5.4.2.Despite the non-liquidation of their respective cash advances considering the

length of time that has elapsed, no sanctions had been imposed on these AOs.

5.4.2.1. The Quarterly Monitoring Report for Cash Advances is required to be

submitted by CAO five days after the end of each quarter. However, this

is often submitted late. Moreover, measures undertaken by agency

officials to monitor liquidation and to demand settlement of any

unliquidated cash advances were not indicated therein, among others.

Of the 18 AOs named in the Report, only 1 expired, leaving the 17 in

active service. Except for those granted for Confidential and

Intelligence Funds, the CAO should have facilitated the deletion of the

employees' names from the payroll until settlement of their cash

advances, as stipulated under Section 3.3 of COA Circular No. 96-004

dated April 19, 1996.

5.4.3.Cash advances for intelligence fund totaling ₱34,843,058.40 withdrawn by the

former LCEs were submitted to the COA Chairperson in the Central Office,

with a copy of the transmittal letter of the liquidation documents duly received

by the said office furnished to the City Accountant, in accordance with COA

Circular No. 2003-003 dated July 30, 2003, but no credit notice has yet been

received. Only the amount of ₱2,325,000.00 made by the incumbent LCE in the

last quarter of CY 2024 has yet to be liquidated.

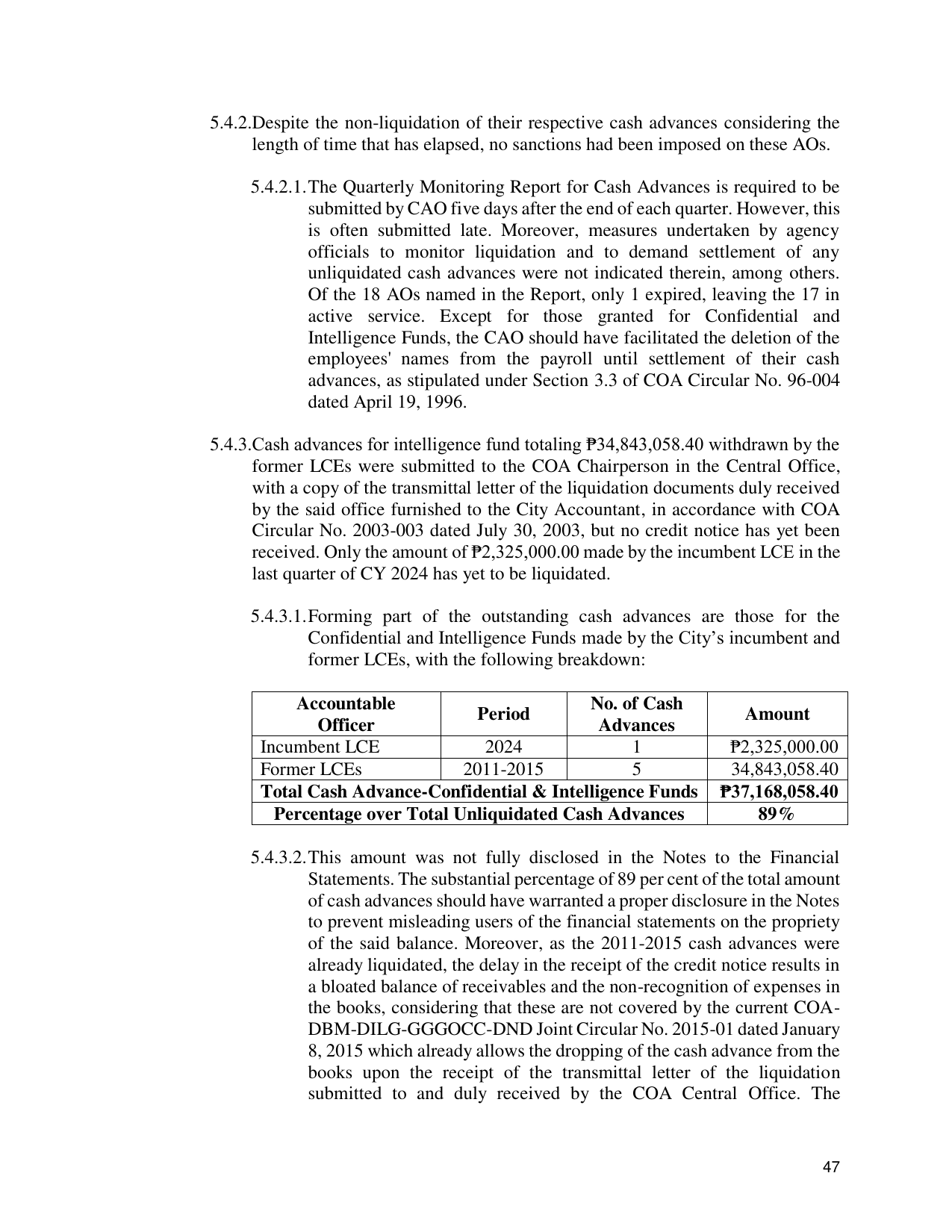

5.4.3.1. Forming part of the outstanding cash advances are those for the

Confidential and Intelligence Funds made by the City’s incumbent and

former LCEs, with the following breakdown:

Accountable No. of Cash

Period Amount

Officer Advances

Incumbent LCE 2024 1 ₱2,325,000.00

Former LCEs 2011-2015 5 34,843,058.40

Total Cash Advance-Confidential & Intelligence Funds ₱37,168,058.40

Percentage over Total Unliquidated Cash Advances 89%

5.4.3.2. This amount was not fully disclosed in the Notes to the Financial

Statements. The substantial percentage of 89 per cent of the total amount

of cash advances should have warranted a proper disclosure in the Notes

to prevent misleading users of the financial statements on the propriety

of the said balance. Moreover, as the 2011-2015 cash advances were

already liquidated, the delay in the receipt of the credit notice results in

a bloated balance of receivables and the non-recognition of expenses in

the books, considering that these are not covered by the current COA-

DBM-DILG-GGGOCC-DND Joint Circular No. 2015-01 dated January

8, 2015 which already allows the dropping of the cash advance from the

books upon the receipt of the transmittal letter of the liquidation

submitted to and duly received by the COA Central Office. The

47