b. Conduct a comprehensive review of all PPE items to identify assets that

have not been depreciated and ensure that depreciation is

systematically applied in accordance with IPSAS 45, specifically

Paragraphs 26 and 41. This includes recognizing depreciation for each

significant component of an asset, where applicable; and

c. Compute the appropriate depreciation expense for the previously

omitted PPE items and recognize the corresponding accumulated

depreciation to correct the misstatement. The necessary adjusting

journal entries should be prepared and recorded to reflect the accurate

net book value of the affected assets and to eliminate the overstatement

in both the asset and equity accounts.

Cash receipts for fund transfers from the National Government not reported in the Statement

of Cash Flows - ₱65,332,120.00

3. Cash receipts for fund transfers from the National Government, amounting to

₱65,332,120.00, were not reported in the Statement of Cash Flows. Instead, these

amounts were deducted from the payments to suppliers, which is inconsistent with

Paragraphs 18, 19, and 22 of International Public Sector Accounting Standard

(IPSAS) 2, leading to inaccurate and unreliable representations of cash inflows and

outflows under the Municipality’s operating activities.

3.1 Paragraph 18 of IPSAS 2 states that the cash flow statement must report cash

flows during the period, classified by operating, investing, and financing

activities. Paragraph 19 further clarifies that an entity presents its cash flows from

operating, investing, and financing activities in a manner that is most appropriate

for its operations. Classification by activity provides information that allows users

to assess the impact of those activities on the entity’s financial position, and the

amount of cash and cash equivalents. This information may also be used to

evaluate the relationships among those activities. Paragraph 22 of the same

IPSAS provides examples of cash flows classified under operating activities.

These include, among others, cash receipts from grants or transfers received from

the National Government, as well as cash payments made to suppliers for goods

and services.

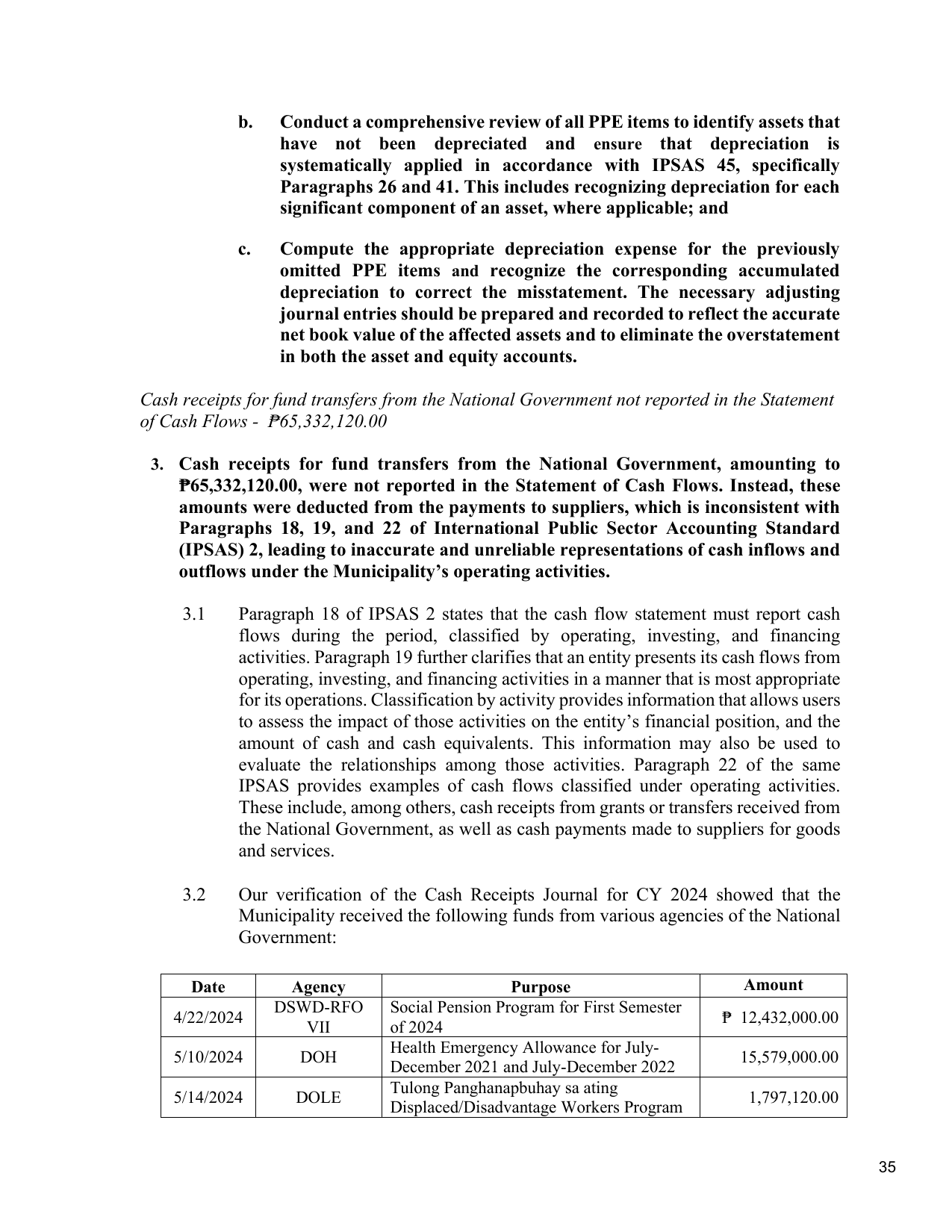

3.2 Our verification of the Cash Receipts Journal for CY 2024 showed that the

Municipality received the following funds from various agencies of the National

Government:

Date Agency Purpose Amount

DSWD-RFO Social Pension Program for First Semester

4/22/2024 ₱ 12,432,000.00

VII of 2024

Health Emergency Allowance for July-

5/10/2024 DOH 15,579,000.00

December 2021 and July-December 2022

Tulong Panghanapbuhay sa ating

5/14/2024 DOLE 1,797,120.00

Displaced/Disadvantage Workers Program

35