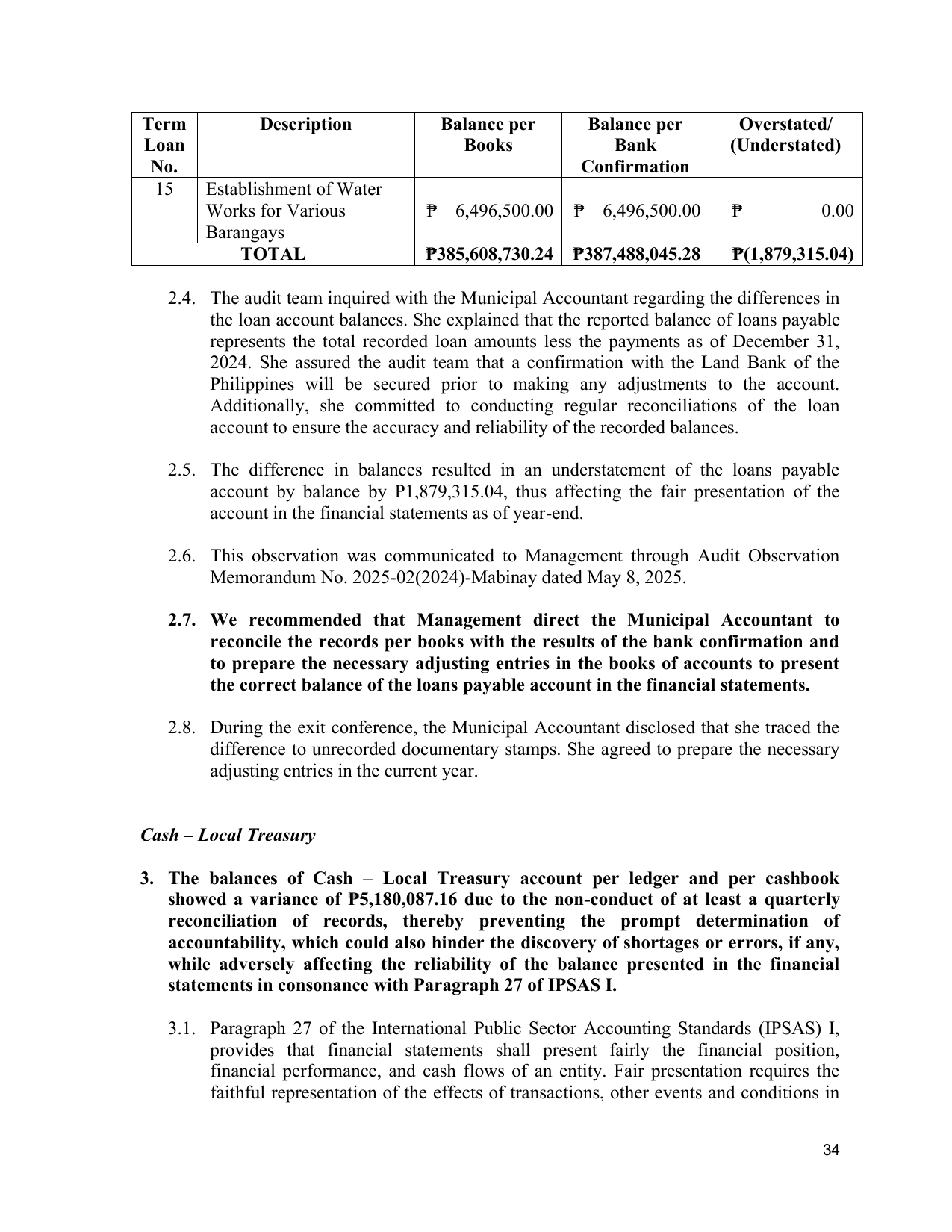

Term Description Balance per Balance per Overstated/

Loan Books Bank (Understated)

No. Confirmation

15 Establishment of Water

Works for Various ₱ 6,496,500.00 ₱ 6,496,500.00 ₱ 0.00

Barangays

TOTAL ₱385,608,730.24 ₱387,488,045.28 ₱(1,879,315.04)

2.4. The audit team inquired with the Municipal Accountant regarding the differences in

the loan account balances. She explained that the reported balance of loans payable

represents the total recorded loan amounts less the payments as of December 31,

2024. She assured the audit team that a confirmation with the Land Bank of the

Philippines will be secured prior to making any adjustments to the account.

Additionally, she committed to conducting regular reconciliations of the loan

account to ensure the accuracy and reliability of the recorded balances.

2.5. The difference in balances resulted in an understatement of the loans payable

account by balance by P1,879,315.04, thus affecting the fair presentation of the

account in the financial statements as of year-end.

2.6. This observation was communicated to Management through Audit Observation

Memorandum No. 2025-02(2024)-Mabinay dated May 8, 2025.

2.7. We recommended that Management direct the Municipal Accountant to

reconcile the records per books with the results of the bank confirmation and

to prepare the necessary adjusting entries in the books of accounts to present

the correct balance of the loans payable account in the financial statements.

2.8. During the exit conference, the Municipal Accountant disclosed that she traced the

difference to unrecorded documentary stamps. She agreed to prepare the necessary

adjusting entries in the current year.

Cash – Local Treasury

3. The balances of Cash – Local Treasury account per ledger and per cashbook

showed a variance of ₱5,180,087.16 due to the non-conduct of at least a quarterly

reconciliation of records, thereby preventing the prompt determination of

accountability, which could also hinder the discovery of shortages or errors, if any,

while adversely affecting the reliability of the balance presented in the financial

statements in consonance with Paragraph 27 of IPSAS I.

3.1. Paragraph 27 of the International Public Sector Accounting Standards (IPSAS) I,

provides that financial statements shall present fairly the financial position,

financial performance, and cash flows of an entity. Fair presentation requires the

faithful representation of the effects of transactions, other events and conditions in

34