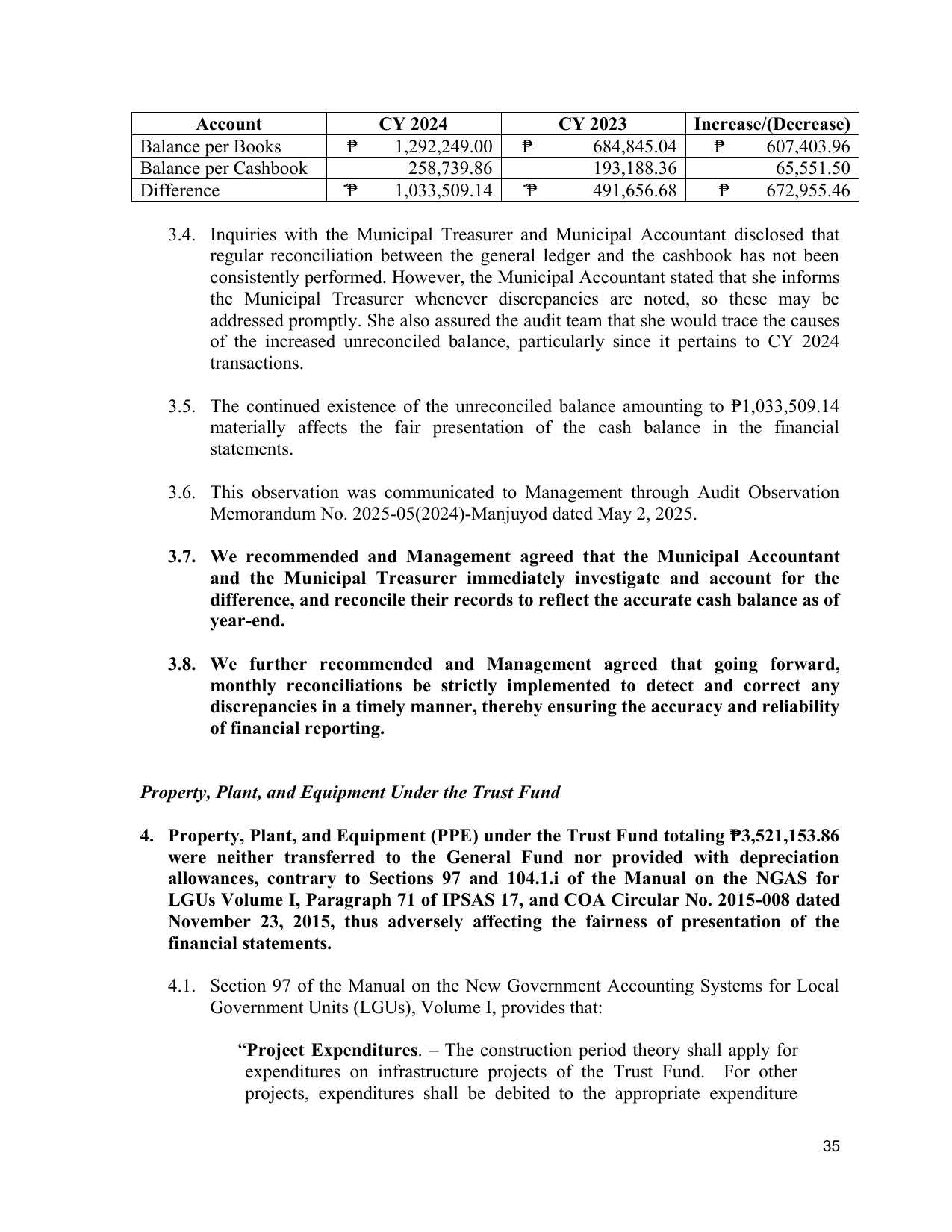

Account CY 2024 CY 2023 Increase/(Decrease)

Balance per Books ₱ 1,292,249.00 ₱ 684,845.04 ₱ 607,403.96

Balance per Cashbook 258,739.86 193,188.36 65,551.50

Difference ̈́₱ 1,033,509.14 ̈́₱ 491,656.68 ₱ 672,955.46

3.4. Inquiries with the Municipal Treasurer and Municipal Accountant disclosed that

regular reconciliation between the general ledger and the cashbook has not been

consistently performed. However, the Municipal Accountant stated that she informs

the Municipal Treasurer whenever discrepancies are noted, so these may be

addressed promptly. She also assured the audit team that she would trace the causes

of the increased unreconciled balance, particularly since it pertains to CY 2024

transactions.

3.5. The continued existence of the unreconciled balance amounting to ₱1,033,509.14

materially affects the fair presentation of the cash balance in the financial

statements.

3.6. This observation was communicated to Management through Audit Observation

Memorandum No. 2025-05(2024)-Manjuyod dated May 2, 2025.

3.7. We recommended and Management agreed that the Municipal Accountant

and the Municipal Treasurer immediately investigate and account for the

difference, and reconcile their records to reflect the accurate cash balance as of

year-end.

3.8. We further recommended and Management agreed that going forward,

monthly reconciliations be strictly implemented to detect and correct any

discrepancies in a timely manner, thereby ensuring the accuracy and reliability

of financial reporting.

Property, Plant, and Equipment Under the Trust Fund

4. Property, Plant, and Equipment (PPE) under the Trust Fund totaling ₱3,521,153.86

were neither transferred to the General Fund nor provided with depreciation

allowances, contrary to Sections 97 and 104.1.i of the Manual on the NGAS for

LGUs Volume I, Paragraph 71 of IPSAS 17, and COA Circular No. 2015-008 dated

November 23, 2015, thus adversely affecting the fairness of presentation of the

financial statements.

4.1. Section 97 of the Manual on the New Government Accounting Systems for Local

Government Units (LGUs), Volume I, provides that:

“Project Expenditures. – The construction period theory shall apply for

expenditures on infrastructure projects of the Trust Fund. For other

projects, expenditures shall be debited to the appropriate expenditure

35