accordance with the definitions and recognition criteria for assets, liabilities,

revenue, and expenses set out in IPSASs.

3.2. Further, Section 7, Chapter II of the Revised Cash Exam Manual, emphasizes that

an accountable officer shall reconcile her cashbook with the accounting records at

least quarterly, unless the agency requires a more frequent reconciliation.

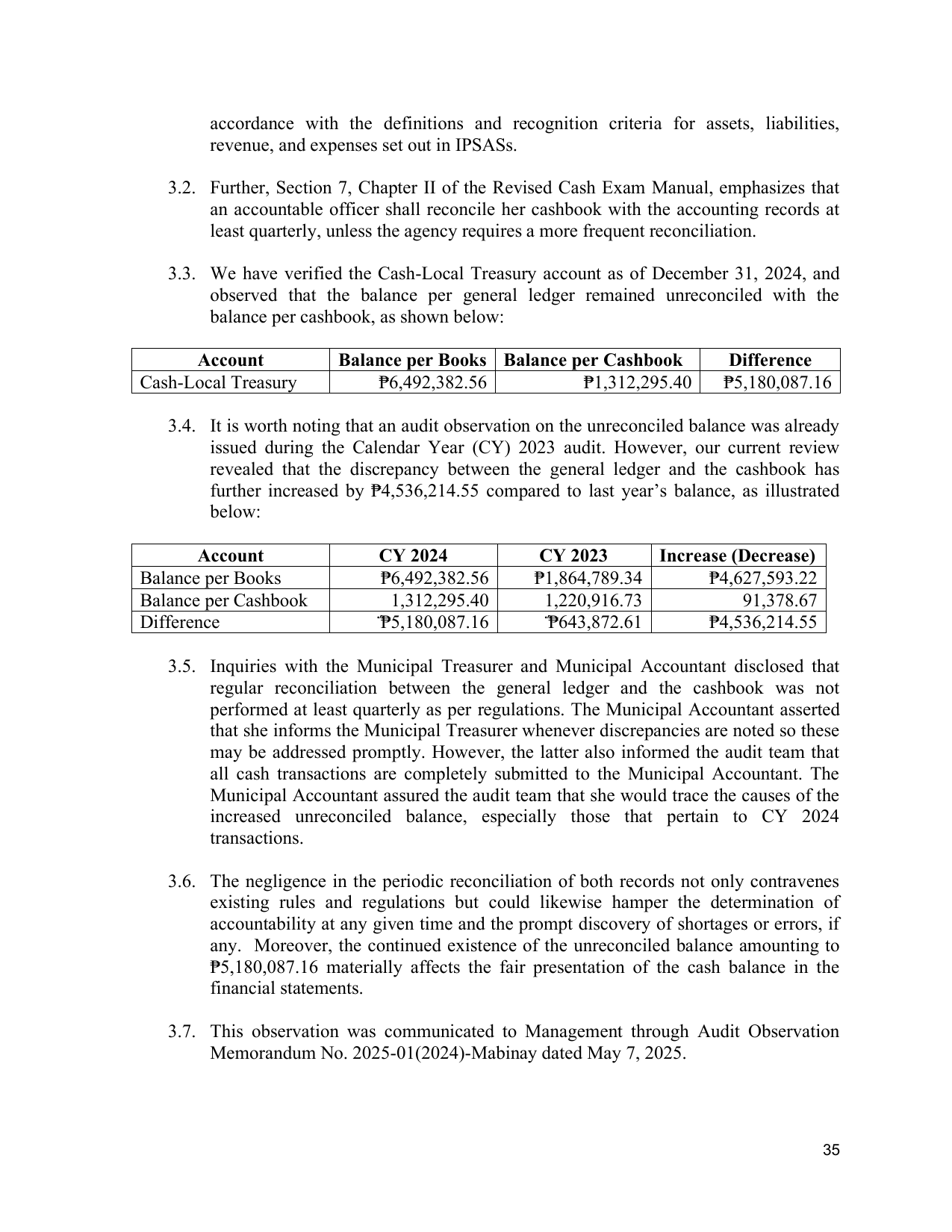

3.3. We have verified the Cash-Local Treasury account as of December 31, 2024, and

observed that the balance per general ledger remained unreconciled with the

balance per cashbook, as shown below:

Account Balance per Books Balance per Cashbook Difference

Cash-Local Treasury ₱6,492,382.56 ₱1,312,295.40 ₱5,180,087.16

3.4. It is worth noting that an audit observation on the unreconciled balance was already

issued during the Calendar Year (CY) 2023 audit. However, our current review

revealed that the discrepancy between the general ledger and the cashbook has

further increased by ₱4,536,214.55 compared to last year’s balance, as illustrated

below:

Account CY 2024 CY 2023 Increase (Decrease)

Balance per Books ₱6,492,382.56 ₱1,864,789.34 ₱4,627,593.22

Balance per Cashbook 1,312,295.40 1,220,916.73 91,378.67

Difference ̈́₱5,180,087.16 ̈́₱643,872.61 ₱4,536,214.55

3.5. Inquiries with the Municipal Treasurer and Municipal Accountant disclosed that

regular reconciliation between the general ledger and the cashbook was not

performed at least quarterly as per regulations. The Municipal Accountant asserted

that she informs the Municipal Treasurer whenever discrepancies are noted so these

may be addressed promptly. However, the latter also informed the audit team that

all cash transactions are completely submitted to the Municipal Accountant. The

Municipal Accountant assured the audit team that she would trace the causes of the

increased unreconciled balance, especially those that pertain to CY 2024

transactions.

3.6. The negligence in the periodic reconciliation of both records not only contravenes

existing rules and regulations but could likewise hamper the determination of

accountability at any given time and the prompt discovery of shortages or errors, if

any. Moreover, the continued existence of the unreconciled balance amounting to

₱5,180,087.16 materially affects the fair presentation of the cash balance in the

financial statements.

3.7. This observation was communicated to Management through Audit Observation

Memorandum No. 2025-01(2024)-Mabinay dated May 7, 2025.

35