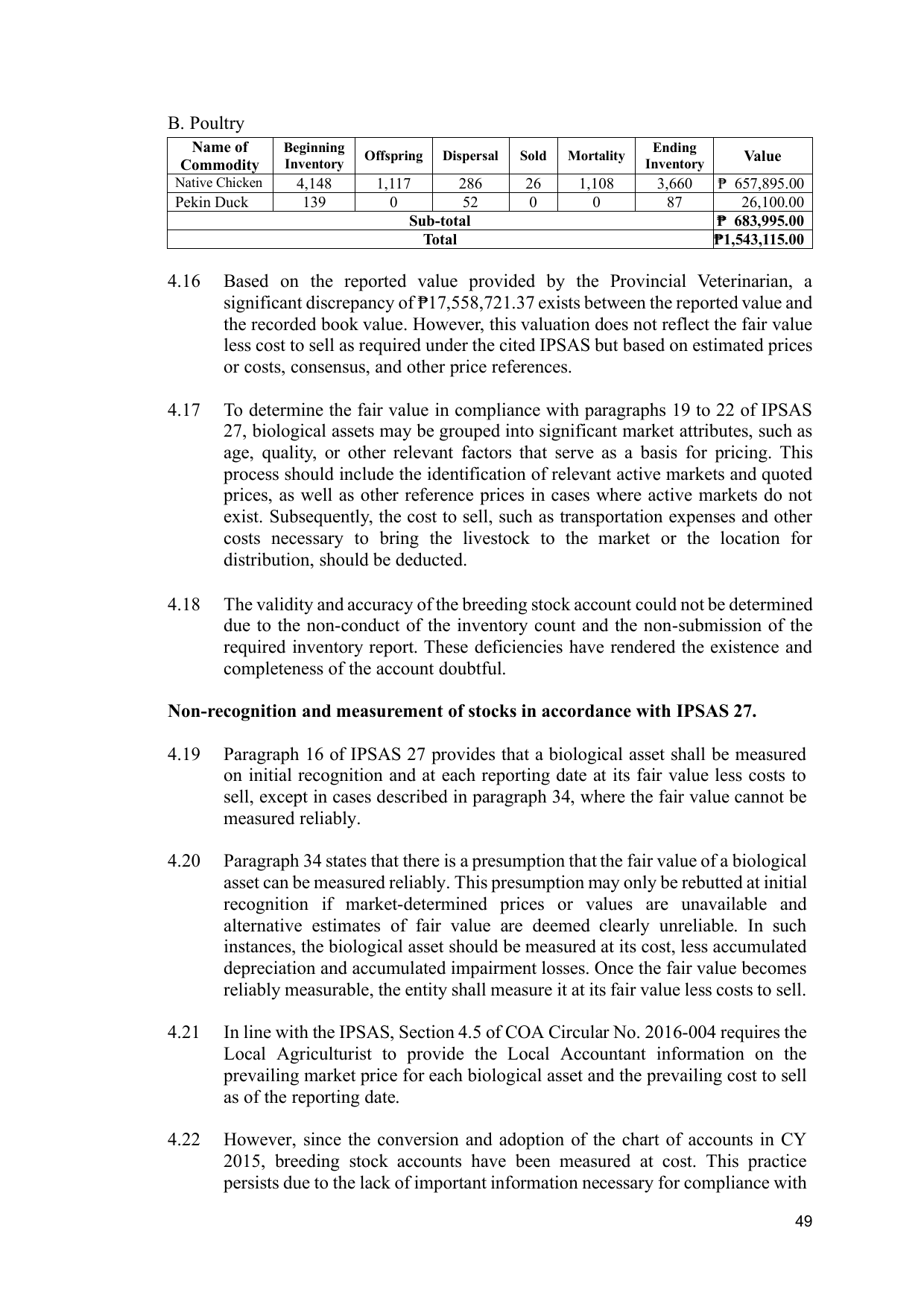

B. Poultry

Name of Beginning Ending

Inventory

Offspring Dispersal Sold Mortality

Inventory

Value

Commodity

Native Chicken 4,148 1,117 286 26 1,108 3,660 ₱ 657,895.00

Pekin Duck 139 0 52 0 0 87 26,100.00

Sub-total ₱ 683,995.00

Total ₱1,543,115.00

4.16 Based on the reported value provided by the Provincial Veterinarian, a

significant discrepancy of ₱17,558,721.37 exists between the reported value and

the recorded book value. However, this valuation does not reflect the fair value

less cost to sell as required under the cited IPSAS but based on estimated prices

or costs, consensus, and other price references.

4.17 To determine the fair value in compliance with paragraphs 19 to 22 of IPSAS

27, biological assets may be grouped into significant market attributes, such as

age, quality, or other relevant factors that serve as a basis for pricing. This

process should include the identification of relevant active markets and quoted

prices, as well as other reference prices in cases where active markets do not

exist. Subsequently, the cost to sell, such as transportation expenses and other

costs necessary to bring the livestock to the market or the location for

distribution, should be deducted.

4.18 The validity and accuracy of the breeding stock account could not be determined

due to the non-conduct of the inventory count and the non-submission of the

required inventory report. These deficiencies have rendered the existence and

completeness of the account doubtful.

Non-recognition and measurement of stocks in accordance with IPSAS 27.

4.19 Paragraph 16 of IPSAS 27 provides that a biological asset shall be measured

on initial recognition and at each reporting date at its fair value less costs to

sell, except in cases described in paragraph 34, where the fair value cannot be

measured reliably.

4.20 Paragraph 34 states that there is a presumption that the fair value of a biological

asset can be measured reliably. This presumption may only be rebutted at initial

recognition if market-determined prices or values are unavailable and

alternative estimates of fair value are deemed clearly unreliable. In such

instances, the biological asset should be measured at its cost, less accumulated

depreciation and accumulated impairment losses. Once the fair value becomes

reliably measurable, the entity shall measure it at its fair value less costs to sell.

4.21 In line with the IPSAS, Section 4.5 of COA Circular No. 2016-004 requires the

Local Agriculturist to provide the Local Accountant information on the

prevailing market price for each biological asset and the prevailing cost to sell

as of the reporting date.

4.22 However, since the conversion and adoption of the chart of accounts in CY

2015, breeding stock accounts have been measured at cost. This practice

persists due to the lack of important information necessary for compliance with

49