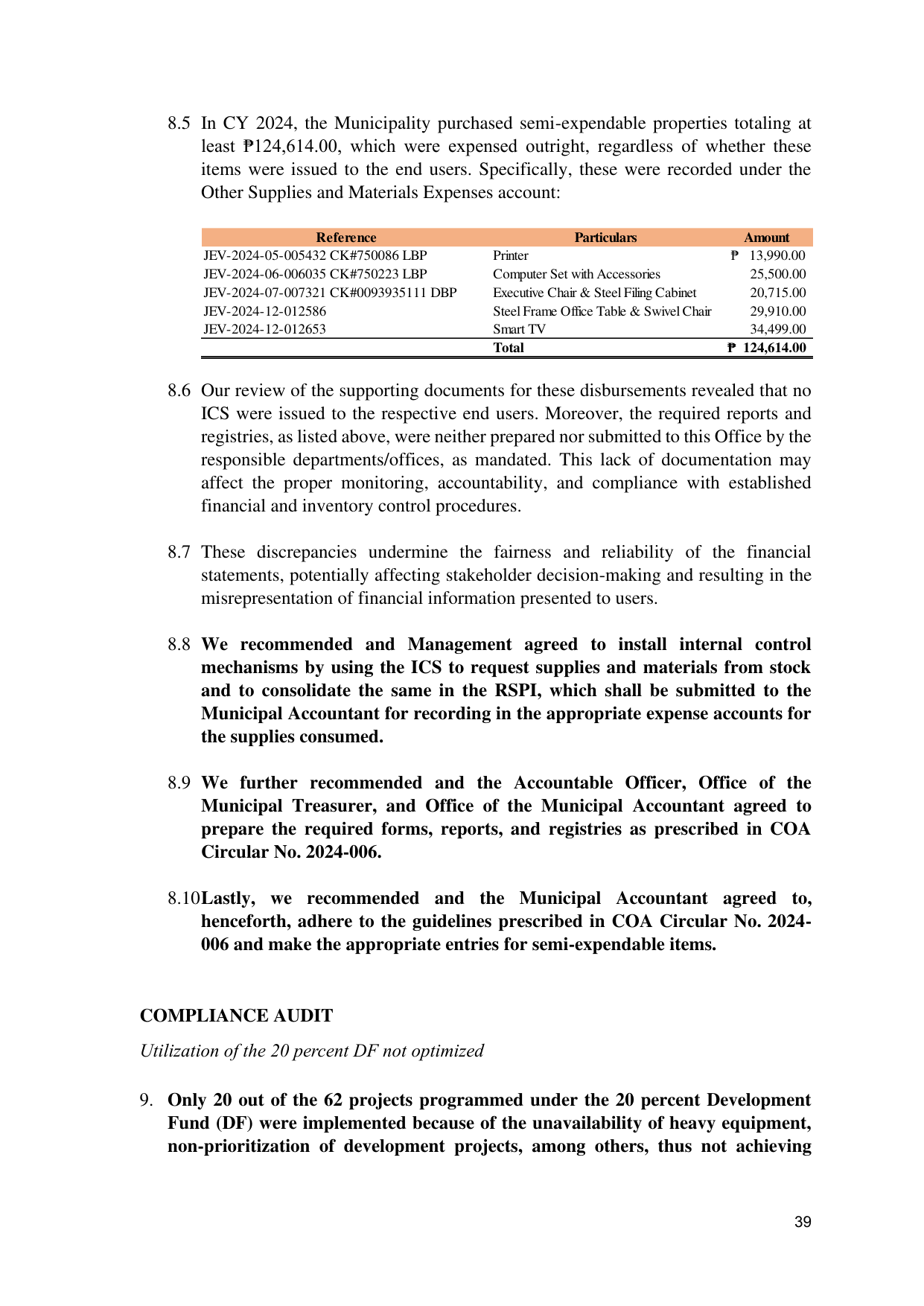

8.5 In CY 2024, the Municipality purchased semi-expendable properties totaling at

least ₱124,614.00, which were expensed outright, regardless of whether these

items were issued to the end users. Specifically, these were recorded under the

Other Supplies and Materials Expenses account:

Reference Particulars Amount

JEV-2024-05-005432 CK#750086 LBP Printer ₱ 13,990.00

JEV-2024-06-006035 CK#750223 LBP Computer Set with Accessories 25,500.00

JEV-2024-07-007321 CK#0093935111 DBP Executive Chair & Steel Filing Cabinet 20,715.00

JEV-2024-12-012586 Steel Frame Office Table & Swivel Chair 29,910.00

JEV-2024-12-012653 Smart TV 34,499.00

Total ₱ 124,614.00

8.6 Our review of the supporting documents for these disbursements revealed that no

ICS were issued to the respective end users. Moreover, the required reports and

registries, as listed above, were neither prepared nor submitted to this Office by the

responsible departments/offices, as mandated. This lack of documentation may

affect the proper monitoring, accountability, and compliance with established

financial and inventory control procedures.

8.7 These discrepancies undermine the fairness and reliability of the financial

statements, potentially affecting stakeholder decision-making and resulting in the

misrepresentation of financial information presented to users.

8.8 We recommended and Management agreed to install internal control

mechanisms by using the ICS to request supplies and materials from stock

and to consolidate the same in the RSPI, which shall be submitted to the

Municipal Accountant for recording in the appropriate expense accounts for

the supplies consumed.

8.9 We further recommended and the Accountable Officer, Office of the

Municipal Treasurer, and Office of the Municipal Accountant agreed to

prepare the required forms, reports, and registries as prescribed in COA

Circular No. 2024-006.

8.10 Lastly, we recommended and the Municipal Accountant agreed to,

henceforth, adhere to the guidelines prescribed in COA Circular No. 2024-

006 and make the appropriate entries for semi-expendable items.

COMPLIANCE AUDIT

Utilization of the 20 percent DF not optimized

9. Only 20 out of the 62 projects programmed under the 20 percent Development

Fund (DF) were implemented because of the unavailability of heavy equipment,

non-prioritization of development projects, among others, thus not achieving

39