as PPE (Sec. 3.7, COA Circular No. 2024-006). However, an interview with the

Accounting Staff revealed that because these items had already been issued with

AREs, they were not subsequently replaced with ICS upon their reclassification.

As a result, the carrying amounts of these semi-expendable properties were not

charged to the Prior Period Adjustment.

1.4 The incorrect treatment in the reclassification of semi-expendable properties led to

an overstatement of the Other Supplies and Materials Inventory, Other Supplies

Inventory, and Other Property Equipment amounting to ₱25,654,129.33,

20,014,411.95, and ₱1,113,365.39, respectively, and an understatement of the PPA

totaling ₱46,781,906.67. The PPA will be closed to Equity at the end of the year,

hence, due to the understatement of the PPA, Equity is overstated by the same

amount. These discrepancies affect the fairness and reliability of the financial

statements, potentially influencing stakeholder decision-making and resulting in a

misrepresentation of financial information presented to users.

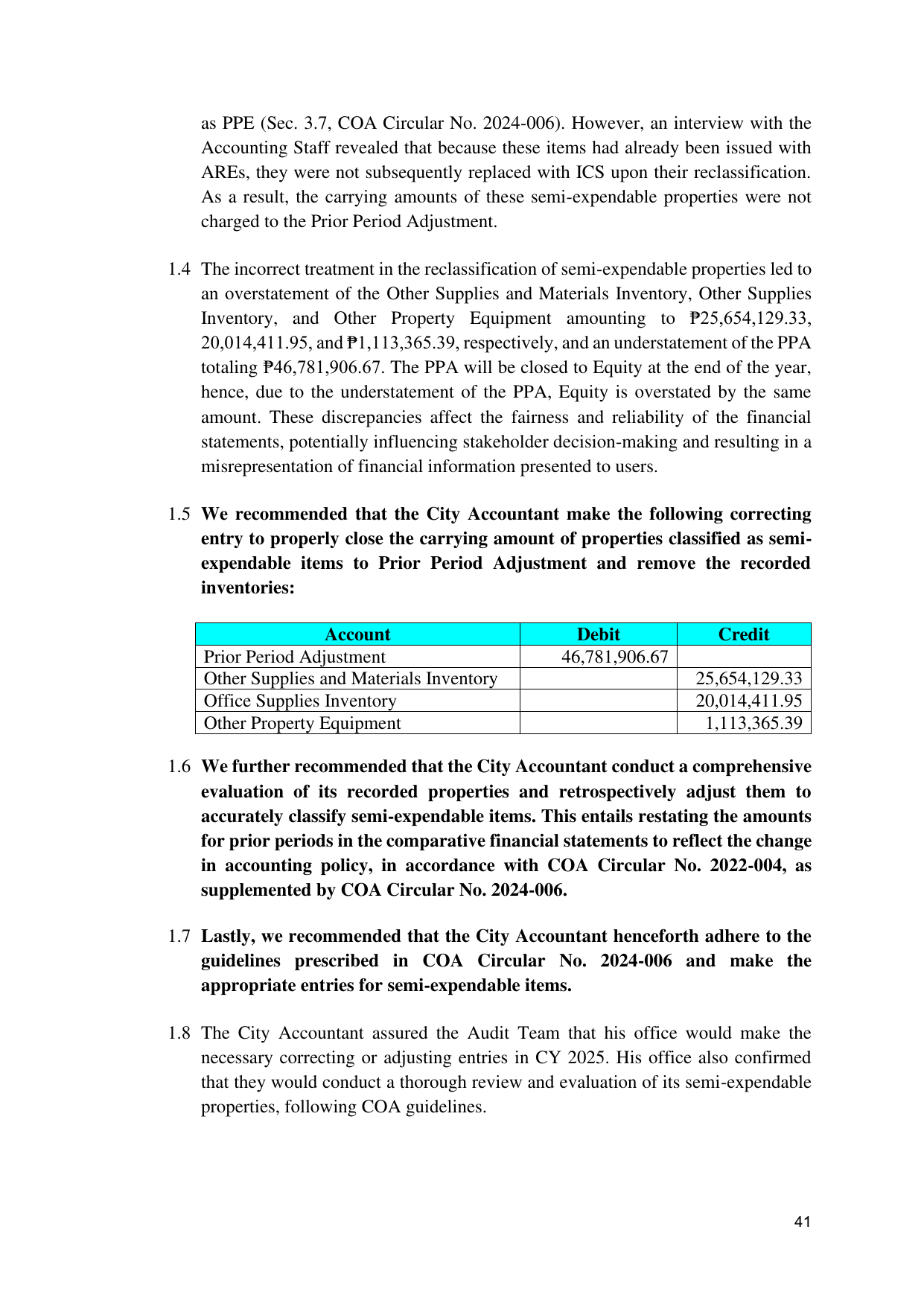

1.5 We recommended that the City Accountant make the following correcting

entry to properly close the carrying amount of properties classified as semi-

expendable items to Prior Period Adjustment and remove the recorded

inventories:

Account Debit Credit

Prior Period Adjustment 46,781,906.67

Other Supplies and Materials Inventory 25,654,129.33

Office Supplies Inventory 20,014,411.95

Other Property Equipment 1,113,365.39

1.6 We further recommended that the City Accountant conduct a comprehensive

evaluation of its recorded properties and retrospectively adjust them to

accurately classify semi-expendable items. This entails restating the amounts

for prior periods in the comparative financial statements to reflect the change

in accounting policy, in accordance with COA Circular No. 2022-004, as

supplemented by COA Circular No. 2024-006.

1.7 Lastly, we recommended that the City Accountant henceforth adhere to the

guidelines prescribed in COA Circular No. 2024-006 and make the

appropriate entries for semi-expendable items.

1.8 The City Accountant assured the Audit Team that his office would make the

necessary correcting or adjusting entries in CY 2025. His office also confirmed

that they would conduct a thorough review and evaluation of its semi-expendable

properties, following COA guidelines.

41