1.4.1 Tangible items below ₱50,000.00 acquired prior to CY 2024 and previously

classified as PPE, which are still in custody of the Supply and/or Property

Division/Unit, the cost shall be reclassified to the appropriate semi-expendable

property account under the major account group Inventories and the

corresponding accumulated depreciation and accumulated impairment losses

shall be closed in the books of accounts; and

1.4.2 Tangible items below ₱50,000.00 acquired and issued prior to CY 2024 and

have been classified as PPE, the carrying amount shall be expensed/charged

to Prior Period Adjustment and the corresponding accumulated depreciation

and accumulated impairment losses shall be closed in the books of accounts.

1.5 We directed Management’s attention to Annex B of the Circular, which delineates

the new accounts that are to be utilized. Additionally, Annex C provides illustrative

accounting entries for various cases.

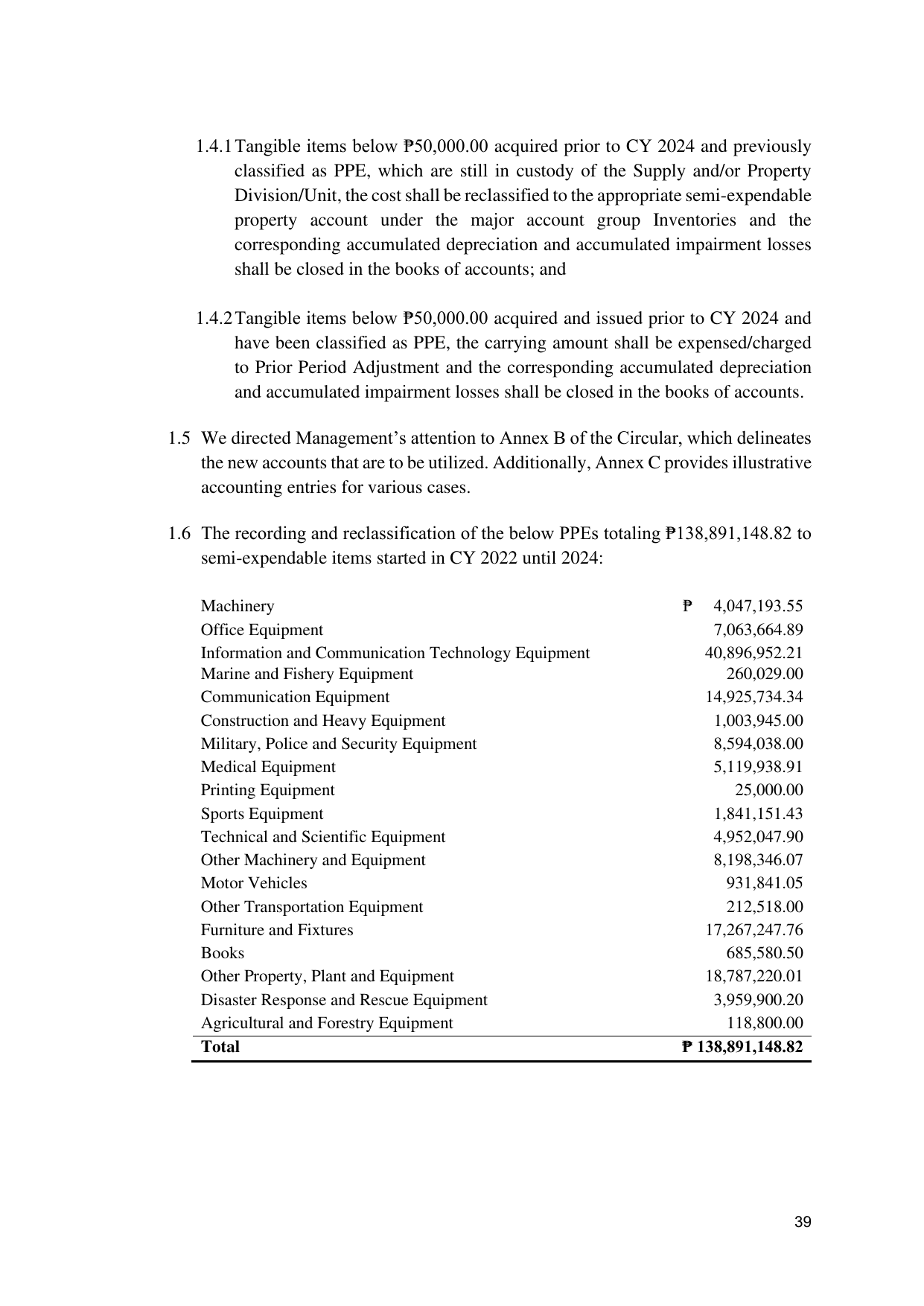

1.6 The recording and reclassification of the below PPEs totaling ₱138,891,148.82 to

semi-expendable items started in CY 2022 until 2024:

Machinery ₱ 4,047,193.55

Office Equipment 7,063,664.89

Information and Communication Technology Equipment 40,896,952.21

Marine and Fishery Equipment 260,029.00

Communication Equipment 14,925,734.34

Construction and Heavy Equipment 1,003,945.00

Military, Police and Security Equipment 8,594,038.00

Medical Equipment 5,119,938.91

Printing Equipment 25,000.00

Sports Equipment 1,841,151.43

Technical and Scientific Equipment 4,952,047.90

Other Machinery and Equipment 8,198,346.07

Motor Vehicles 931,841.05

Other Transportation Equipment 212,518.00

Furniture and Fixtures 17,267,247.76

Books 685,580.50

Other Property, Plant and Equipment 18,787,220.01

Disaster Response and Rescue Equipment 3,959,900.20

Agricultural and Forestry Equipment 118,800.00

Total ₱ 138,891,148.82

39