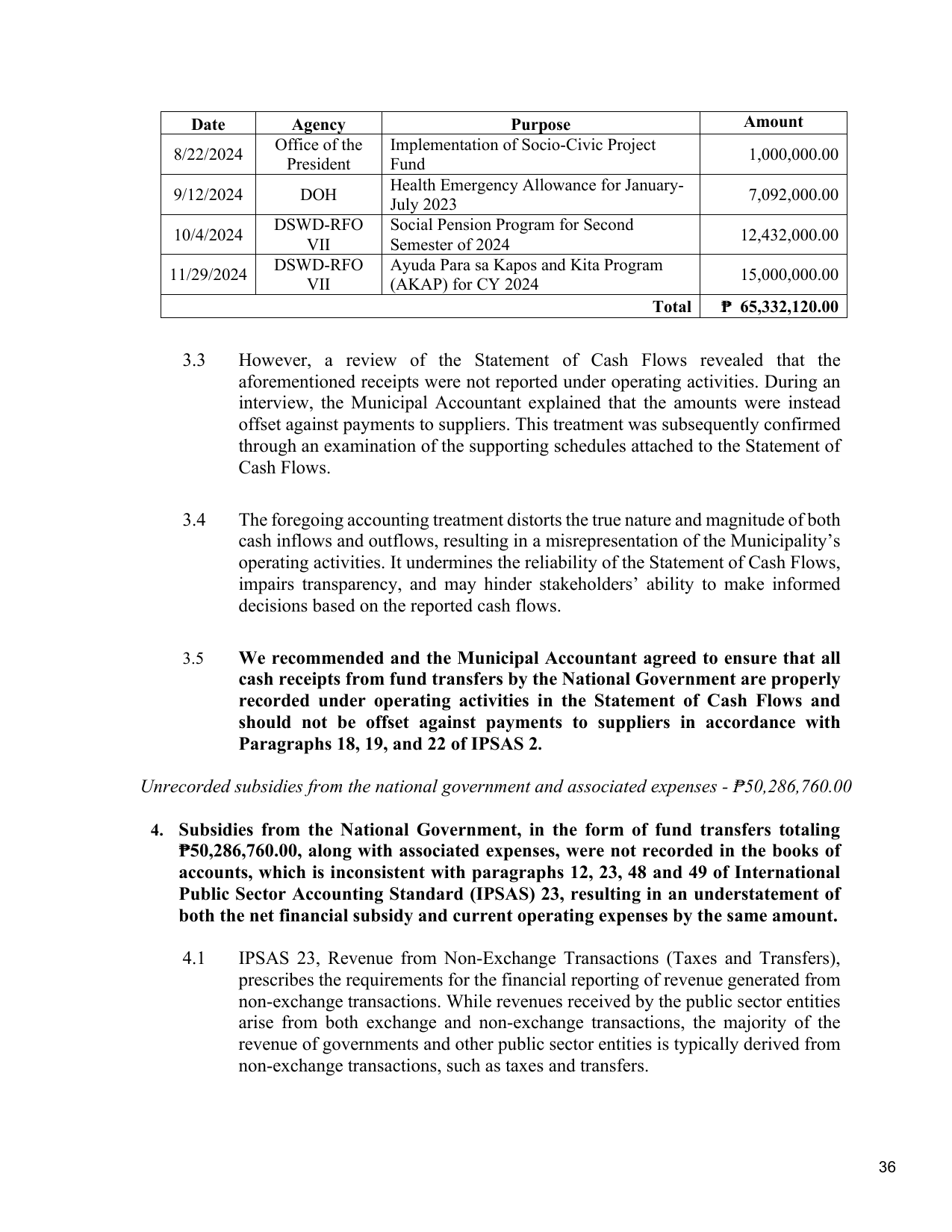

Date Agency Purpose Amount

Office of the Implementation of Socio-Civic Project

8/22/2024 1,000,000.00

President Fund

Health Emergency Allowance for January-

9/12/2024 DOH 7,092,000.00

July 2023

DSWD-RFO Social Pension Program for Second

10/4/2024 12,432,000.00

VII Semester of 2024

DSWD-RFO Ayuda Para sa Kapos and Kita Program

11/29/2024 15,000,000.00

VII (AKAP) for CY 2024

Total ₱ 65,332,120.00

3.3 However, a review of the Statement of Cash Flows revealed that the

aforementioned receipts were not reported under operating activities. During an

interview, the Municipal Accountant explained that the amounts were instead

offset against payments to suppliers. This treatment was subsequently confirmed

through an examination of the supporting schedules attached to the Statement of

Cash Flows.

3.4 The foregoing accounting treatment distorts the true nature and magnitude of both

cash inflows and outflows, resulting in a misrepresentation of the Municipality’s

operating activities. It undermines the reliability of the Statement of Cash Flows,

impairs transparency, and may hinder stakeholders’ ability to make informed

decisions based on the reported cash flows.

3.5 We recommended and the Municipal Accountant agreed to ensure that all

cash receipts from fund transfers by the National Government are properly

recorded under operating activities in the Statement of Cash Flows and

should not be offset against payments to suppliers in accordance with

Paragraphs 18, 19, and 22 of IPSAS 2.

Unrecorded subsidies from the national government and associated expenses - ₱50,286,760.00

4. Subsidies from the National Government, in the form of fund transfers totaling

₱50,286,760.00, along with associated expenses, were not recorded in the books of

accounts, which is inconsistent with paragraphs 12, 23, 48 and 49 of International

Public Sector Accounting Standard (IPSAS) 23, resulting in an understatement of

both the net financial subsidy and current operating expenses by the same amount.

4.1 IPSAS 23, Revenue from Non-Exchange Transactions (Taxes and Transfers),

prescribes the requirements for the financial reporting of revenue generated from

non-exchange transactions. While revenues received by the public sector entities

arise from both exchange and non-exchange transactions, the majority of the

revenue of governments and other public sector entities is typically derived from

non-exchange transactions, such as taxes and transfers.

36