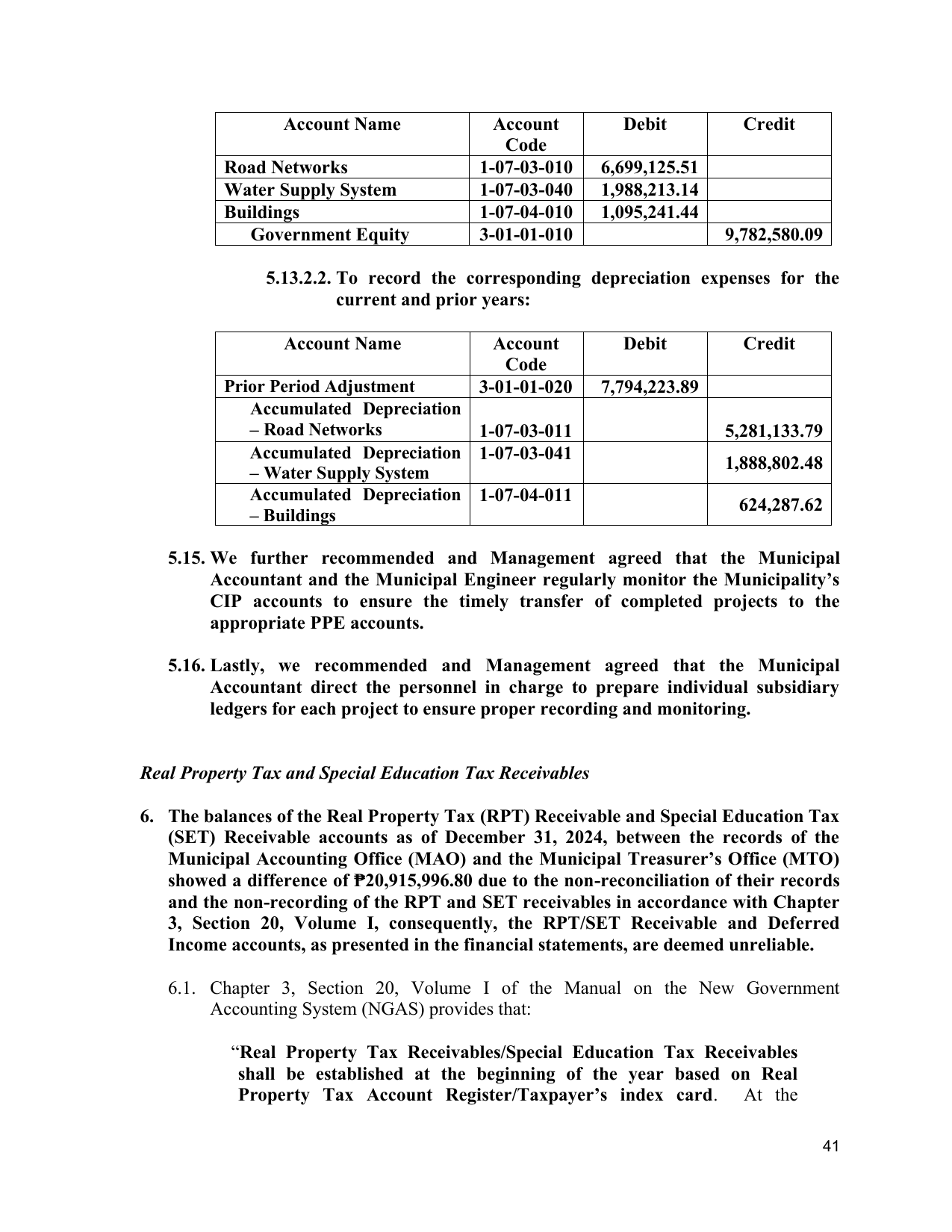

Account Name Account Debit Credit

Code

Road Networks 1-07-03-010 6,699,125.51

Water Supply System 1-07-03-040 1,988,213.14

Buildings 1-07-04-010 1,095,241.44

Government Equity 3-01-01-010 9,782,580.09

5.13.2.2. To record the corresponding depreciation expenses for the

current and prior years:

Account Name Account Debit Credit

Code

Prior Period Adjustment 3-01-01-020 7,794,223.89

Accumulated Depreciation

– Road Networks 1-07-03-011 5,281,133.79

Accumulated Depreciation 1-07-03-041

1,888,802.48

– Water Supply System

Accumulated Depreciation 1-07-04-011

624,287.62

– Buildings

5.15. We further recommended and Management agreed that the Municipal

Accountant and the Municipal Engineer regularly monitor the Municipality’s

CIP accounts to ensure the timely transfer of completed projects to the

appropriate PPE accounts.

5.16. Lastly, we recommended and Management agreed that the Municipal

Accountant direct the personnel in charge to prepare individual subsidiary

ledgers for each project to ensure proper recording and monitoring.

Real Property Tax and Special Education Tax Receivables

6. The balances of the Real Property Tax (RPT) Receivable and Special Education Tax

(SET) Receivable accounts as of December 31, 2024, between the records of the

Municipal Accounting Office (MAO) and the Municipal Treasurer’s Office (MTO)

showed a difference of ₱20,915,996.80 due to the non-reconciliation of their records

and the non-recording of the RPT and SET receivables in accordance with Chapter

3, Section 20, Volume I, consequently, the RPT/SET Receivable and Deferred

Income accounts, as presented in the financial statements, are deemed unreliable.

6.1. Chapter 3, Section 20, Volume I of the Manual on the New Government

Accounting System (NGAS) provides that:

“Real Property Tax Receivables/Special Education Tax Receivables

shall be established at the beginning of the year based on Real

Property Tax Account Register/Taxpayer’s index card. At the

41