Page 69 of 88

STATUS OF IMPLEMENTATION OF PRIOR YEARS’ AUDIT

RECOMMENDATIONS

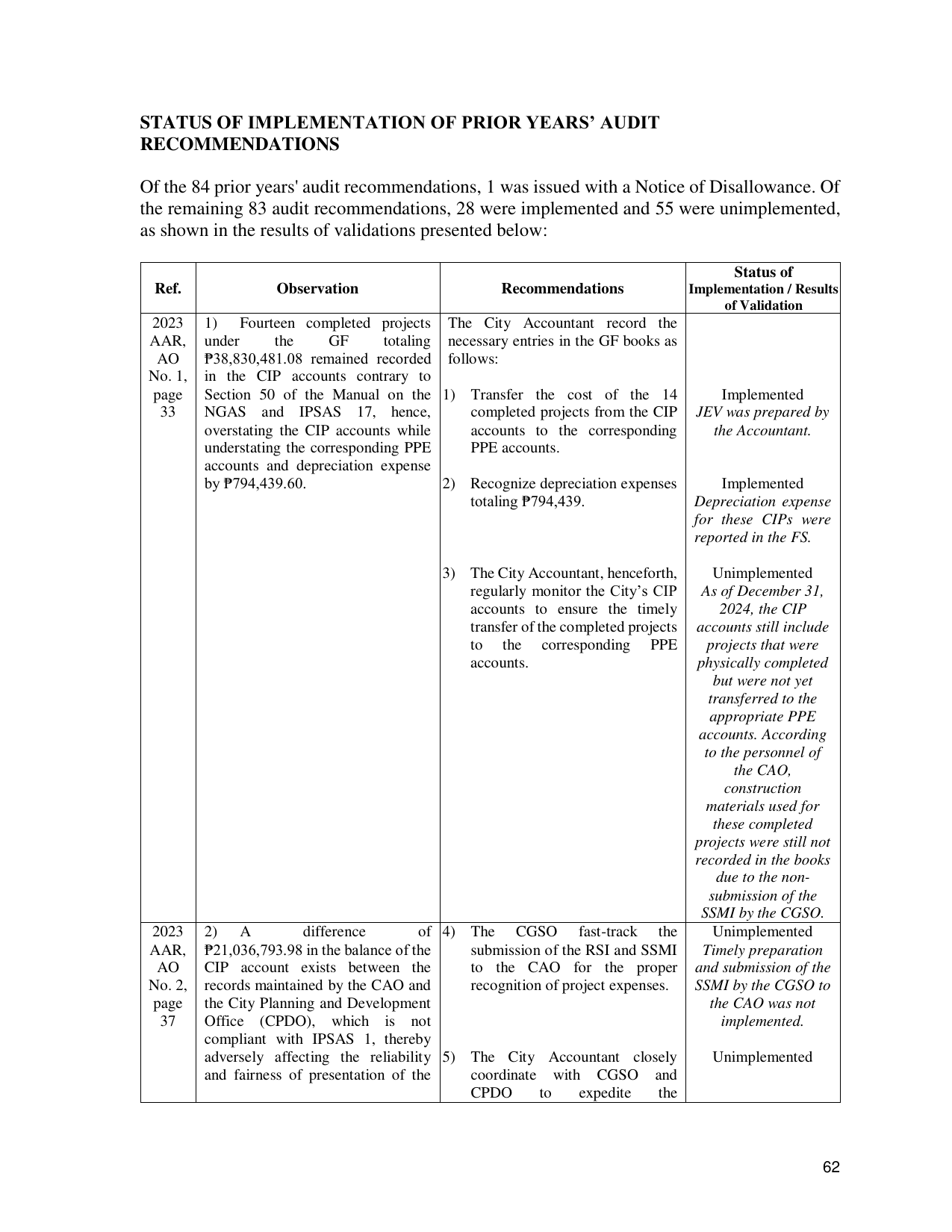

Of the 84 prior years' audit recommendations, 1 was issued with a Notice of Disallowance. Of

the remaining 83 audit recommendations, 28 were implemented and 55 were unimplemented,

as shown in the results of validations presented below:

Status of

Ref. Observation Recommendations Implementation / Results

of Validation

2023 1) Fourteen completed projects The City Accountant record the

AAR, under the GF totaling necessary entries in the GF books as

AO ₱38,830,481.08 remained recorded follows:

No. 1, in the CIP accounts contrary to

page Section 50 of the Manual on the 1) Transfer the cost of the 14 Implemented

33 NGAS and IPSAS 17, hence, completed projects from the CIP JEV was prepared by

overstating the CIP accounts while accounts to the corresponding the Accountant.

understating the corresponding PPE PPE accounts.

accounts and depreciation expense

by ₱794,439.60. 2) Recognize depreciation expenses Implemented

totaling ₱794,439. Depreciation expense

for these CIPs were

reported in the FS.

3) The City Accountant, henceforth, Unimplemented

regularly monitor the City’s CIP As of December 31,

accounts to ensure the timely 2024, the CIP

transfer of the completed projects accounts still include

to the corresponding PPE projects that were

accounts. physically completed

but were not yet

transferred to the

appropriate PPE

accounts. According

to the personnel of

the CAO,

construction

materials used for

these completed

projects were still not

recorded in the books

due to the non-

submission of the

SSMI by the CGSO.

2023 2) A difference of 4) The CGSO fast-track the Unimplemented

AAR, ₱21,036,793.98 in the balance of the submission of the RSI and SSMI Timely preparation

AO CIP account exists between the to the CAO for the proper and submission of the

No. 2, records maintained by the CAO and recognition of project expenses. SSMI by the CGSO to

page the City Planning and Development the CAO was not

37 Office (CPDO), which is not implemented.

compliant with IPSAS 1, thereby

adversely affecting the reliability 5) The City Accountant closely Unimplemented

and fairness of presentation of the coordinate with CGSO and

CPDO to expedite the

62