Water Supply Systems, and Buildings were understated by ₱6,699,125.51,

₱1,988,213.14, and ₱1,095,241.44, respectively, totaling ₱9,782,580.09.

5.12. Moreover, the non-recording of the asset accounts in the GF books resulted in the

non-recognition of related Depreciation Expenses. Thus, the corresponding

Accumulated Depreciation accounts were understated while the surplus account

was overstated by an estimated amount totaling ₱7,794,223.89 for the period.

Collectively, these deficiencies have adversely affected the accuracy and fair

presentation of these account balances in the financial statements.

5.13. This observation was communicated to Management through Audit Observation

Memorandum No. 2025-03(2024)-Manjuyod dated April 25, 2025.

5.14. We recommended and Management agreed that the Municipal Accountant

prepare the following entries in the Trust Fund and General Fund books as

follows:

5.13.1. Trust Fund Books:

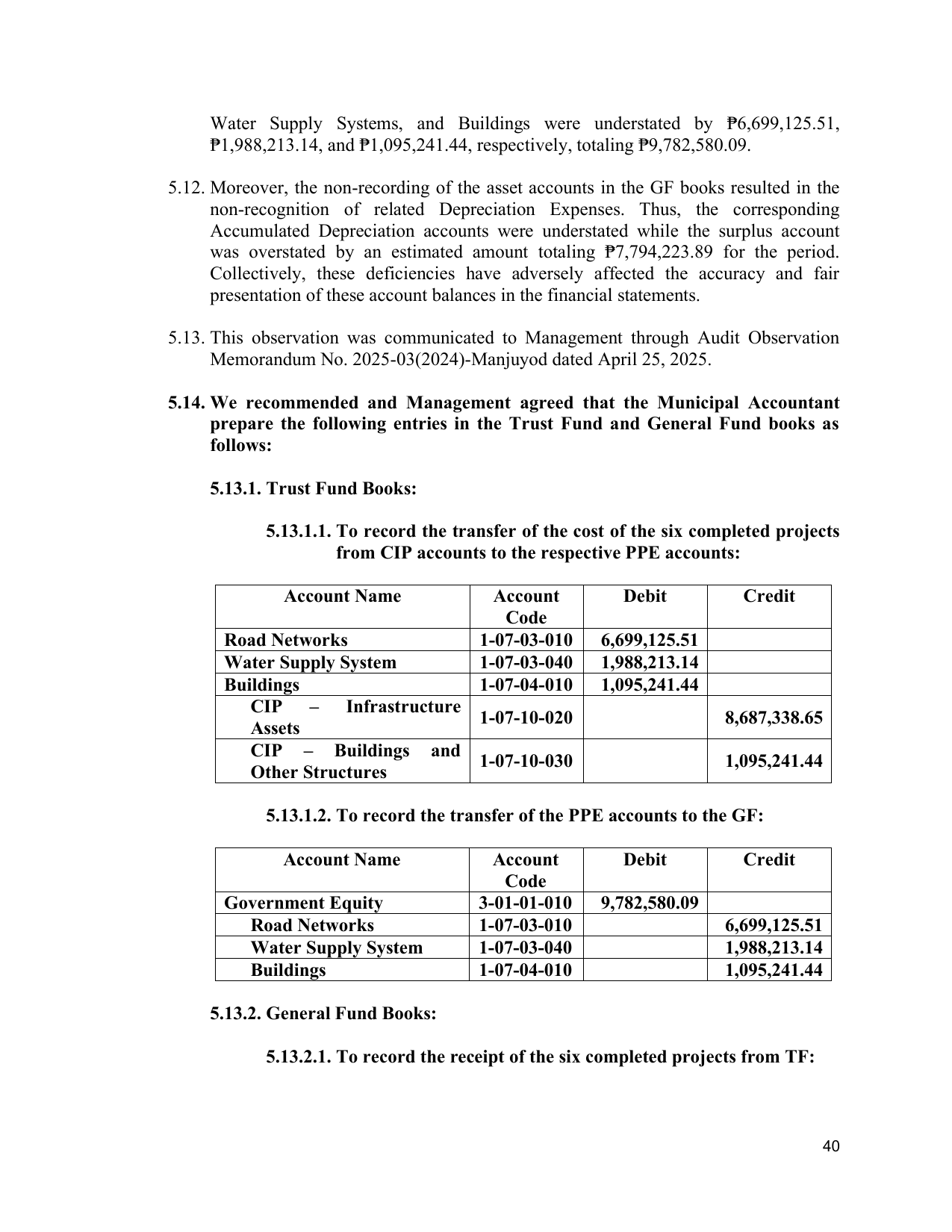

5.13.1.1. To record the transfer of the cost of the six completed projects

from CIP accounts to the respective PPE accounts:

Account Name Account Debit Credit

Code

Road Networks 1-07-03-010 6,699,125.51

Water Supply System 1-07-03-040 1,988,213.14

Buildings 1-07-04-010 1,095,241.44

CIP – Infrastructure

1-07-10-020 8,687,338.65

Assets

CIP – Buildings and

1-07-10-030 1,095,241.44

Other Structures

5.13.1.2. To record the transfer of the PPE accounts to the GF:

Account Name Account Debit Credit

Code

Government Equity 3-01-01-010 9,782,580.09

Road Networks 1-07-03-010 6,699,125.51

Water Supply System 1-07-03-040 1,988,213.14

Buildings 1-07-04-010 1,095,241.44

5.13.2. General Fund Books:

5.13.2.1. To record the receipt of the six completed projects from TF:

40