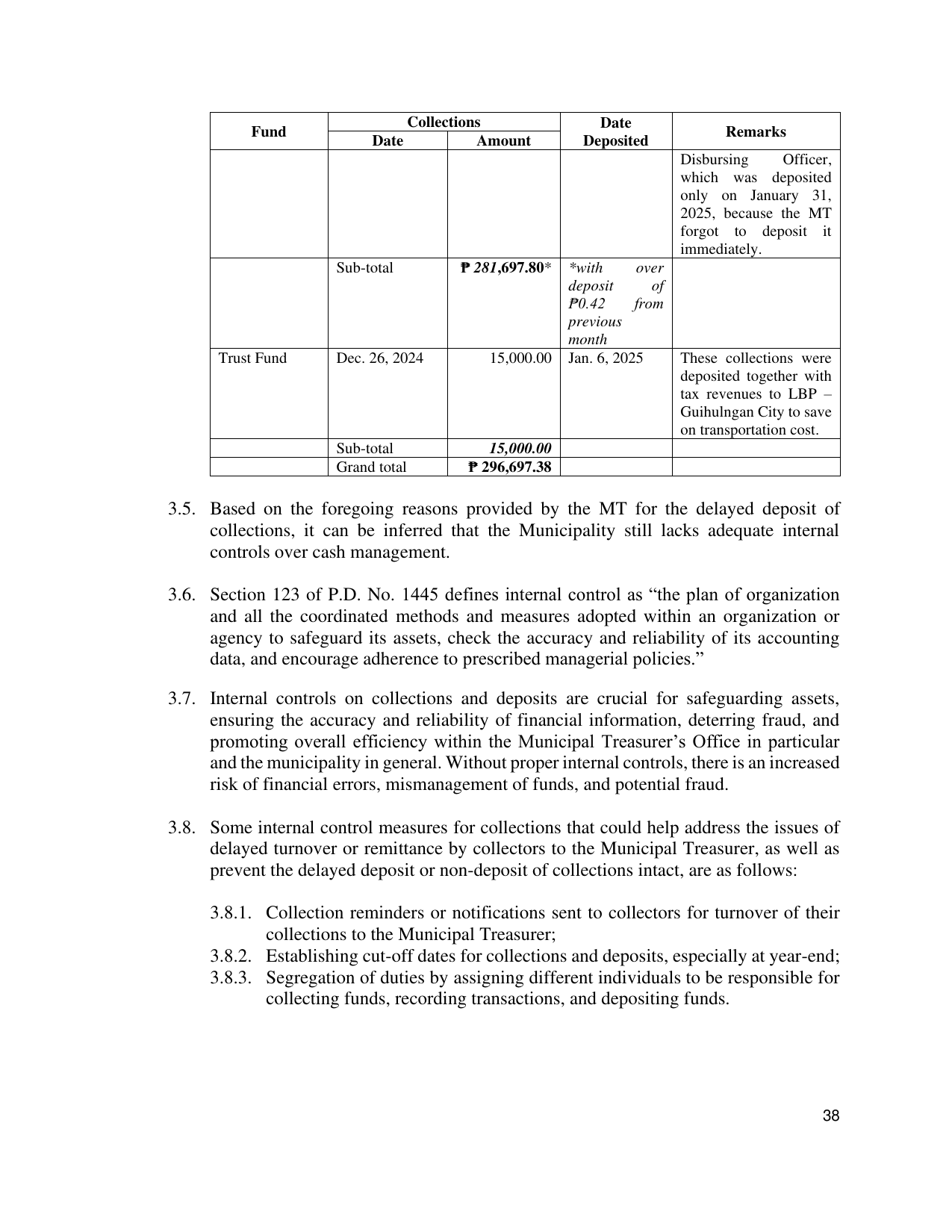

Collections Date

Fund Remarks

Date Amount Deposited

Disbursing Officer,

which was deposited

only on January 31,

2025, because the MT

forgot to deposit it

immediately.

Sub-total ₱ 281,697.80* *with over

deposit of

₱0.42 from

previous

month

Trust Fund Dec. 26, 2024 15,000.00 Jan. 6, 2025 These collections were

deposited together with

tax revenues to LBP –

Guihulngan City to save

on transportation cost.

Sub-total 15,000.00

Grand total ₱ 296,697.38

3.5. Based on the foregoing reasons provided by the MT for the delayed deposit of

collections, it can be inferred that the Municipality still lacks adequate internal

controls over cash management.

3.6. Section 123 of P.D. No. 1445 defines internal control as “the plan of organization

and all the coordinated methods and measures adopted within an organization or

agency to safeguard its assets, check the accuracy and reliability of its accounting

data, and encourage adherence to prescribed managerial policies.”

3.7. Internal controls on collections and deposits are crucial for safeguarding assets,

ensuring the accuracy and reliability of financial information, deterring fraud, and

promoting overall efficiency within the Municipal Treasurer’s Office in particular

and the municipality in general. Without proper internal controls, there is an increased

risk of financial errors, mismanagement of funds, and potential fraud.

3.8. Some internal control measures for collections that could help address the issues of

delayed turnover or remittance by collectors to the Municipal Treasurer, as well as

prevent the delayed deposit or non-deposit of collections intact, are as follows:

3.8.1. Collection reminders or notifications sent to collectors for turnover of their

collections to the Municipal Treasurer;

3.8.2. Establishing cut-off dates for collections and deposits, especially at year-end;

3.8.3. Segregation of duties by assigning different individuals to be responsible for

collecting funds, recording transactions, and depositing funds.

38