APMT — Page 7 of 90

AGENCY ACTION PLAN and STATUS of IMPLEMENTATION RESULTS of COA VALIDATION

Agency Action Plan (for Partially Implemented

and Not Implemented Recommendations) Reason for Actual

Status of Partial/Delay/ Action Date Status of

Audit Action Plan/ Target Implementation

Ref. Audit Observations Person/ Implemen- Non- Taken/Action Follow Implemen- Remarks

Recommendations Remarks Department Implementati Implementation, Date

Responsible tation to be Taken Up tation

on Date if applicable

From To From To

strengthen internal

controls over the

Provincial

Government’s

biological assets.

These policies

include provisions

for ensuring the

timely flow of

relevant

accounting

information

concerning

biological assets

from the operating

units to the PaccO,

thereby enhancing

accuracy and

accountability for

succeeding years.

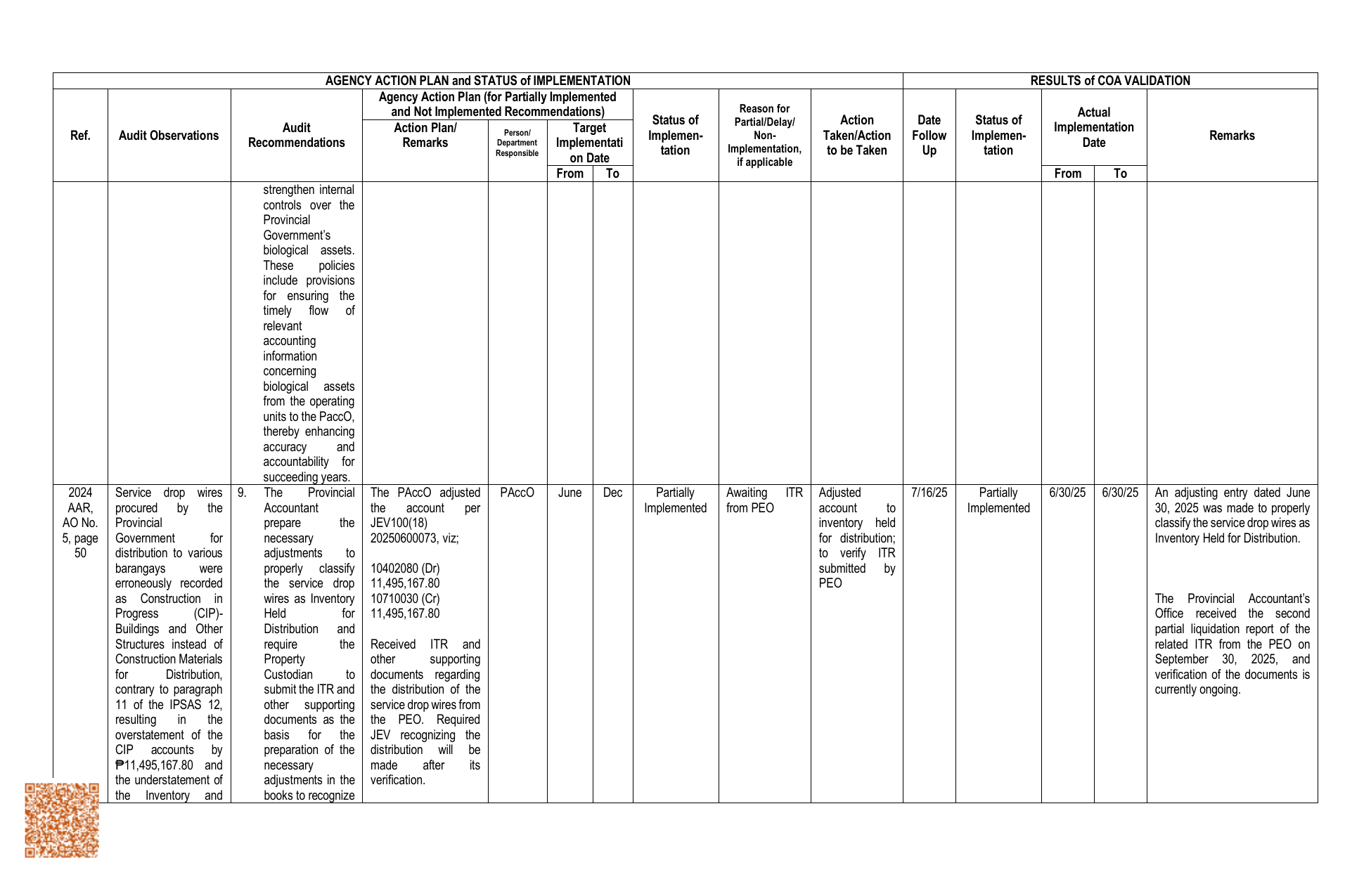

2024 Service drop wires 9. The Provincial The PAccO adjusted PAccO June Dec Partially Awaiting ITR Adjusted 7/16/25 Partially 6/30/25 6/30/25 An adjusting entry dated June

AAR, procured by the Accountant the account per Implemented from PEO account to Implemented 30, 2025 was made to properly

AO No. Provincial prepare the JEV100(18) inventory held classify the service drop wires as

5, page Government for necessary 20250600073, viz; for distribution; Inventory Held for Distribution.

50 distribution to various adjustments to to verify ITR

barangays were properly classify 10402080 (Dr) submitted by

erroneously recorded the service drop 11,495,167.80 PEO

as Construction in wires as Inventory 10710030 (Cr) The Provincial Accountant’s

Progress (CIP)- Held for 11,495,167.80 Office received the second

Buildings and Other Distribution and partial liquidation report of the

Structures instead of require the Received ITR and related ITR from the PEO on

Construction Materials Property other supporting September 30, 2025, and

for Distribution, Custodian to documents regarding verification of the documents is

contrary to paragraph submit the ITR and the distribution of the currently ongoing.

11 of the IPSAS 12, other supporting service drop wires from

resulting in the documents as the the PEO. Required

overstatement of the basis for the JEV recognizing the

CIP accounts by preparation of the distribution will be

₱11,495,167.80 and necessary made after its

the understatement of adjustments in the verification.

the Inventory and books to recognize