3.10 Budget information

The annual budget is prepared on a modified cash basis, that is, all planned costs

and income are presented in a single statement to determine the needs of the

Province. As a result of the adoption of the modified cash basis for budgeting

purposes, there are basis, timing, or entity differences that would require

reconciliation between the actual comparable amounts and the amounts presented

as a separate additional financial statement in the statement of comparison of

budget and actual amounts. Explanatory comments are provided in the notes to the

annual financial statements; first, the reasons for overall growth or decline in the

budget are stated, followed by details of overspending or underspending on line

items.

3.11 Significant judgments and sources of estimation uncertainty

Judgments

In the process of applying the LGU accounting policies, management has made

judgments that have the most significant effect on the amounts recognized in the

consolidated financial statements.

Useful lives and residual values

The useful lives and residual values of assets are assessed using the table provided

by the COA.

3.12 Financial instruments - financial risk management

Exposure to currency, commodity, interest rate, liquidity, and credit risks arises in

the normal course of the LGUs operations. This note presents information about its

exposure to each of the mentioned risks, its policies and processes for measuring

and managing risk, and the LGU’s management of capital. Further quantitative

disclosures are included throughout these financial statements. The fair values set

out below are a comparison by class of the carrying amounts and fair value of the

LGU’s financial instruments.

The fair value of the financial assets and liabilities is included at the amount at

which the instrument could be exchanged in a current transaction between willing

parties, other than in a forced sale or liquidation.

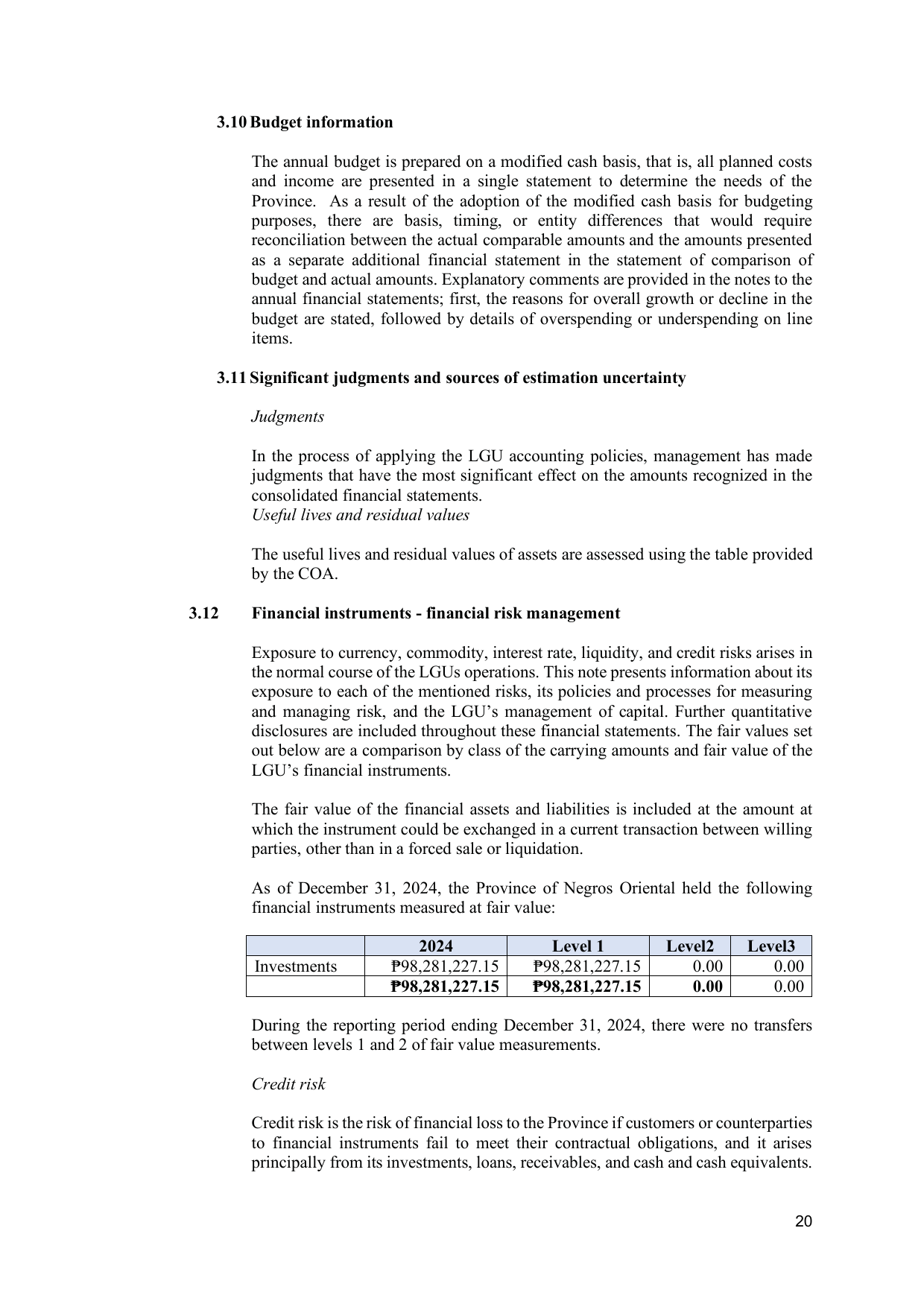

As of December 31, 2024, the Province of Negros Oriental held the following

financial instruments measured at fair value:

2024 Level 1 Level2 Level3

Investments ₱98,281,227.15 ₱98,281,227.15 0.00 0.00

₱98,281,227.15 ₱98,281,227.15 0.00 0.00

During the reporting period ending December 31, 2024, there were no transfers

between levels 1 and 2 of fair value measurements.

Credit risk

Credit risk is the risk of financial loss to the Province if customers or counterparties

to financial instruments fail to meet their contractual obligations, and it arises

principally from its investments, loans, receivables, and cash and cash equivalents.

20