beginning of the year, the Treasurer shall furnish the Chief Accountant of

a duly certified list showing the name of taxpayers and the amount due

and collectible for the year. Based on the list, the Chief Accountant shall

draw a Journal Entry Voucher (JEV) to record the debit to Real Property

Tax Receivable/Special Education Tax Receivable and crediting to

Deferred Real Property Tax Income/Deferred Special Education Tax

Income.” (Emphasis ours)

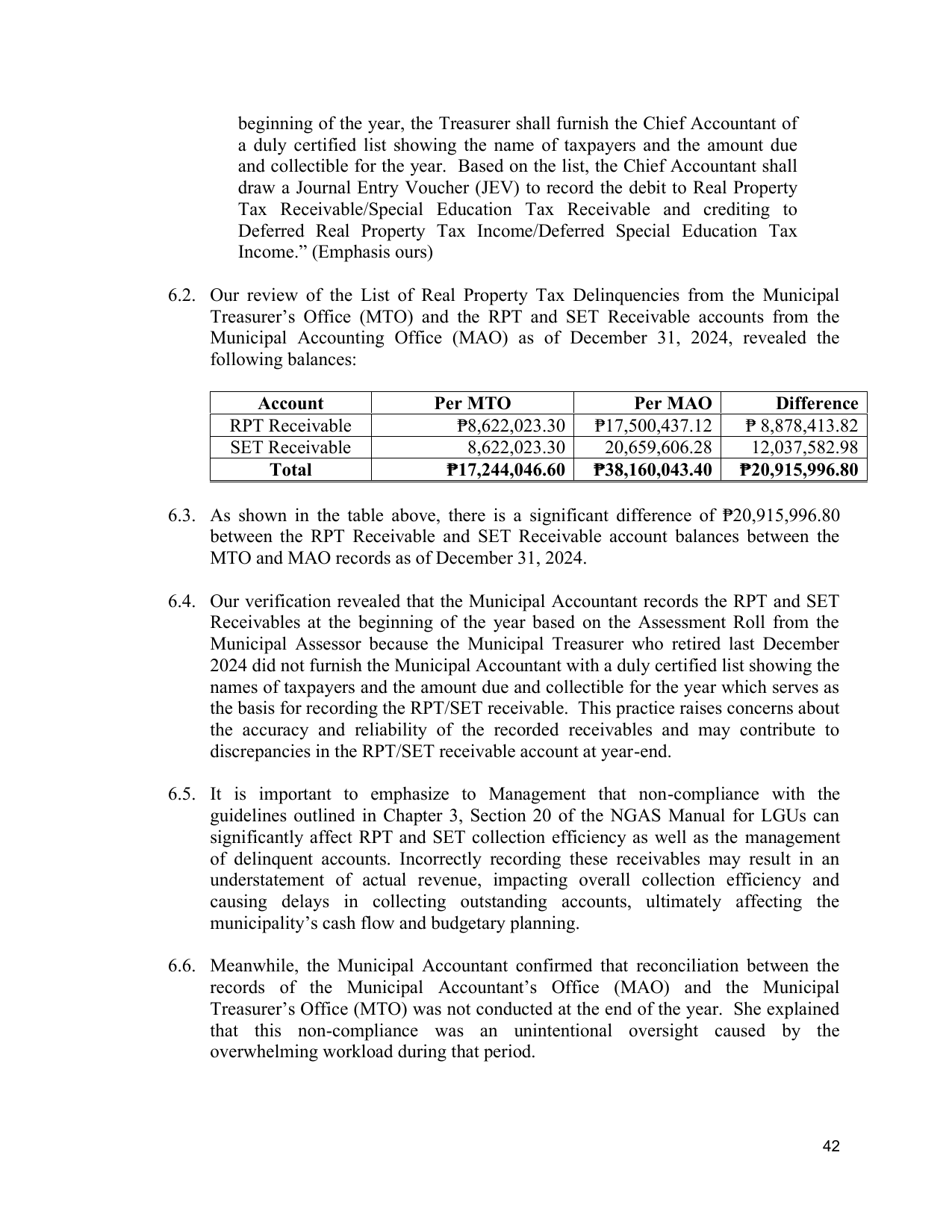

6.2. Our review of the List of Real Property Tax Delinquencies from the Municipal

Treasurer’s Office (MTO) and the RPT and SET Receivable accounts from the

Municipal Accounting Office (MAO) as of December 31, 2024, revealed the

following balances:

Account Per MTO Per MAO Difference

RPT Receivable ₱8,622,023.30 ₱17,500,437.12 ₱ 8,878,413.82

SET Receivable 8,622,023.30 20,659,606.28 12,037,582.98

Total ₱17,244,046.60 ₱38,160,043.40 ₱20,915,996.80

6.3. As shown in the table above, there is a significant difference of ₱20,915,996.80

between the RPT Receivable and SET Receivable account balances between the

MTO and MAO records as of December 31, 2024.

6.4. Our verification revealed that the Municipal Accountant records the RPT and SET

Receivables at the beginning of the year based on the Assessment Roll from the

Municipal Assessor because the Municipal Treasurer who retired last December

2024 did not furnish the Municipal Accountant with a duly certified list showing the

names of taxpayers and the amount due and collectible for the year which serves as

the basis for recording the RPT/SET receivable. This practice raises concerns about

the accuracy and reliability of the recorded receivables and may contribute to

discrepancies in the RPT/SET receivable account at year-end.

6.5. It is important to emphasize to Management that non-compliance with the

guidelines outlined in Chapter 3, Section 20 of the NGAS Manual for LGUs can

significantly affect RPT and SET collection efficiency as well as the management

of delinquent accounts. Incorrectly recording these receivables may result in an

understatement of actual revenue, impacting overall collection efficiency and

causing delays in collecting outstanding accounts, ultimately affecting the

municipality’s cash flow and budgetary planning.

6.6. Meanwhile, the Municipal Accountant confirmed that reconciliation between the

records of the Municipal Accountant’s Office (MAO) and the Municipal

Treasurer’s Office (MTO) was not conducted at the end of the year. She explained

that this non-compliance was an unintentional oversight caused by the

overwhelming workload during that period.

42