commission issued COA Circular No. 2024-006,

dated March 14, 2024, which serves as a supplemental guideline for implementing

COA Circular No. 2022-004. Section 3.4 emphasizes that an Inventory Custodian

Slip (ICS) shall be issued to the end-user of semi-expendable property to establish

accountability over such item.

8.4 We would also like to draw Management’s attention to Annex B of the Circular,

which delineates the new accounts that will be utilized. Additionally, Annex C

provides illustrative accounting entries for various cases.

38