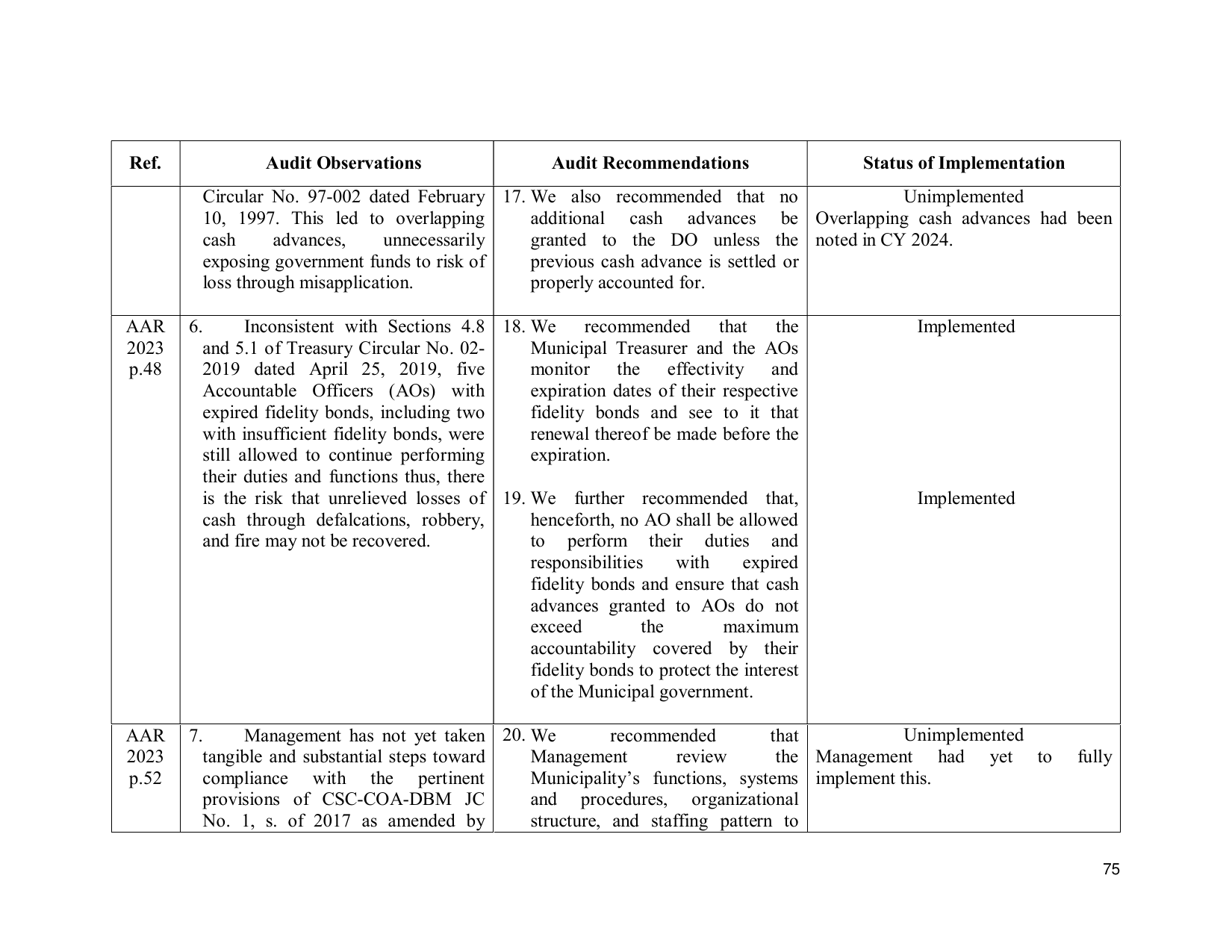

Ref. Audit Observations Audit Recommendations Status of Implementation

Circular No. 97-002 dated February 17. We also recommended that no Unimplemented

10, 1997. This led to overlapping additional cash advances be Overlapping cash advances had been

cash advances, unnecessarily granted to the DO unless the noted in CY 2024.

exposing government funds to risk of previous cash advance is settled or

loss through misapplication. properly accounted for.

AAR 6. Inconsistent with Sections 4.8 18. We recommended that the Implemented

2023 and 5.1 of Treasury Circular No. 02- Municipal Treasurer and the AOs

p.48 2019 dated April 25, 2019, five monitor the effectivity and

Accountable Officers (AOs) with expiration dates of their respective

expired fidelity bonds, including two fidelity bonds and see to it that

with insufficient fidelity bonds, were renewal thereof be made before the

still allowed to continue performing expiration.

their duties and functions thus, there

is the risk that unrelieved losses of 19. We further recommended that, Implemented

cash through defalcations, robbery, henceforth, no AO shall be allowed

and fire may not be recovered. to perform their duties and

responsibilities with expired

fidelity bonds and ensure that cash

advances granted to AOs do not

exceed the maximum

accountability covered by their

fidelity bonds to protect the interest

of the Municipal government.

AAR 7. Management has not yet taken 20. We recommended that Unimplemented

2023 tangible and substantial steps toward Management review the Management had yet to fully

p.52 compliance with the pertinent Municipality’s functions, systems implement this.

provisions of CSC-COA-DBM JC and procedures, organizational

No. 1, s. of 2017 as amended by structure, and staffing pattern to

75