allow them to assess the activities of the Municipal Government. Although these

are recorded as expenditures, the misclassification of certain expenses can still

affect the fairness of the presentation of each account and influence the

interpretation of users of financial information.

6.6 We recommended and the Municipal Accountant agreed to establish internal

accounting policies to identify whether a particular expenditure pertains to

Other Maintenance and Operating Expenses, Training Expenses, or

Extraordinary and Miscellaneous Expenses. We also recommended and the

Municipal Accountant agreed to, henceforth, strictly follow the Revised Chart

of Accounts, as required in COA Circular No. 2015-009.

Inventory accounts remained unchanged since CY 2018 - ₱524,237.55

7. Inventory accounts totaling ₱524,237.55 have remained unchanged since CY 2018

as the SSMI was not submitted by the Municipal Treasurer, which is inconsistent

with Sec. 121 of the NGAS Manual for LGUs, Vol. 1, resulting in unadjusted

inventory balances and causing a misstatement in both inventory and equity

accounts.

7.1 Section 121 of the NGAS Manual for LGUs, Vol. 1 requires the Municipal

Treasurer to consolidate the RIS weekly for supplies and materials issued using the

SSMI and submit the same to the Municipal Accountant. Based on the SSMI, a

journal entry voucher shall be prepared to record the expenditures using

appropriate expenditure accounts.

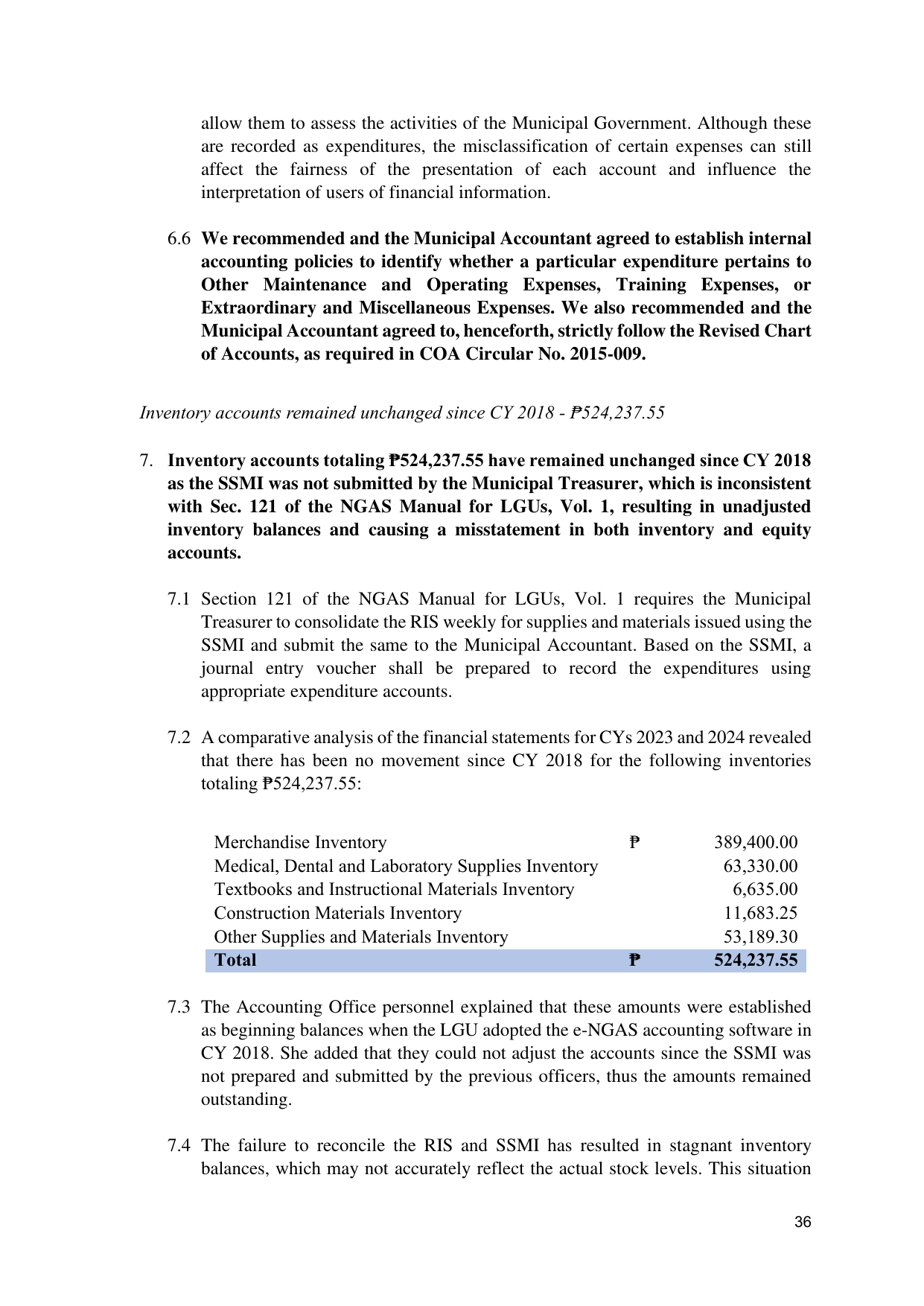

7.2 A comparative analysis of the financial statements for CYs 2023 and 2024 revealed

that there has been no movement since CY 2018 for the following inventories

totaling ₱524,237.55:

Merchandise Inventory ₱ 389,400.00

Medical, Dental and Laboratory Supplies Inventory 63,330.00

Textbooks and Instructional Materials Inventory 6,635.00

Construction Materials Inventory 11,683.25

Other Supplies and Materials Inventory 53,189.30

Total ₱ 524,237.55

7.3 The Accounting Office personnel explained that these amounts were established

as beginning balances when the LGU adopted the e-NGAS accounting software in

CY 2018. She added that they could not adjust the accounts since the SSMI was

not prepared and submitted by the previous officers, thus the amounts remained

outstanding.

7.4 The failure to reconcile the RIS and SSMI has resulted in stagnant inventory

balances, which may not accurately reflect the actual stock levels. This situation

36