2.10. Finally, the current liabilities were overstated by ₱89,158,886.28 and the non-

current liabilities were understated by the same amount, thereby affecting the fair

presentation and reliability of the financial statements as of year-end.

2.11. This observation was communicated to Management through Audit Observation

Memorandum No. 2025-04(2024)-Manjuyod dated April 25, 2025.

2.12. We recommended and Management agreed that the Municipal Accountant

thoroughly review and reclassify the Loans Payable account in accordance

with Section 80 of IPSAS 1 – Presentation of Financial Statements, by properly

segregating the current and non-current portions based on the loan

amortization schedules. Specifically, only the portion of the loan due within

twelve months from the reporting date should be classified under Current

Liabilities, while the remaining balance must be presented under Non-Current

Liabilities.

Cash – Local Treasury

3. Cash – Local Treasury account balance per general ledger in the total amount of

₱1,292,249.00 as of December 31, 2024, does not reconcile with the cashbook

balance of ₱258,739.86, resulting in an unreconciled difference of ₱1,033,509.14

which is not in consonance with Paragraph 27 of IPSAS 1, thus affecting the fair

presentation of the recorded balance of the Cash account in the financial statements.

3.1. Paragraph 27 of the International Public Sector Accounting Standards (IPSAS) 1,

provides that financial statements shall present fairly the financial position,

financial performance, and cash flows of an entity. Fair presentation requires the

faithful representation of the effects of transactions, other events and conditions in

accordance with the definitions and recognition criteria for assets, liabilities,

revenue and expenses set out in IPSASs.

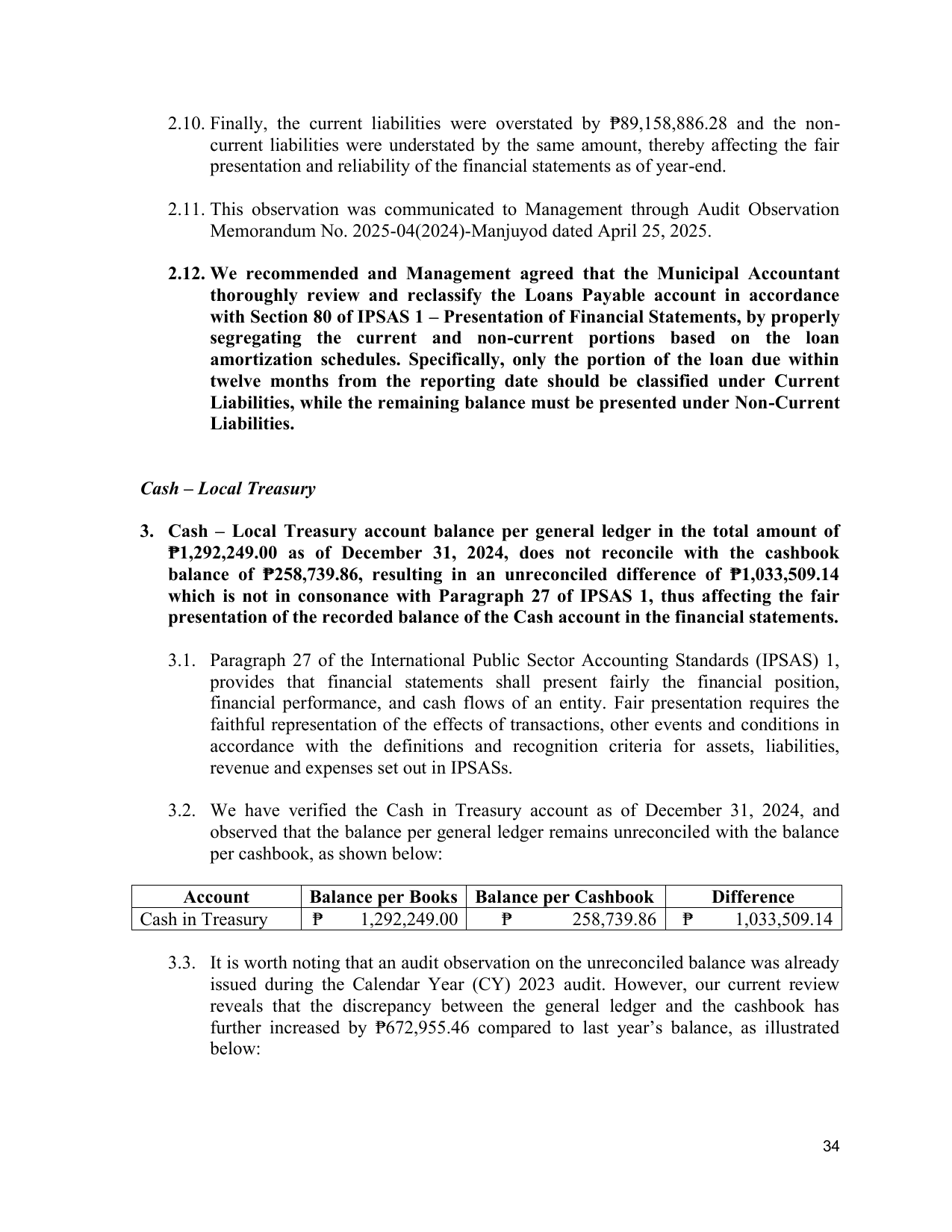

3.2. We have verified the Cash in Treasury account as of December 31, 2024, and

observed that the balance per general ledger remains unreconciled with the balance

per cashbook, as shown below:

Account Balance per Books Balance per Cashbook Difference

Cash in Treasury ₱ 1,292,249.00 ₱ 258,739.86 ₱ 1,033,509.14

3.3. It is worth noting that an audit observation on the unreconciled balance was already

issued during the Calendar Year (CY) 2023 audit. However, our current review

reveals that the discrepancy between the general ledger and the cashbook has

further increased by ₱672,955.46 compared to last year’s balance, as illustrated

below:

34