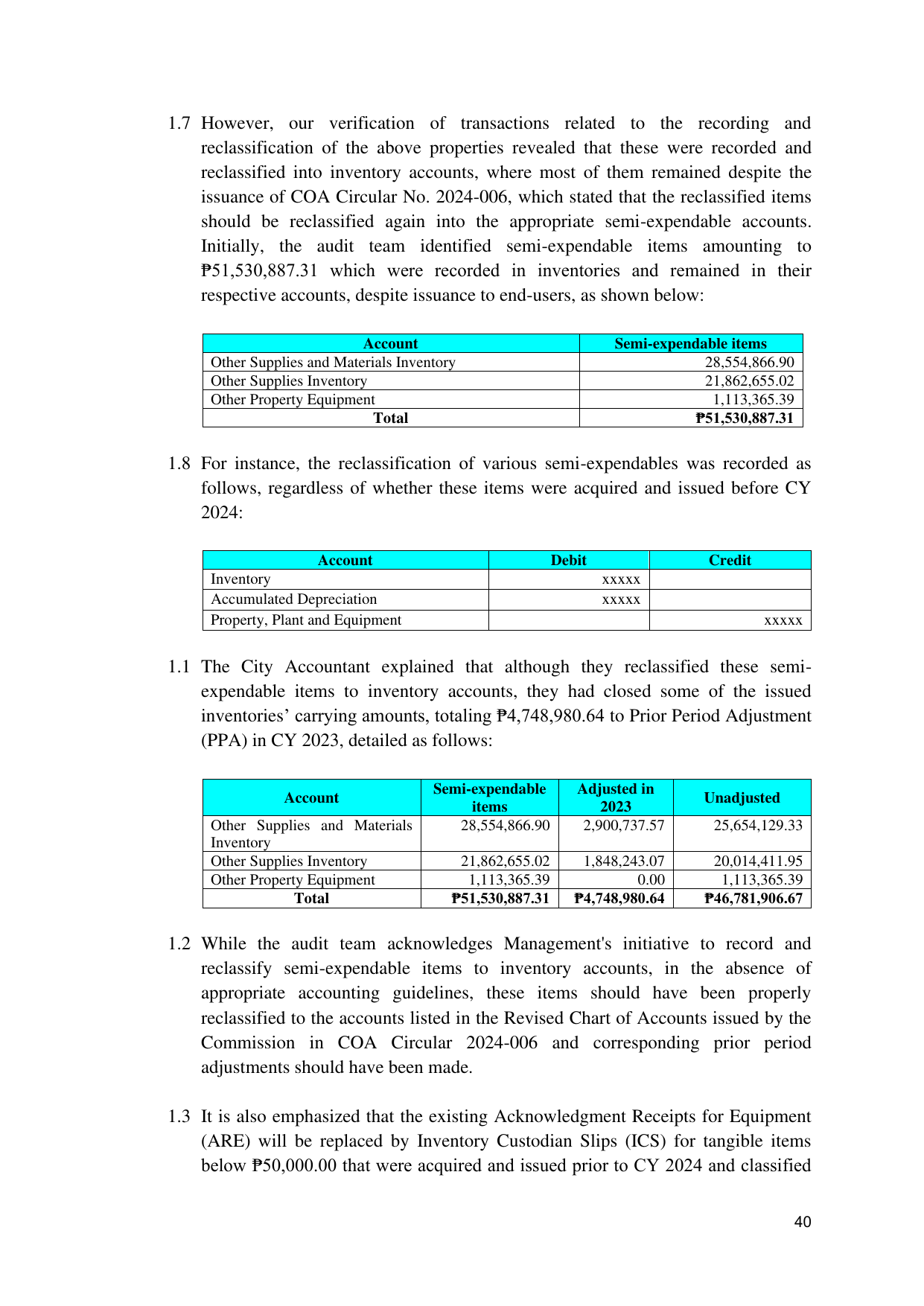

1.7 However, our verification of transactions related to the recording and

reclassification of the above properties revealed that these were recorded and

reclassified into inventory accounts, where most of them remained despite the

issuance of COA Circular No. 2024-006, which stated that the reclassified items

should be reclassified again into the appropriate semi-expendable accounts.

Initially, the audit team identified semi-expendable items amounting to

₱51,530,887.31 which were recorded in inventories and remained in their

respective accounts, despite issuance to end-users, as shown below:

Account Semi-expendable items

Other Supplies and Materials Inventory 28,554,866.90

Other Supplies Inventory 21,862,655.02

Other Property Equipment 1,113,365.39

Total ₱51,530,887.31

1.8 For instance, the reclassification of various semi-expendables was recorded as

follows, regardless of whether these items were acquired and issued before CY

2024:

Account Debit Credit

Inventory xxxxx

Accumulated Depreciation xxxxx

Property, Plant and Equipment xxxxx

1.1 The City Accountant explained that although they reclassified these semi-

expendable items to inventory accounts, they had closed some of the issued

inventories’ carrying amounts, totaling ₱4,748,980.64 to Prior Period Adjustment

(PPA) in CY 2023, detailed as follows:

Semi-expendable Adjusted in

Account Unadjusted

items 2023

Other Supplies and Materials 28,554,866.90 2,900,737.57 25,654,129.33

Inventory

Other Supplies Inventory 21,862,655.02 1,848,243.07 20,014,411.95

Other Property Equipment 1,113,365.39 0.00 1,113,365.39

Total ₱51,530,887.31 ₱4,748,980.64 ₱46,781,906.67

1.2 While the audit team acknowledges Management's initiative to record and

reclassify semi-expendable items to inventory accounts, in the absence of

appropriate accounting guidelines, these items should have been properly

reclassified to the accounts listed in the Revised Chart of Accounts issued by the

Commission in COA Circular 2024-006 and corresponding prior period

adjustments should have been made.

1.3 It is also emphasized that the existing Acknowledgment Receipts for Equipment

(ARE) will be replaced by Inventory Custodian Slips (ICS) for tangible items

below ₱50,000.00 that were acquired and issued prior to CY 2024 and classified

40