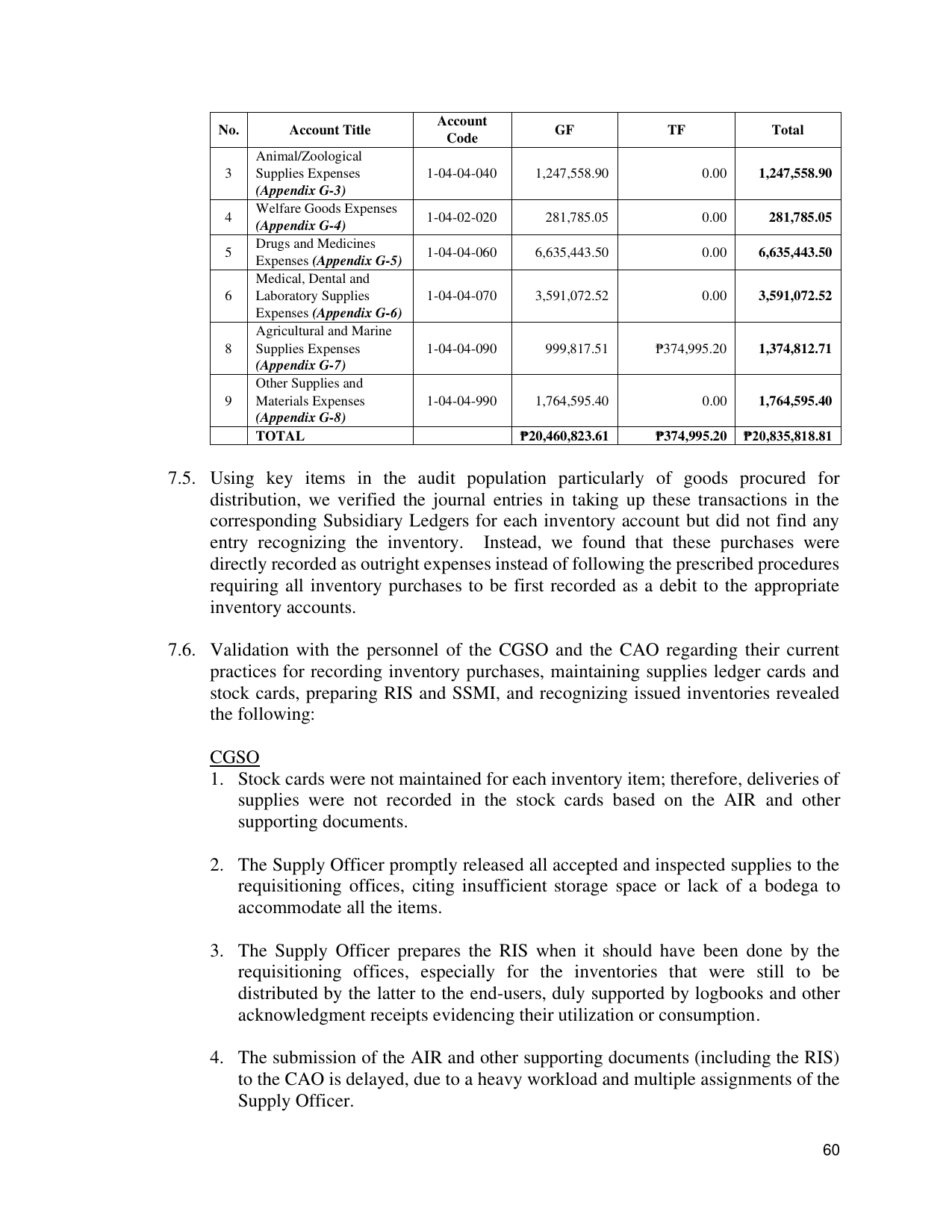

Account

No. Account Title GF TF Total

Code

Animal/Zoological

3 Supplies Expenses 1-04-04-040 1,247,558.90 0.00 1,247,558.90

(Appendix G-3)

Welfare Goods Expenses

4 1-04-02-020 281,785.05 0.00 281,785.05

(Appendix G-4)

Drugs and Medicines

5 1-04-04-060 6,635,443.50 0.00 6,635,443.50

Expenses (Appendix G-5)

Medical, Dental and

6 Laboratory Supplies 1-04-04-070 3,591,072.52 0.00 3,591,072.52

Expenses (Appendix G-6)

Agricultural and Marine

8 Supplies Expenses 1-04-04-090 999,817.51 ₱374,995.20 1,374,812.71

(Appendix G-7)

Other Supplies and

9 Materials Expenses 1-04-04-990 1,764,595.40 0.00 1,764,595.40

(Appendix G-8)

TOTAL ₱20,460,823.61 ₱374,995.20 ₱20,835,818.81

7.5. Using key items in the audit population particularly of goods procured for

distribution, we verified the journal entries in taking up these transactions in the

corresponding Subsidiary Ledgers for each inventory account but did not find any

entry recognizing the inventory. Instead, we found that these purchases were

directly recorded as outright expenses instead of following the prescribed procedures

requiring all inventory purchases to be first recorded as a debit to the appropriate

inventory accounts.

7.6. Validation with the personnel of the CGSO and the CAO regarding their current

practices for recording inventory purchases, maintaining supplies ledger cards and

stock cards, preparing RIS and SSMI, and recognizing issued inventories revealed

the following:

CGSO

1. Stock cards were not maintained for each inventory item; therefore, deliveries of

supplies were not recorded in the stock cards based on the AIR and other

supporting documents.

2. The Supply Officer promptly released all accepted and inspected supplies to the

requisitioning offices, citing insufficient storage space or lack of a bodega to

accommodate all the items.

3. The Supply Officer prepares the RIS when it should have been done by the

requisitioning offices, especially for the inventories that were still to be

distributed by the latter to the end-users, duly supported by logbooks and other

acknowledgment receipts evidencing their utilization or consumption.

4. The submission of the AIR and other supporting documents (including the RIS)

to the CAO is delayed, due to a heavy workload and multiple assignments of the

Supply Officer.

60