raises concerns regarding the reliability of financial reports and may lead to

misstatements in the inventories and corresponding expenditure accounts.

Additionally, the delay in recording transactions affects budget utilization

monitoring, which could impact decision-making and resource allocation.

7.5 We recommended and the Municipal Treasurer agreed to ensure the timely

consolidation and submission of the SSMI in compliance with Sec. 121 of the

NGAS Manual for LGUs, Vol. 1.

7.6 We further recommended and the Municipal Accountant agreed to conduct a

thorough reconciliation of inventory balances and record the corresponding

journal entries to reflect the correct financial position.

Semi-expendable properties erroneously recorded to Other Supplies and Materials

Expenses - ₱124,614.00

8. Purchases of semi-expendable properties totaling at least ₱124,614.00 were

recorded under the Other Supplies and Materials Expenses account instead of the

appropriate semi-expendable inventory account, contrary to COA Circular 2024-

006, thus, eliminating the required accounting of the receipt and utilization

established through the use of Inventory Custodian Slips and Report on Semi-

Expendable Property Issued, and other reports and registries, which could result

in the misstatements of semi-expendable inventories and corresponding expense

accounts at the end of the year.

8.1 COA Circular No. 2022-004 dated May 31, 2022, provides guidelines for

implementing the increase in the capitalization threshold from ₱15,000.00 to

₱50,000.00. Specifically, Section 4 thereof requires that tangible items meeting the

definition and recognition criteria of Property, Plant, and Equipment (PPE) but

costing below ₱50,000.00 be accounted for in the books of accounts of the agencies

as semi-expendable property.

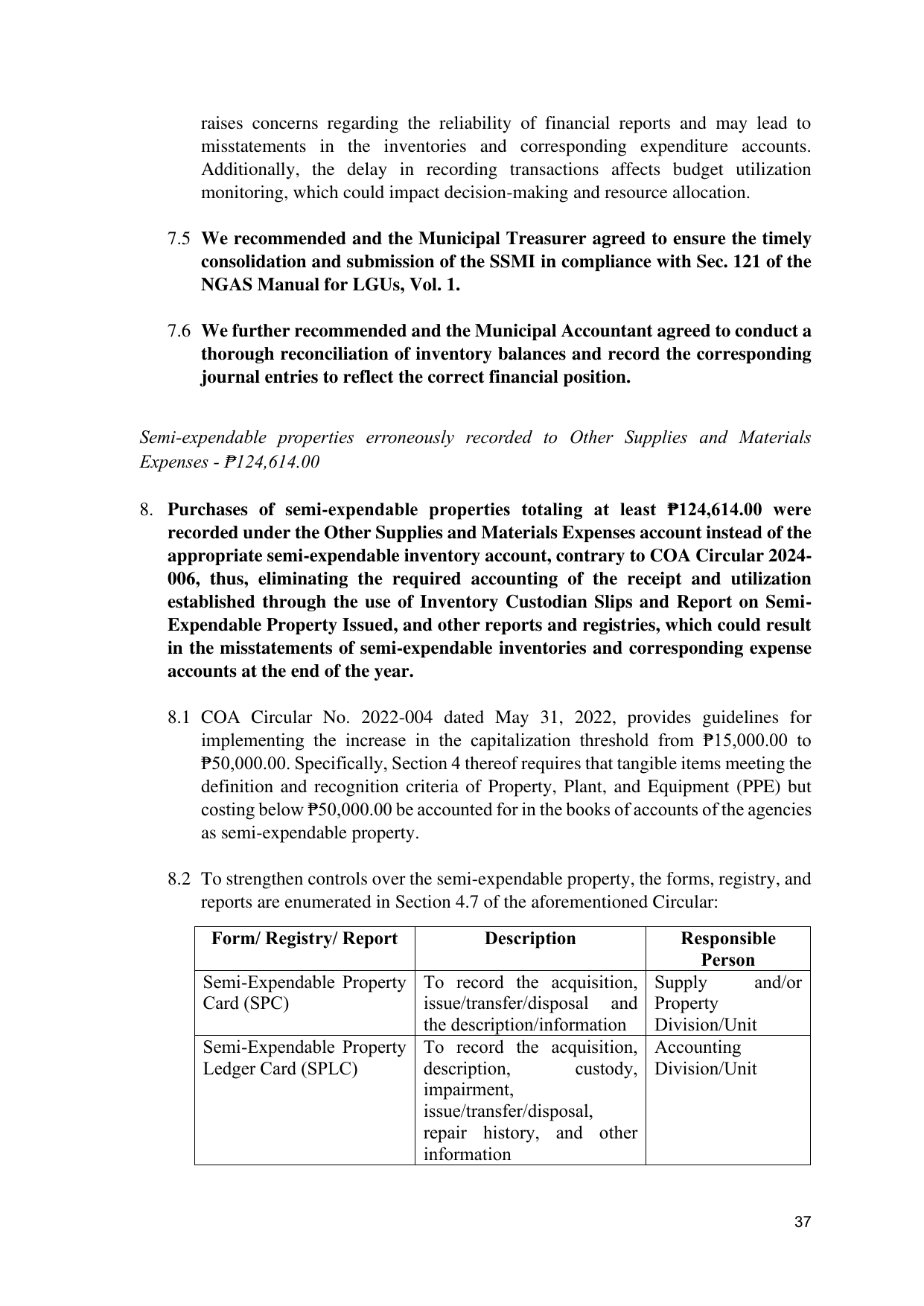

8.2 To strengthen controls over the semi-expendable property, the forms, registry, and

reports are enumerated in Section 4.7 of the aforementioned Circular:

Form/ Registry/ Report Description Responsible

Person

Semi-Expendable Property To record the acquisition, Supply and/or

Card (SPC) issue/transfer/disposal and Property

the description/information Division/Unit

Semi-Expendable Property To record the acquisition, Accounting

Ledger Card (SPLC) description, custody, Division/Unit

impairment,

issue/transfer/disposal,

repair history, and other

information

37