7.12 We further recommended and it was agreed that, henceforth, the Municipal

Treasurer provide the Municipal Accountant at the beginning of each year

with a certified list of taxpayers with their amounts due and collectible for

the current year, to serve as her basis for recording the RPT and SET

Receivables in compliance with Sections 19(b), 20, and 84 of the NGAS

Manual for LGUs, Volume 1.

Biological Assets’ year end balances were not reported at fair value less costs to sell -

₱2,196,314.50

8. Biological Assets totaling ₱2,196,314.50 as of December 31, 2024, were not reported

at fair value less costs to sell, which is inconsistent with Paragraph 17 of

International Public Sector Accounting Standards (IPSAS) 27, rendering the

reported amount in the financial statements unreliable.

8.1 Paragraph 16 of IPSAS 27 requires that a biological asset be measured at its fair

value less costs to sell upon initial recognition and at each reporting date.

Furthermore, paragraph 30 of the same IPSAS states that a gain or loss arising on

initial recognition of a biological asset at fair value less costs to sell as well as

from a change in fair value less costs to sell of a biological asset shall be included

in surplus or deficit for the period in which it arises.

8.2 In relation to this, COA Circular No. 2016-004 dated September 30, 2016,

provides guidelines for the preparation of financial statements in line with the

adoption of the International Public Sector Accounting Standards (IPSAS) by

Local Government Units (LGUs). Section 4.5 of the circular specifies that the

Municipal Agriculturist is responsible for providing the Municipal Accountant

with an inventory of breeding stocks and other biological assets, along with the

prevailing market price for each item as of the reporting date and information on

the prevailing costs to sell these biological assets.

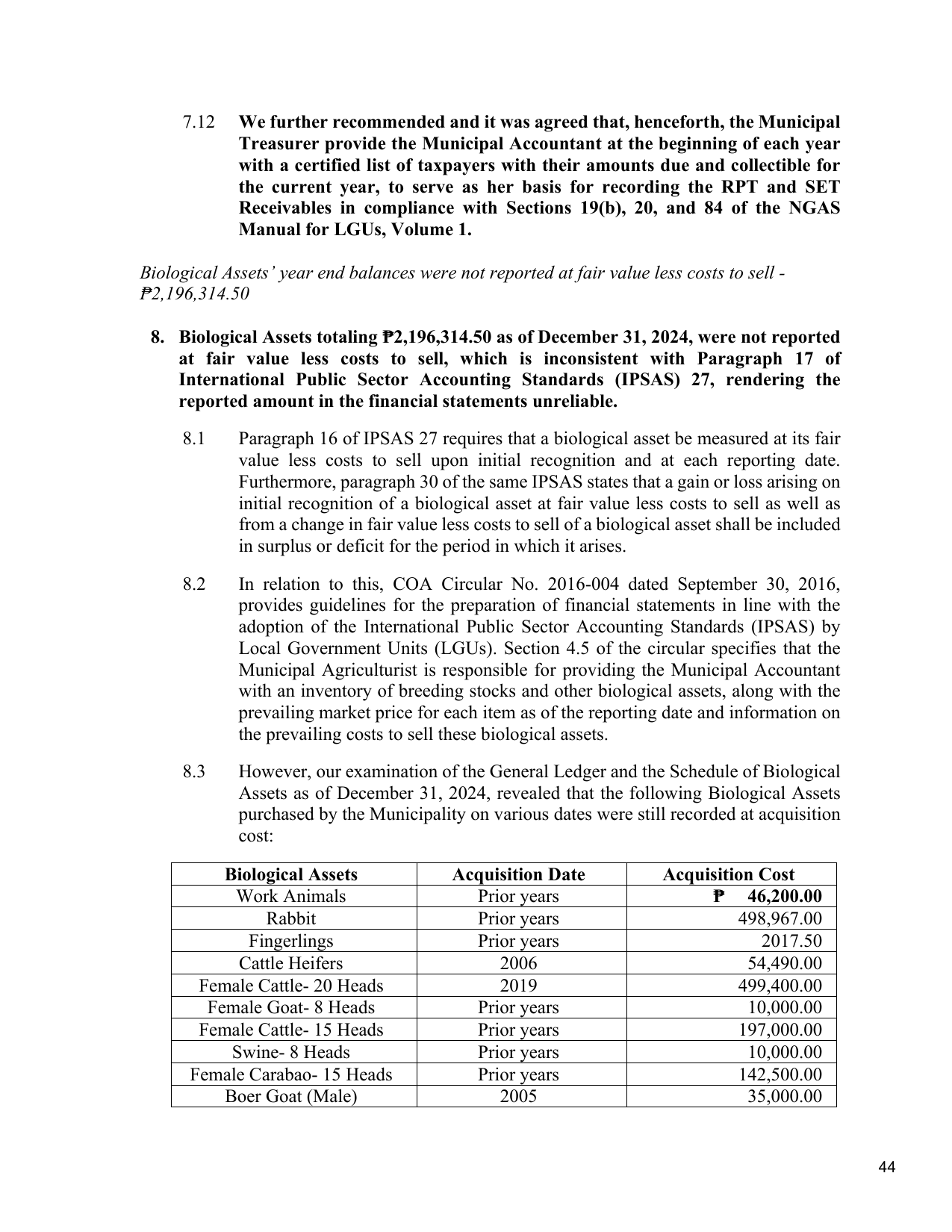

8.3 However, our examination of the General Ledger and the Schedule of Biological

Assets as of December 31, 2024, revealed that the following Biological Assets

purchased by the Municipality on various dates were still recorded at acquisition

cost:

Biological Assets Acquisition Date Acquisition Cost

Work Animals Prior years ₱ 46,200.00

Rabbit Prior years 498,967.00

Fingerlings Prior years 2017.50

Cattle Heifers 2006 54,490.00

Female Cattle- 20 Heads 2019 499,400.00

Female Goat- 8 Heads Prior years 10,000.00

Female Cattle- 15 Heads Prior years 197,000.00

Swine- 8 Heads Prior years 10,000.00

Female Carabao- 15 Heads Prior years 142,500.00

Boer Goat (Male) 2005 35,000.00

44