7.2 Furthermore, Sections 20 and 84 thereof provides that the Real Property Tax

Receivables/Special Education Tax Receivables shall be established at the

beginning of the year based on the Real Property Tax Account

Register/Taxpayer’s index card. At the beginning of the year, the Treasurer shall

furnish the Chief Accountant with a duly certified list showing the name of

taxpayers and the amount due and collectible for the year. Based on the list, the

Chief Accountant shall draw a Journal Entry Voucher (JEV) to record the debit

to Real Property Tax Receivable/Special Education Tax Receivable and credit to

the Deferred Real Property Tax Income/Deferred Special Education Tax Income.

7.3 Upon collection of Real Property Taxes during the year, income is recognized by

crediting Real Property Tax Income while the Deferred Real Property Tax

Income/Deferred Special Education Tax Income is debited. The share of the

Province and Barangay shall also be credited to Due to LGUs.

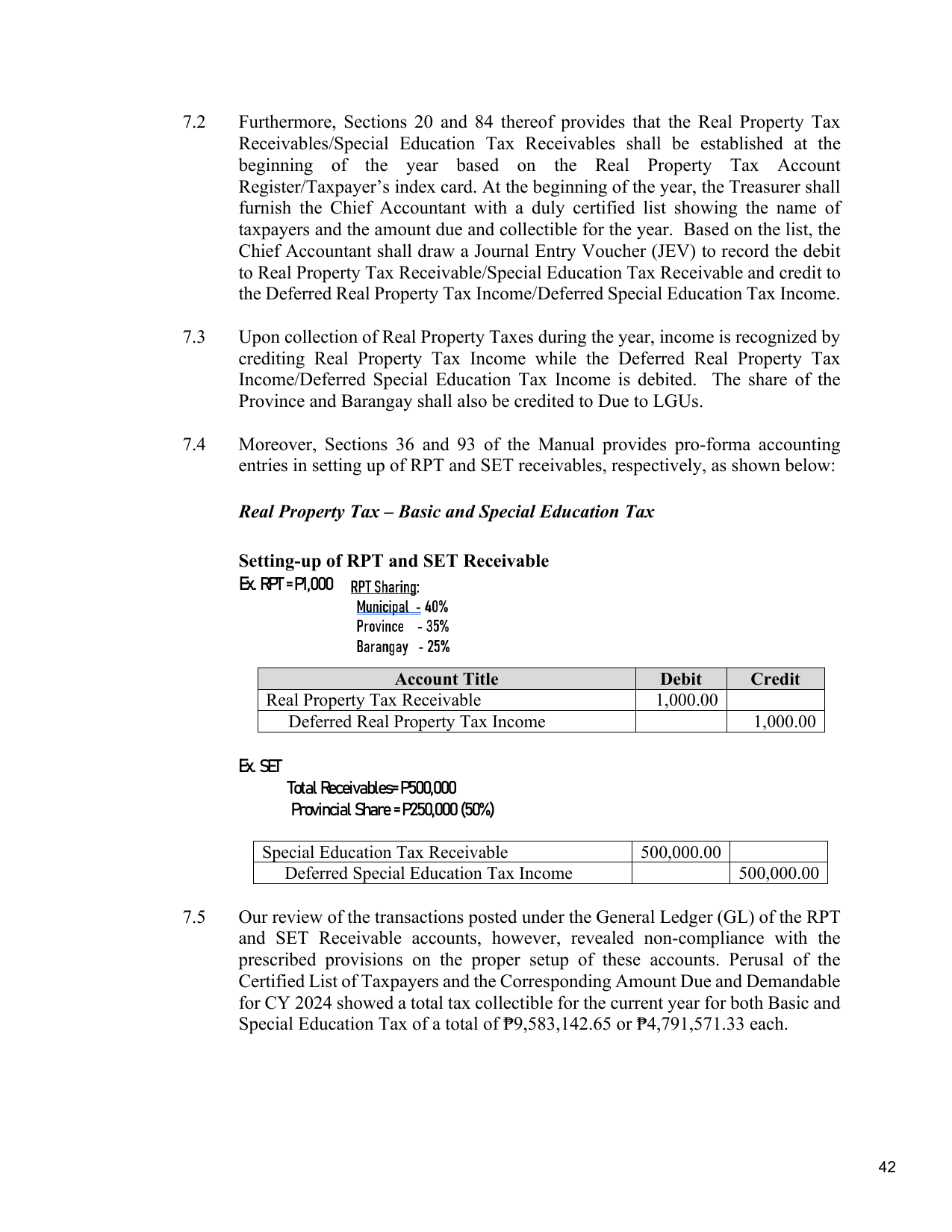

7.4 Moreover, Sections 36 and 93 of the Manual provides pro-forma accounting

entries in setting up of RPT and SET receivables, respectively, as shown below:

Real Property Tax – Basic and Special Education Tax

Setting-up of RPT and SET Receivable

Ex. RPT =P1,000

Account Title Debit Credit

Real Property Tax Receivable 1,000.00

Deferred Real Property Tax Income 1,000.00

Ex. SET

Total Receivables=P500,000

Provincial Share =P250,000 (50%)

Special Education Tax Receivable 500,000.00

Deferred Special Education Tax Income 500,000.00

7.5 Our review of the transactions posted under the General Ledger (GL) of the RPT

and SET Receivable accounts, however, revealed non-compliance with the

prescribed provisions on the proper setup of these accounts. Perusal of the

Certified List of Taxpayers and the Corresponding Amount Due and Demandable

for CY 2024 showed a total tax collectible for the current year for both Basic and

Special Education Tax of a total of ₱9,583,142.65 or ₱4,791,571.33 each.

42