Depreciation on PPE assets were not recognized

2. Items of PPE with a total cost of ₱106,188,435.86 were not provided with

depreciation, contrary to Paragraph 26 of the International Public Sector

Accounting Standard (IPSAS) 45, hence, the municipality’s asset and equity

accounts were overstated by the amount of depreciation that should have been

applied to these assets.

2.1 IPSAS 45 provides guidance on measuring property, plant, and equipment.

According to paragraph 26, after recognizing an item, it should be recorded at its

historical cost, minus any accumulated depreciation and impairment losses.

Paragraph 41 of the same IPSAS also requires that any significant part of an item

of PPE should be depreciated separately, based on its total cost or value.

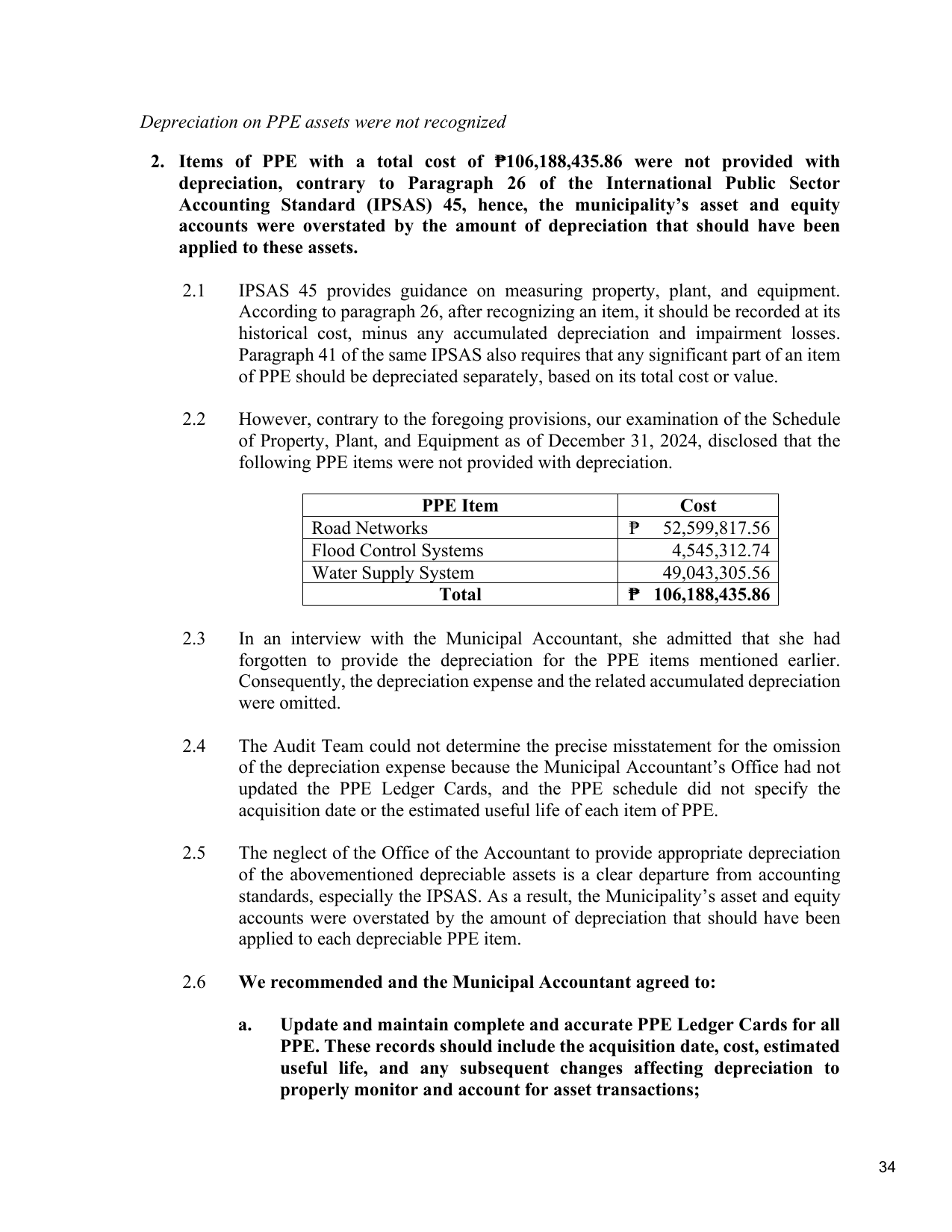

2.2 However, contrary to the foregoing provisions, our examination of the Schedule

of Property, Plant, and Equipment as of December 31, 2024, disclosed that the

following PPE items were not provided with depreciation.

PPE Item Cost

Road Networks ₱ 52,599,817.56

Flood Control Systems 4,545,312.74

Water Supply System 49,043,305.56

Total ₱ 106,188,435.86

2.3 In an interview with the Municipal Accountant, she admitted that she had

forgotten to provide the depreciation for the PPE items mentioned earlier.

Consequently, the depreciation expense and the related accumulated depreciation

were omitted.

2.4 The Audit Team could not determine the precise misstatement for the omission

of the depreciation expense because the Municipal Accountant’s Office had not

updated the PPE Ledger Cards, and the PPE schedule did not specify the

acquisition date or the estimated useful life of each item of PPE.

2.5 The neglect of the Office of the Accountant to provide appropriate depreciation

of the abovementioned depreciable assets is a clear departure from accounting

standards, especially the IPSAS. As a result, the Municipality’s asset and equity

accounts were overstated by the amount of depreciation that should have been

applied to each depreciable PPE item.

2.6 We recommended and the Municipal Accountant agreed to:

a. Update and maintain complete and accurate PPE Ledger Cards for all

PPE. These records should include the acquisition date, cost, estimated

useful life, and any subsequent changes affecting depreciation to

properly monitor and account for asset transactions;

34