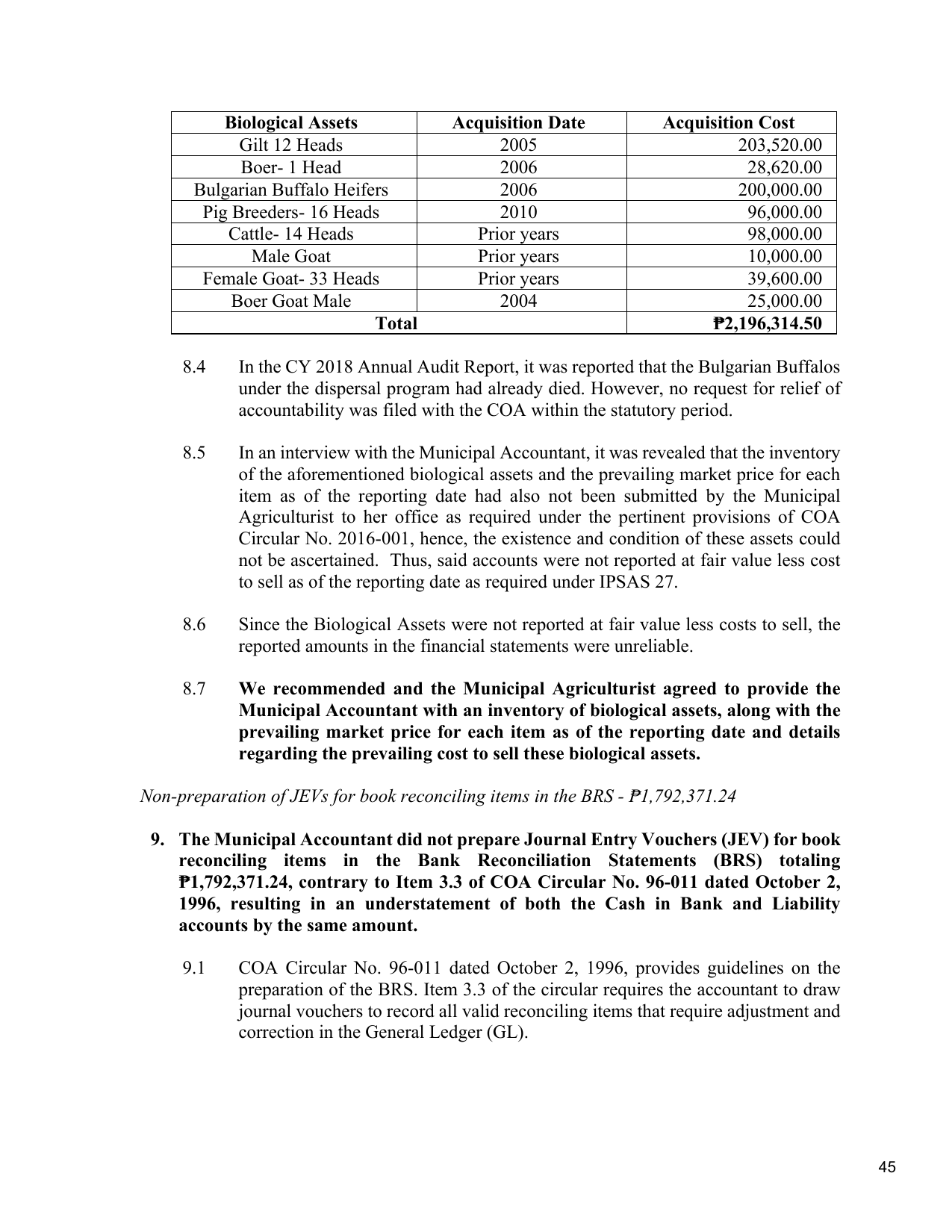

Biological Assets Acquisition Date Acquisition Cost

Gilt 12 Heads 2005 203,520.00

Boer- 1 Head 2006 28,620.00

Bulgarian Buffalo Heifers 2006 200,000.00

Pig Breeders- 16 Heads 2010 96,000.00

Cattle- 14 Heads Prior years 98,000.00

Male Goat Prior years 10,000.00

Female Goat- 33 Heads Prior years 39,600.00

Boer Goat Male 2004 25,000.00

Total ₱2,196,314.50

8.4 In the CY 2018 Annual Audit Report, it was reported that the Bulgarian Buffalos

under the dispersal program had already died. However, no request for relief of

accountability was filed with the COA within the statutory period.

8.5 In an interview with the Municipal Accountant, it was revealed that the inventory

of the aforementioned biological assets and the prevailing market price for each

item as of the reporting date had also not been submitted by the Municipal

Agriculturist to her office as required under the pertinent provisions of COA

Circular No. 2016-001, hence, the existence and condition of these assets could

not be ascertained. Thus, said accounts were not reported at fair value less cost

to sell as of the reporting date as required under IPSAS 27.

8.6 Since the Biological Assets were not reported at fair value less costs to sell, the

reported amounts in the financial statements were unreliable.

8.7 We recommended and the Municipal Agriculturist agreed to provide the

Municipal Accountant with an inventory of biological assets, along with the

prevailing market price for each item as of the reporting date and details

regarding the prevailing cost to sell these biological assets.

Non-preparation of JEVs for book reconciling items in the BRS - ₱1,792,371.24

9. The Municipal Accountant did not prepare Journal Entry Vouchers (JEV) for book

reconciling items in the Bank Reconciliation Statements (BRS) totaling

₱1,792,371.24, contrary to Item 3.3 of COA Circular No. 96-011 dated October 2,

1996, resulting in an understatement of both the Cash in Bank and Liability

accounts by the same amount.

9.1 COA Circular No. 96-011 dated October 2, 1996, provides guidelines on the

preparation of the BRS. Item 3.3 of the circular requires the accountant to draw

journal vouchers to record all valid reconciling items that require adjustment and

correction in the General Ledger (GL).

45