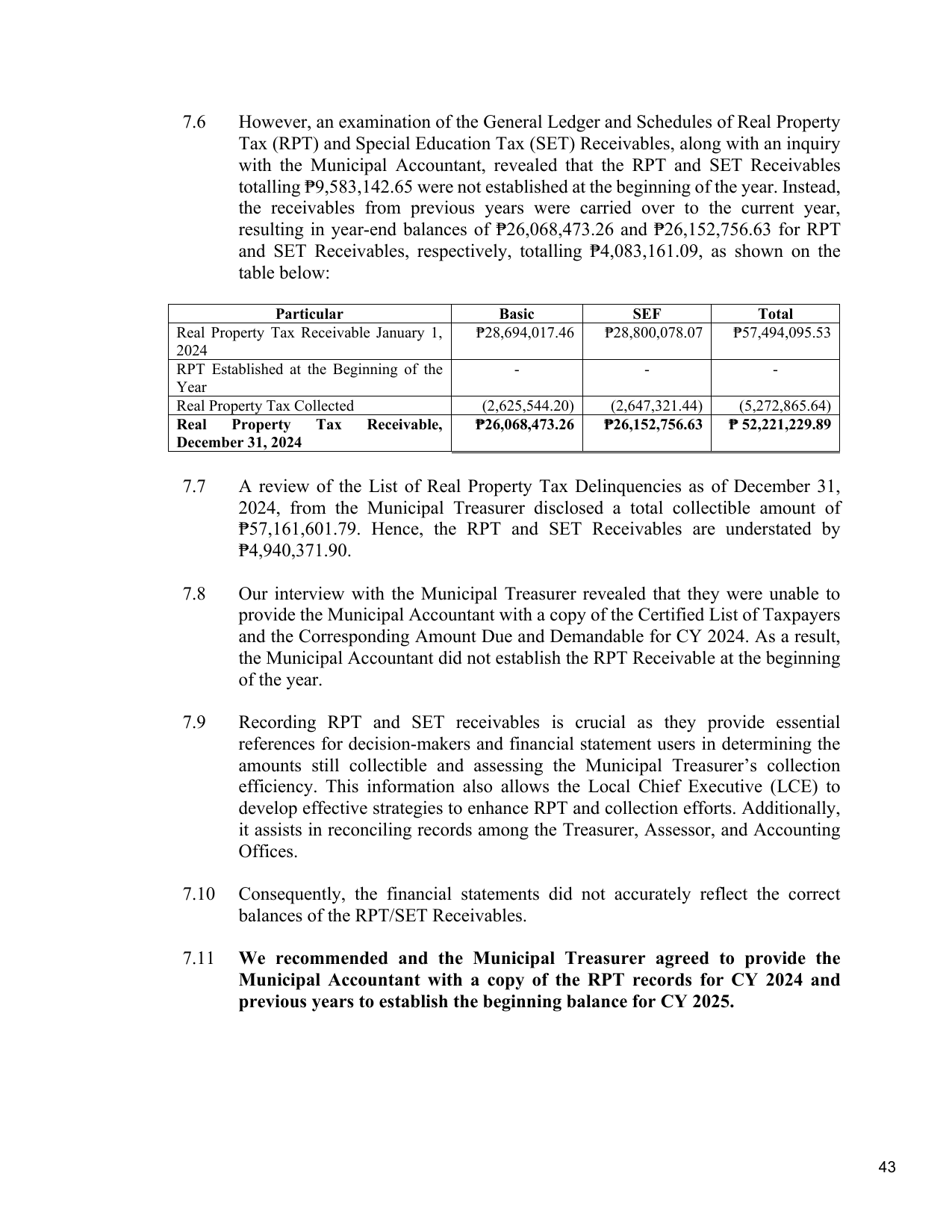

7.6 However, an examination of the General Ledger and Schedules of Real Property

Tax (RPT) and Special Education Tax (SET) Receivables, along with an inquiry

with the Municipal Accountant, revealed that the RPT and SET Receivables

totalling ₱9,583,142.65 were not established at the beginning of the year. Instead,

the receivables from previous years were carried over to the current year,

resulting in year-end balances of ₱26,068,473.26 and ₱26,152,756.63 for RPT

and SET Receivables, respectively, totalling ₱4,083,161.09, as shown on the

table below:

Particular Basic SEF Total

Real Property Tax Receivable January 1, ₱28,694,017.46 ₱28,800,078.07 ₱57,494,095.53

2024

RPT Established at the Beginning of the - - -

Year

Real Property Tax Collected (2,625,544.20) (2,647,321.44) (5,272,865.64)

Real Property Tax Receivable, ₱26,068,473.26 ₱26,152,756.63 ₱ 52,221,229.89

December 31, 2024

7.7 A review of the List of Real Property Tax Delinquencies as of December 31,

2024, from the Municipal Treasurer disclosed a total collectible amount of

₱57,161,601.79. Hence, the RPT and SET Receivables are understated by

₱4,940,371.90.

7.8 Our interview with the Municipal Treasurer revealed that they were unable to

provide the Municipal Accountant with a copy of the Certified List of Taxpayers

and the Corresponding Amount Due and Demandable for CY 2024. As a result,

the Municipal Accountant did not establish the RPT Receivable at the beginning

of the year.

7.9 Recording RPT and SET receivables is crucial as they provide essential

references for decision-makers and financial statement users in determining the

amounts still collectible and assessing the Municipal Treasurer’s collection

efficiency. This information also allows the Local Chief Executive (LCE) to

develop effective strategies to enhance RPT and collection efforts. Additionally,

it assists in reconciling records among the Treasurer, Assessor, and Accounting

Offices.

7.10 Consequently, the financial statements did not accurately reflect the correct

balances of the RPT/SET Receivables.

7.11 We recommended and the Municipal Treasurer agreed to provide the

Municipal Accountant with a copy of the RPT records for CY 2024 and

previous years to establish the beginning balance for CY 2025.

43