appropriations. The use of said funds withheld by the government

agencies other than for the purpose of remitting Program contributions

will hold the erring government employers liable under the pertinent

provisions of the Revised Penal Code.”

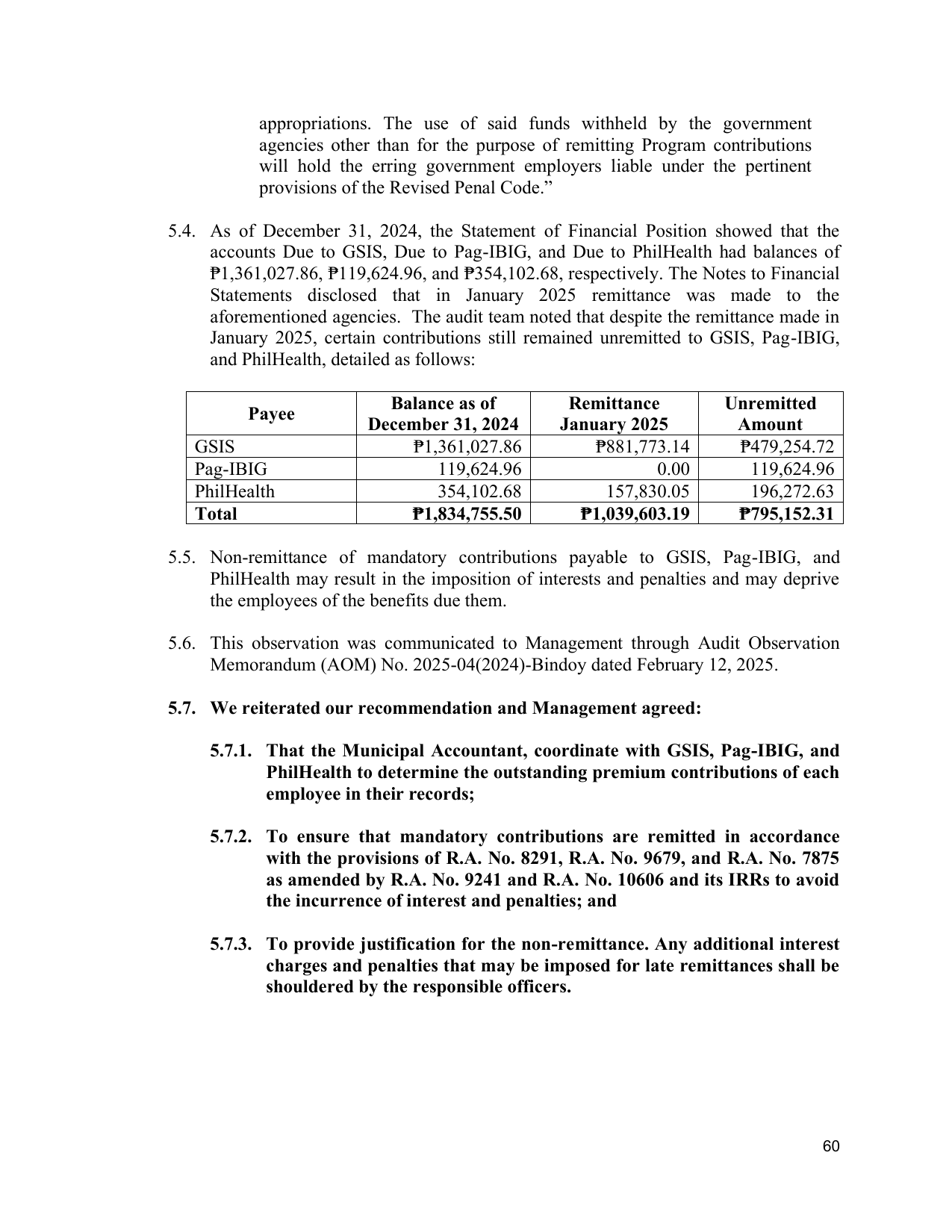

5.4. As of December 31, 2024, the Statement of Financial Position showed that the

accounts Due to GSIS, Due to Pag-IBIG, and Due to PhilHealth had balances of

₱1,361,027.86, ₱119,624.96, and ₱354,102.68, respectively. The Notes to Financial

Statements disclosed that in January 2025 remittance was made to the

aforementioned agencies. The audit team noted that despite the remittance made in

January 2025, certain contributions still remained unremitted to GSIS, Pag-IBIG,

and PhilHealth, detailed as follows:

Balance as of Remittance Unremitted

Payee

December 31, 2024 January 2025 Amount

GSIS ₱1,361,027.86 ₱881,773.14 ₱479,254.72

Pag-IBIG 119,624.96 0.00 119,624.96

PhilHealth 354,102.68 157,830.05 196,272.63

Total ₱1,834,755.50 ₱1,039,603.19 ₱795,152.31

5.5. Non-remittance of mandatory contributions payable to GSIS, Pag-IBIG, and

PhilHealth may result in the imposition of interests and penalties and may deprive

the employees of the benefits due them.

5.6. This observation was communicated to Management through Audit Observation

Memorandum (AOM) No. 2025-04(2024)-Bindoy dated February 12, 2025.

5.7. We reiterated our recommendation and Management agreed:

5.7.1. That the Municipal Accountant, coordinate with GSIS, Pag-IBIG, and

PhilHealth to determine the outstanding premium contributions of each

employee in their records;

5.7.2. To ensure that mandatory contributions are remitted in accordance

with the provisions of R.A. No. 8291, R.A. No. 9679, and R.A. No. 7875

as amended by R.A. No. 9241 and R.A. No. 10606 and its IRRs to avoid

the incurrence of interest and penalties; and

5.7.3. To provide justification for the non-remittance. Any additional interest

charges and penalties that may be imposed for late remittances shall be

shouldered by the responsible officers.

60