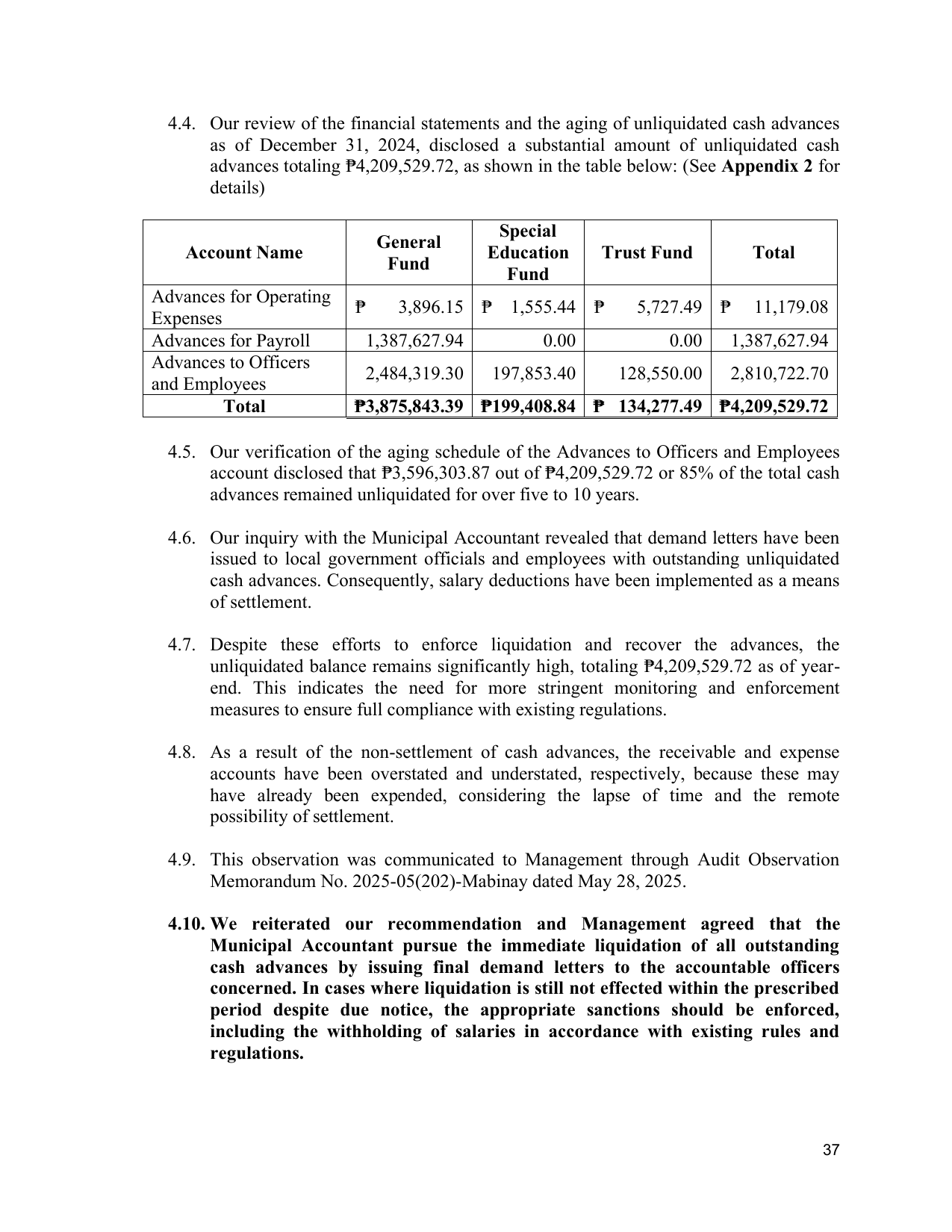

4.4. Our review of the financial statements and the aging of unliquidated cash advances

as of December 31, 2024, disclosed a substantial amount of unliquidated cash

advances totaling ₱4,209,529.72, as shown in the table below: (See Appendix 2 for

details)

Special

General

Account Name Education Trust Fund Total

Fund

Fund

Advances for Operating

₱ 3,896.15 ₱ 1,555.44 ₱ 5,727.49 ₱ 11,179.08

Expenses

Advances for Payroll 1,387,627.94 0.00 0.00 1,387,627.94

Advances to Officers

2,484,319.30 197,853.40 128,550.00 2,810,722.70

and Employees

Total ₱3,875,843.39 ₱199,408.84 ₱ 134,277.49 ₱4,209,529.72

4.5. Our verification of the aging schedule of the Advances to Officers and Employees

account disclosed that ₱3,596,303.87 out of ₱4,209,529.72 or 85% of the total cash

advances remained unliquidated for over five to 10 years.

4.6. Our inquiry with the Municipal Accountant revealed that demand letters have been

issued to local government officials and employees with outstanding unliquidated

cash advances. Consequently, salary deductions have been implemented as a means

of settlement.

4.7. Despite these efforts to enforce liquidation and recover the advances, the

unliquidated balance remains significantly high, totaling ₱4,209,529.72 as of year-

end. This indicates the need for more stringent monitoring and enforcement

measures to ensure full compliance with existing regulations.

4.8. As a result of the non-settlement of cash advances, the receivable and expense

accounts have been overstated and understated, respectively, because these may

have already been expended, considering the lapse of time and the remote

possibility of settlement.

4.9. This observation was communicated to Management through Audit Observation

Memorandum No. 2025-05(202)-Mabinay dated May 28, 2025.

4.10. We reiterated our recommendation and Management agreed that the

Municipal Accountant pursue the immediate liquidation of all outstanding

cash advances by issuing final demand letters to the accountable officers

concerned. In cases where liquidation is still not effected within the prescribed

period despite due notice, the appropriate sanctions should be enforced,

including the withholding of salaries in accordance with existing rules and

regulations.

37