Real Property Tax and Special Education Tax Receivables

6. The balances of the Real Property Tax (RPT) Receivable and Special Education Tax

(SET) Receivable accounts as of December 31, 2024, between the records of the

Municipal Accounting Office (MAO) and the Municipal Treasurer’s Office (MTO)

showed a difference of ₱40,038,710.14 because the Municipal Accountant and

Municipal Treasurer did not periodically reconcile their records while the RPT and

SET receivables were not recorded in accordance with Section 20, Volume I, and

Section 10, Volume II of the Manual on the New Government Accounting System

(NGAS) thus, RPT/SET Receivable and Deferred RPT/SET Income accounts as

presented in the financial statements are deemed unreliable.

6.1. Section 20, Volume I of the Manual on the New Government Accounting System

(NGAS) provides that:

“Real Property Tax Receivables/Special Education Tax Receivables shall

be established at the beginning of the year based on Real Property Tax

Account Register/Taxpayer’s index card. At the beginning of the year,

the Treasurer shall furnish the Chief Accountant of a duly certified list

showing the name of taxpayers and the amount due and collectible for the

year. Based on the list, the Chief Accountant shall draw a Journal Entry

Voucher (JEV) to record the debit to Real Property Tax Receivable/Special

Education Tax Receivable and crediting to Deferred Real Property Tax

Income/Deferred Special Education Tax Income.” (Emphasis ours)

6.2. On the other hand, Section 10, Volume II of the same Manual for LGUs provides

that:

“The Subsidiary Ledger is a book of final entry containing the details or

breakdown of the balances of the controlling account appearing in the

General ledger. Postings to the subsidiary ledgers generally come from the

source documents. xxx. The totals of the subsidiary ledger balances shall be

reconciled to their respective control account at the end of every month.”

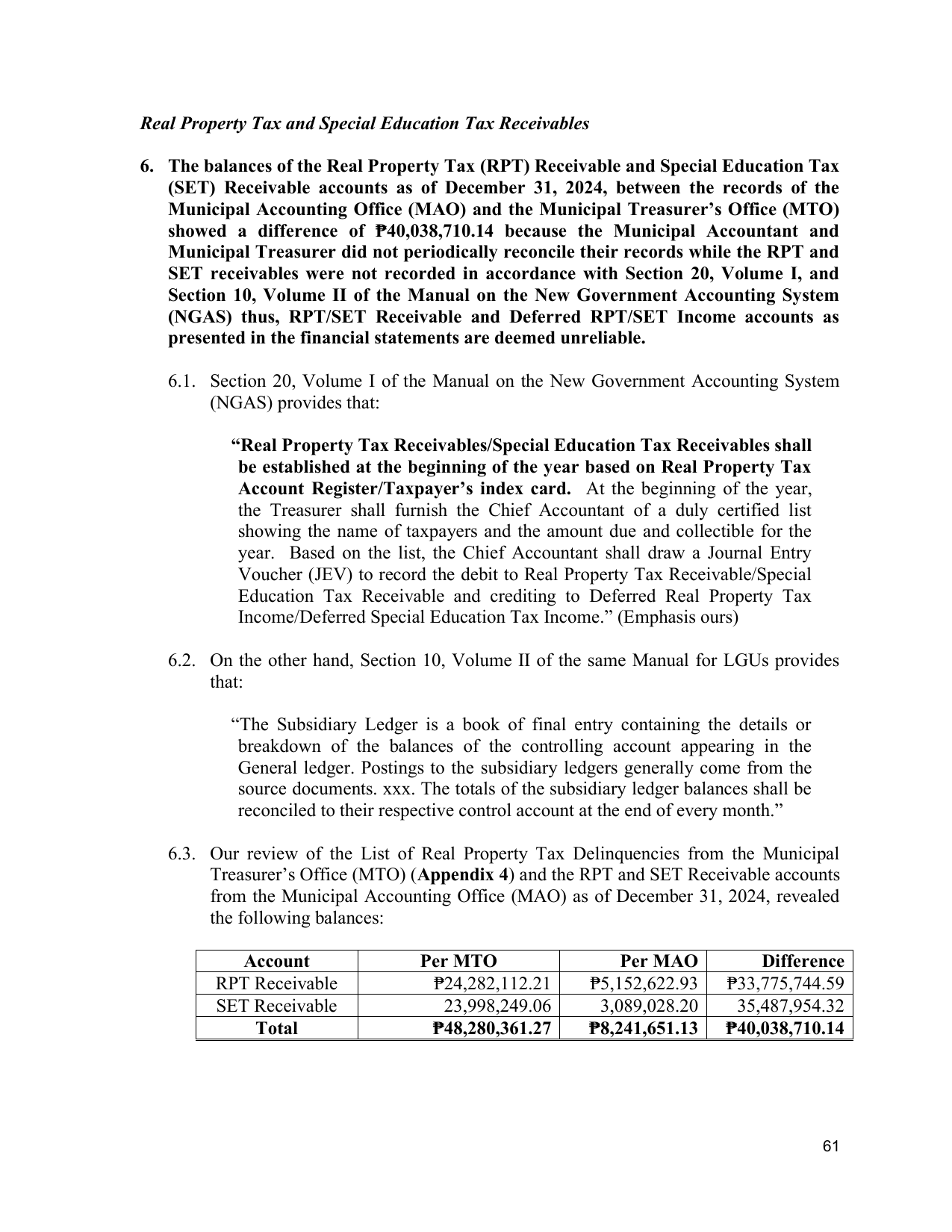

6.3. Our review of the List of Real Property Tax Delinquencies from the Municipal

Treasurer’s Office (MTO) (Appendix 4) and the RPT and SET Receivable accounts

from the Municipal Accounting Office (MAO) as of December 31, 2024, revealed

the following balances:

Account Per MTO Per MAO Difference

RPT Receivable ₱24,282,112.21 ₱5,152,622.93 ₱33,775,744.59

SET Receivable 23,998,249.06 3,089,028.20 35,487,954.32

Total ₱48,280,361.27 ₱8,241,651.13 ₱40,038,710.14

61