The Guaranty/Security Deposits Payable account consists of bidder’s bonds,

performance bonds, and warranty securities.

Customer’s Deposits Payable represents the temporary guaranty deposit required for

the installation of water service based on Municipal Tax Ordinance No. 1 series of 1992,

which is estimated to cover two month’s consumption. It shall be refunded only when the

concessionaires changes or when the service is permanently close, provided that all

outstanding accounts of the depositor, if any, shall first be deducted from the said guaranty.

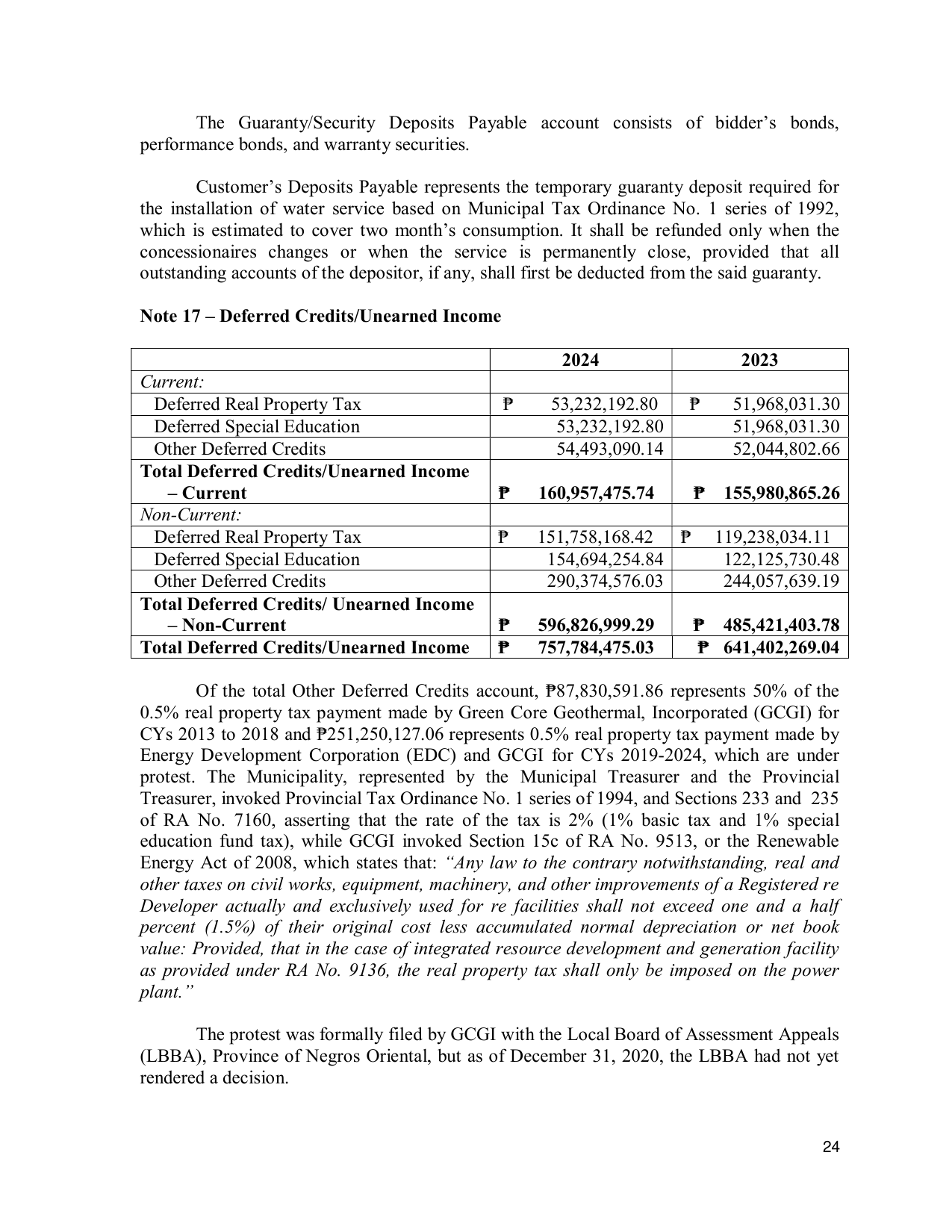

Note 17 – Deferred Credits/Unearned Income

2024 2023

Current:

Deferred Real Property Tax ₱ 53,232,192.80 ₱ 51,968,031.30

Deferred Special Education 53,232,192.80 51,968,031.30

Other Deferred Credits 54,493,090.14 52,044,802.66

Total Deferred Credits/Unearned Income

– Current ₱ 160,957,475.74 ₱ 155,980,865.26

Non-Current:

Deferred Real Property Tax ₱ 151,758,168.42 ₱ 119,238,034.11

Deferred Special Education 154,694,254.84 122,125,730.48

Other Deferred Credits 290,374,576.03 244,057,639.19

Total Deferred Credits/ Unearned Income

– Non-Current ₱ 596,826,999.29 ₱ 485,421,403.78

Total Deferred Credits/Unearned Income ₱ 757,784,475.03 ₱ 641,402,269.04

Of the total Other Deferred Credits account, ₱87,830,591.86 represents 50% of the

0.5% real property tax payment made by Green Core Geothermal, Incorporated (GCGI) for

CYs 2013 to 2018 and ₱251,250,127.06 represents 0.5% real property tax payment made by

Energy Development Corporation (EDC) and GCGI for CYs 2019-2024, which are under

protest. The Municipality, represented by the Municipal Treasurer and the Provincial

Treasurer, invoked Provincial Tax Ordinance No. 1 series of 1994, and Sections 233 and 235

of RA No. 7160, asserting that the rate of the tax is 2% (1% basic tax and 1% special

education fund tax), while GCGI invoked Section 15c of RA No. 9513, or the Renewable

Energy Act of 2008, which states that: “Any law to the contrary notwithstanding, real and

other taxes on civil works, equipment, machinery, and other improvements of a Registered re

Developer actually and exclusively used for re facilities shall not exceed one and a half

percent (1.5%) of their original cost less accumulated normal depreciation or net book

value: Provided, that in the case of integrated resource development and generation facility

as provided under RA No. 9136, the real property tax shall only be imposed on the power

plant.”

The protest was formally filed by GCGI with the Local Board of Assessment Appeals

(LBBA), Province of Negros Oriental, but as of December 31, 2020, the LBBA had not yet

rendered a decision.

24