No. of Years

Date of

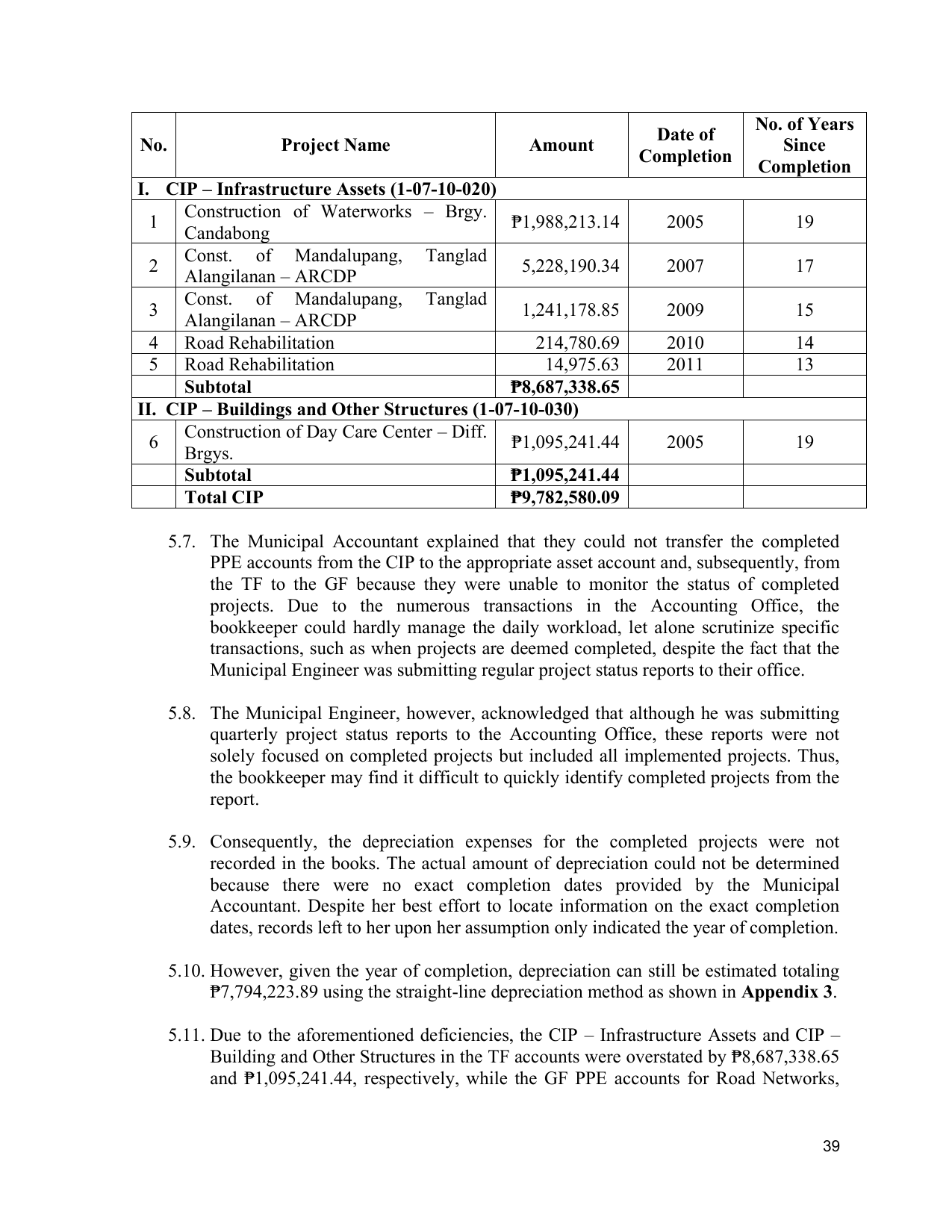

No. Project Name Amount Since

Completion

Completion

I. CIP – Infrastructure Assets (1-07-10-020)

Construction of Waterworks – Brgy.

1 ₱1,988,213.14 2005 19

Candabong

Const. of Mandalupang, Tanglad

2 5,228,190.34 2007 17

Alangilanan – ARCDP

Const. of Mandalupang, Tanglad

3 1,241,178.85 2009 15

Alangilanan – ARCDP

4 Road Rehabilitation 214,780.69 2010 14

5 Road Rehabilitation 14,975.63 2011 13

Subtotal ₱8,687,338.65

II. CIP – Buildings and Other Structures (1-07-10-030)

Construction of Day Care Center – Diff.

6 ₱1,095,241.44 2005 19

Brgys.

Subtotal ₱1,095,241.44

Total CIP ₱9,782,580.09

5.7. The Municipal Accountant explained that they could not transfer the completed

PPE accounts from the CIP to the appropriate asset account and, subsequently, from

the TF to the GF because they were unable to monitor the status of completed

projects. Due to the numerous transactions in the Accounting Office, the

bookkeeper could hardly manage the daily workload, let alone scrutinize specific

transactions, such as when projects are deemed completed, despite the fact that the

Municipal Engineer was submitting regular project status reports to their office.

5.8. The Municipal Engineer, however, acknowledged that although he was submitting

quarterly project status reports to the Accounting Office, these reports were not

solely focused on completed projects but included all implemented projects. Thus,

the bookkeeper may find it difficult to quickly identify completed projects from the

report.

5.9. Consequently, the depreciation expenses for the completed projects were not

recorded in the books. The actual amount of depreciation could not be determined

because there were no exact completion dates provided by the Municipal

Accountant. Despite her best effort to locate information on the exact completion

dates, records left to her upon her assumption only indicated the year of completion.

5.10. However, given the year of completion, depreciation can still be estimated totaling

₱7,794,223.89 using the straight-line depreciation method as shown in Appendix 3.

5.11. Due to the aforementioned deficiencies, the CIP – Infrastructure Assets and CIP –

Building and Other Structures in the TF accounts were overstated by ₱8,687,338.65

and ₱1,095,241.44, respectively, while the GF PPE accounts for Road Networks,

39