GPB, ensuring that the proposed PPAs are properly charged to the GAD

Fund.

Delayed Remittance of Withheld Taxes

19. Taxes withheld from payments for purchases and compensation were not fully

remitted within the prescribed period specified in Item B.4 of the Bureau of

Internal Revenue (BIR) Revenue Memorandum Circular (RMC) No. 23-2012

dated February 14, 2012, which may hamper the government’s immediate use of

these funds for various programs and projects and may subject the withheld

amounts to penalties and surcharges for delayed remittances.

19.1 Paragraph B of BIR Revenue Memorandum Circular No. 23-2012 dated

February 14, 2012, provides, in substance, the responsibilities of government

officials and employees as withholding agents. Among these responsibilities are

the proper withholding of the correct amount of tax and the timely remittance

of the withheld taxes within the prescribed periods.

19.2 Paragraph C of the RMC outlines the applicable penalties for specific violations.

Failure to fulfil their responsibilities expose government officials or personnel

to the risk of incurring applicable interest and surcharges.

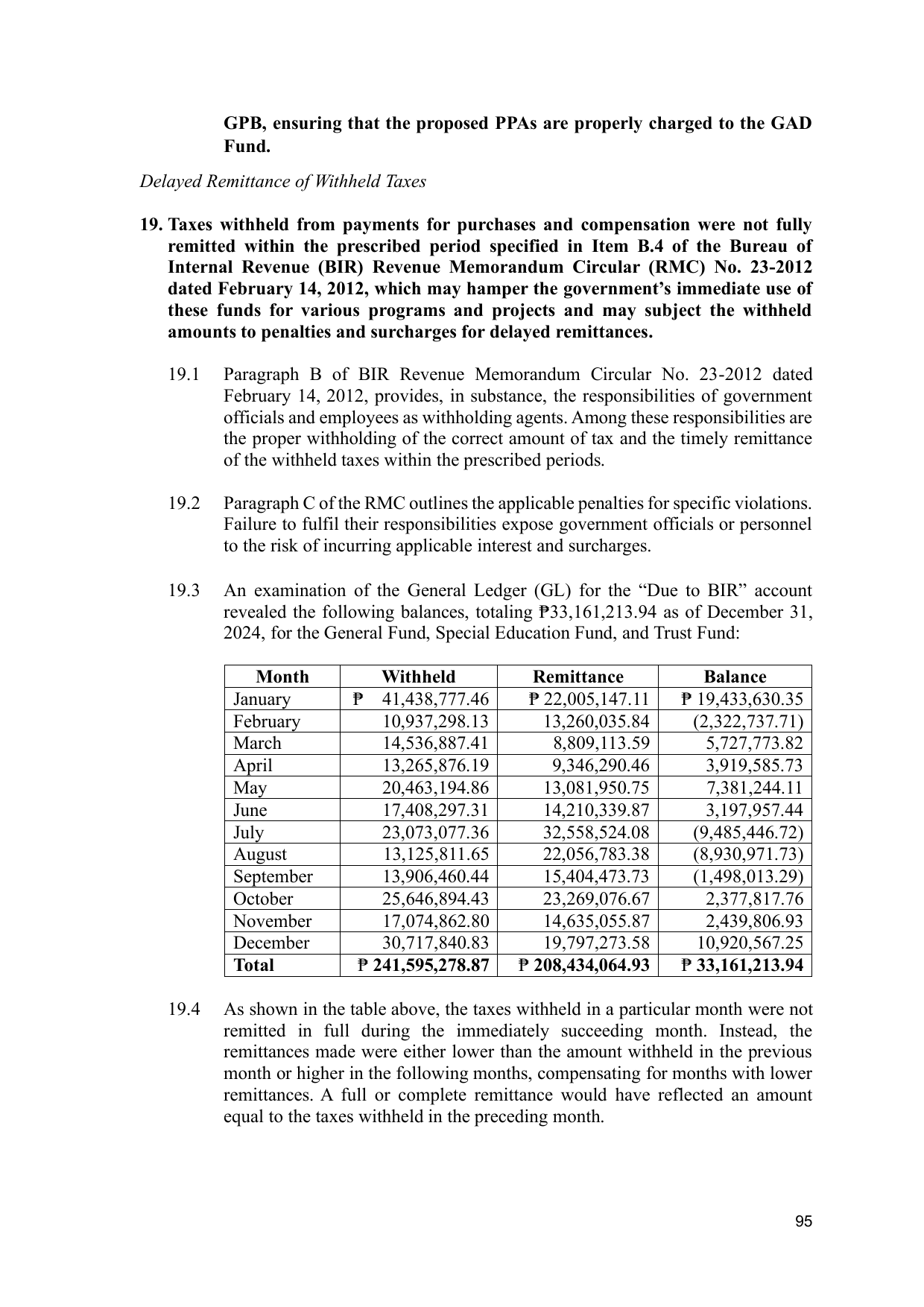

19.3 An examination of the General Ledger (GL) for the “Due to BIR” account

revealed the following balances, totaling ₱33,161,213.94 as of December 31,

2024, for the General Fund, Special Education Fund, and Trust Fund:

Month Withheld Remittance Balance

January ₱ 41,438,777.46 ₱ 22,005,147.11 ₱ 19,433,630.35

February 10,937,298.13 13,260,035.84 (2,322,737.71)

March 14,536,887.41 8,809,113.59 5,727,773.82

April 13,265,876.19 9,346,290.46 3,919,585.73

May 20,463,194.86 13,081,950.75 7,381,244.11

June 17,408,297.31 14,210,339.87 3,197,957.44

July 23,073,077.36 32,558,524.08 (9,485,446.72)

August 13,125,811.65 22,056,783.38 (8,930,971.73)

September 13,906,460.44 15,404,473.73 (1,498,013.29)

October 25,646,894.43 23,269,076.67 2,377,817.76

November 17,074,862.80 14,635,055.87 2,439,806.93

December 30,717,840.83 19,797,273.58 10,920,567.25

Total ₱ 241,595,278.87 ₱ 208,434,064.93 ₱ 33,161,213.94

19.4 As shown in the table above, the taxes withheld in a particular month were not

remitted in full during the immediately succeeding month. Instead, the

remittances made were either lower than the amount withheld in the previous

month or higher in the following months, compensating for months with lower

remittances. A full or complete remittance would have reflected an amount

equal to the taxes withheld in the preceding month.

95