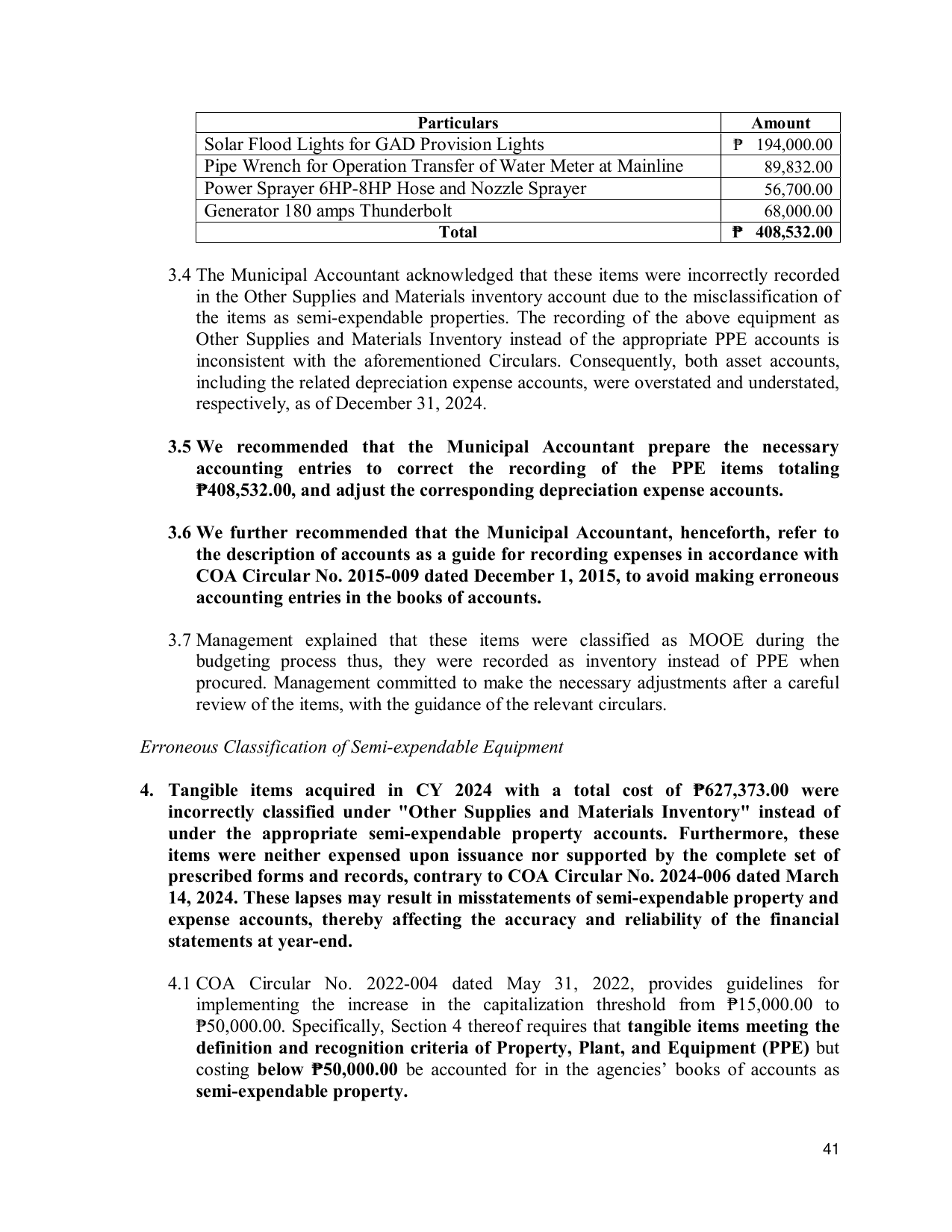

Particulars Amount

Solar Flood Lights for GAD Provision Lights ₱ 194,000.00

Pipe Wrench for Operation Transfer of Water Meter at Mainline 89,832.00

Power Sprayer 6HP-8HP Hose and Nozzle Sprayer 56,700.00

Generator 180 amps Thunderbolt 68,000.00

Total ₱ 408,532.00

3.4 The Municipal Accountant acknowledged that these items were incorrectly recorded

in the Other Supplies and Materials inventory account due to the misclassification of

the items as semi-expendable properties. The recording of the above equipment as

Other Supplies and Materials Inventory instead of the appropriate PPE accounts is

inconsistent with the aforementioned Circulars. Consequently, both asset accounts,

including the related depreciation expense accounts, were overstated and understated,

respectively, as of December 31, 2024.

3.5 We recommended that the Municipal Accountant prepare the necessary

accounting entries to correct the recording of the PPE items totaling

₱408,532.00, and adjust the corresponding depreciation expense accounts.

3.6 We further recommended that the Municipal Accountant, henceforth, refer to

the description of accounts as a guide for recording expenses in accordance with

COA Circular No. 2015-009 dated December 1, 2015, to avoid making erroneous

accounting entries in the books of accounts.

3.7 Management explained that these items were classified as MOOE during the

budgeting process thus, they were recorded as inventory instead of PPE when

procured. Management committed to make the necessary adjustments after a careful

review of the items, with the guidance of the relevant circulars.

Erroneous Classification of Semi-expendable Equipment

4. Tangible items acquired in CY 2024 with a total cost of ₱627,373.00 were

incorrectly classified under "Other Supplies and Materials Inventory" instead of

under the appropriate semi-expendable property accounts. Furthermore, these

items were neither expensed upon issuance nor supported by the complete set of

prescribed forms and records, contrary to COA Circular No. 2024-006 dated March

14, 2024. These lapses may result in misstatements of semi-expendable property and

expense accounts, thereby affecting the accuracy and reliability of the financial

statements at year-end.

4.1 COA Circular No. 2022-004 dated May 31, 2022, provides guidelines for

implementing the increase in the capitalization threshold from ₱15,000.00 to

₱50,000.00. Specifically, Section 4 thereof requires that tangible items meeting the

definition and recognition criteria of Property, Plant, and Equipment (PPE) but

costing below ₱50,000.00 be accounted for in the agencies’ books of accounts as

semi-expendable property.

41