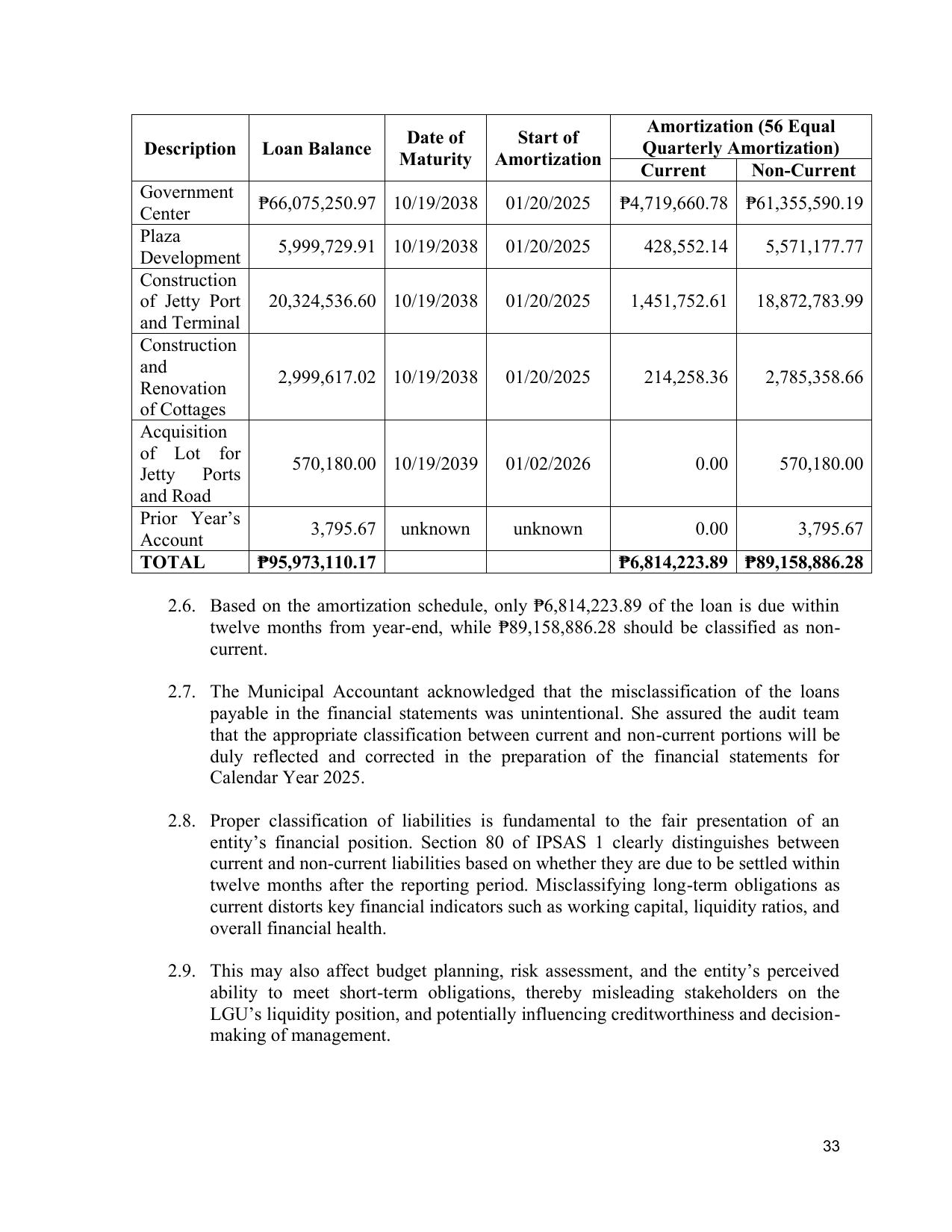

Amortization (56 Equal

Date of Start of

Description Loan Balance Quarterly Amortization)

Maturity Amortization

Current Non-Current

Government

₱66,075,250.97 10/19/2038 01/20/2025 ₱4,719,660.78 ₱61,355,590.19

Center

Plaza

5,999,729.91 10/19/2038 01/20/2025 428,552.14 5,571,177.77

Development

Construction

of Jetty Port 20,324,536.60 10/19/2038 01/20/2025 1,451,752.61 18,872,783.99

and Terminal

Construction

and

2,999,617.02 10/19/2038 01/20/2025 214,258.36 2,785,358.66

Renovation

of Cottages

Acquisition

of Lot for

570,180.00 10/19/2039 01/02/2026 0.00 570,180.00

Jetty Ports

and Road

Prior Year’s

3,795.67 unknown unknown 0.00 3,795.67

Account

TOTAL ₱95,973,110.17 ₱6,814,223.89 ₱89,158,886.28

2.6. Based on the amortization schedule, only ₱6,814,223.89 of the loan is due within

twelve months from year-end, while ₱89,158,886.28 should be classified as non-

current.

2.7. The Municipal Accountant acknowledged that the misclassification of the loans

payable in the financial statements was unintentional. She assured the audit team

that the appropriate classification between current and non-current portions will be

duly reflected and corrected in the preparation of the financial statements for

Calendar Year 2025.

2.8. Proper classification of liabilities is fundamental to the fair presentation of an

entity’s financial position. Section 80 of IPSAS 1 clearly distinguishes between

current and non-current liabilities based on whether they are due to be settled within

twelve months after the reporting period. Misclassifying long-term obligations as

current distorts key financial indicators such as working capital, liquidity ratios, and

overall financial health.

2.9. This may also affect budget planning, risk assessment, and the entity’s perceived

ability to meet short-term obligations, thereby misleading stakeholders on the

LGU’s liquidity position, and potentially influencing creditworthiness and decision-

making of management.

33