4.11. Furthermore, we recommended and Management agreed that the Municipal

Accountant conduct regular monitoring and timely reporting of unliquidated

cash advances to the Local Chief Executive, to ensure proper oversight and to

facilitate appropriate administrative actions as necessary.

Real Property Tax/Special Education Tax Receivables

5. The balances of the Real Property Tax (RPT) Receivable and Special Education Tax

(SET) Receivable accounts as of December 31, 2024, between the records of the

Municipal Accounting Office (MAO) and the Municipal Treasurer’s Office (MTO)

showed a difference of ₱90,418,239.18 due to the non-reconciliation of their records

thus, the RPT/SET Receivable and Deferred Income accounts, as presented in the

financial statements, are deemed unreliable.

5.1. Basic accounting principles dictate the reconciliation of records to ensure that

financial data is accurate, complete, and consistent. Reconciliation is the process of

comparing two sets of records to verify that the figures match and to identify any

discrepancies. In practice, regular reconciliation (monthly, quarterly, or annually)

promotes sound financial management, supports decision-making, and ensures

compliance with standards and policies.

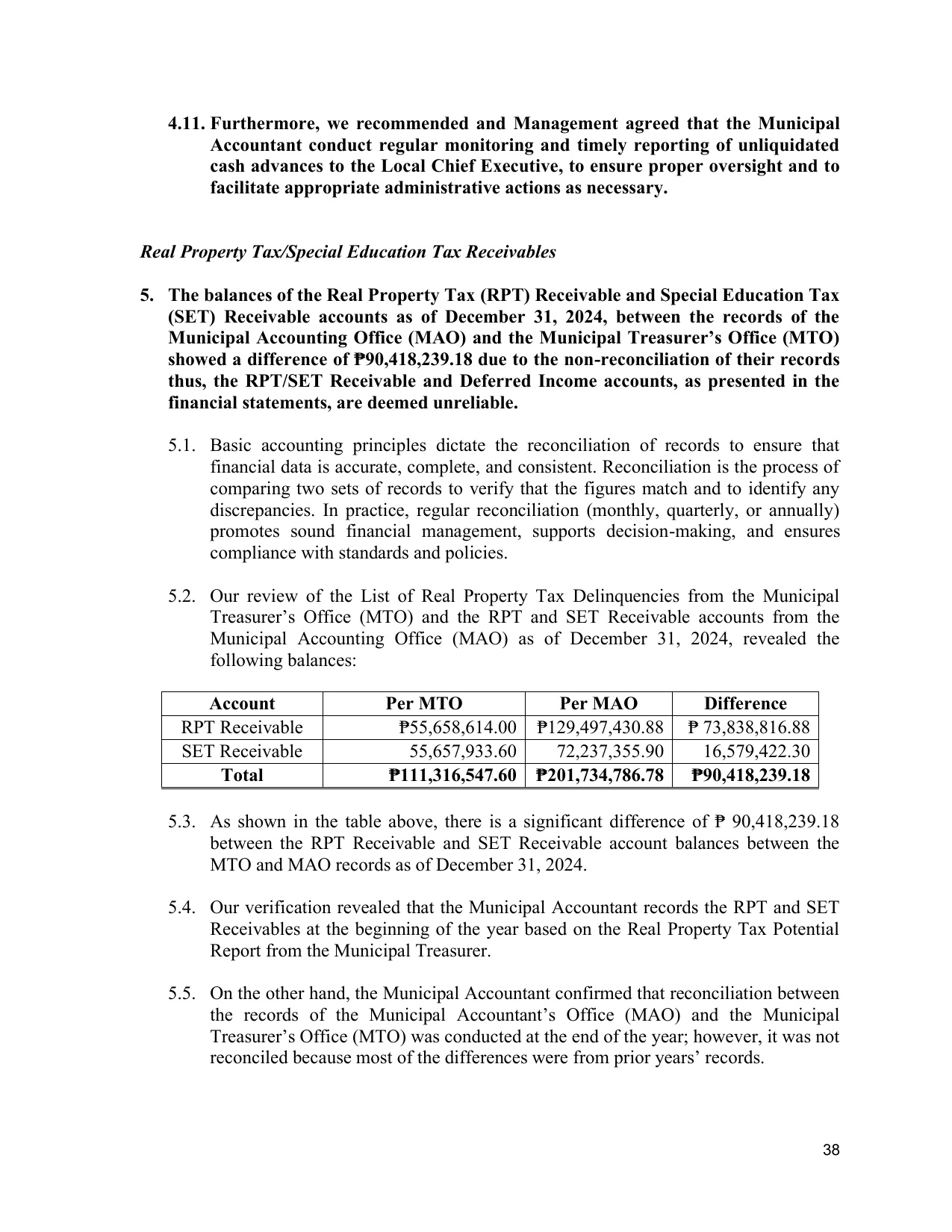

5.2. Our review of the List of Real Property Tax Delinquencies from the Municipal

Treasurer’s Office (MTO) and the RPT and SET Receivable accounts from the

Municipal Accounting Office (MAO) as of December 31, 2024, revealed the

following balances:

Account Per MTO Per MAO Difference

RPT Receivable ₱55,658,614.00 ₱129,497,430.88 ₱ 73,838,816.88

SET Receivable 55,657,933.60 72,237,355.90 16,579,422.30

Total ₱111,316,547.60 ₱201,734,786.78 ₱90,418,239.18

5.3. As shown in the table above, there is a significant difference of ₱ 90,418,239.18

between the RPT Receivable and SET Receivable account balances between the

MTO and MAO records as of December 31, 2024.

5.4. Our verification revealed that the Municipal Accountant records the RPT and SET

Receivables at the beginning of the year based on the Real Property Tax Potential

Report from the Municipal Treasurer.

5.5. On the other hand, the Municipal Accountant confirmed that reconciliation between

the records of the Municipal Accountant’s Office (MAO) and the Municipal

Treasurer’s Office (MTO) was conducted at the end of the year; however, it was not

reconciled because most of the differences were from prior years’ records.

38