6.11. We recommended and the City Mayor agreed to direct the CGSO to fully

account for the fuel purchases based on valid supporting documents, assign a

specific person to prioritize the preparation of the liquidation reports, to the

extent possible, ensure the immediate submission of the utilization reports to the

CAO, and pinpoint responsibility for any fuel that cannot be accounted for.

Purchases of supplies and materials directly recorded as outright expenses - ₱20,835,818.81

7. Inventory procedures for the procurement of supplies and materials totaling

₱20,835,818.81 were not in accordance with Sections 114, 120, 121, and 122, Chapter

7 of the Manual on NGAS for LGUs, Volume I, resulting in an understatement of the

inventory and an overstatement of the City’s expense accounts, a breakdown of

internal controls in property and supply management, and an increased risk of

exposing unissued supplies to loss or misuse.

7.1. Section 114, Chapter 7 of the NGAS Manual for LGUs, Volume I provides the basic

accounting principles to be followed in recording the procured supplies and materials,

viz.:

Sec. 114. Perpetual Inventory Method. Purchase of supplies and materials

for stock, regardless of whether or not they are consumed within the

accounting period, shall be recorded as inventory following the perpetual

inventory method. Under the perpetual inventory method, an inventory

control account is maintained in the General Ledger on a current basis. In

addition, detailed inventory records are maintained for each inventory item.

Regular purchases shall be coursed thru the inventory account and issuances

thereof shall be recorded as they take place, except those purchased out of the

petty cash fund which shall be for immediate use and for stock in which case

shall be charged immediately to the appropriate expense accounts.

7.2. Moreover, Sections 120 and 121 of the same Manual provide the guidelines for

recording the delivered supplies and their issuances in the books of the accounts

(please see paragraphs 3.1 for the exact provisions).

7.3. Finally, Section 122 clearly outlines the general procedures of the inventory system

and identifies the responsible person or unit.

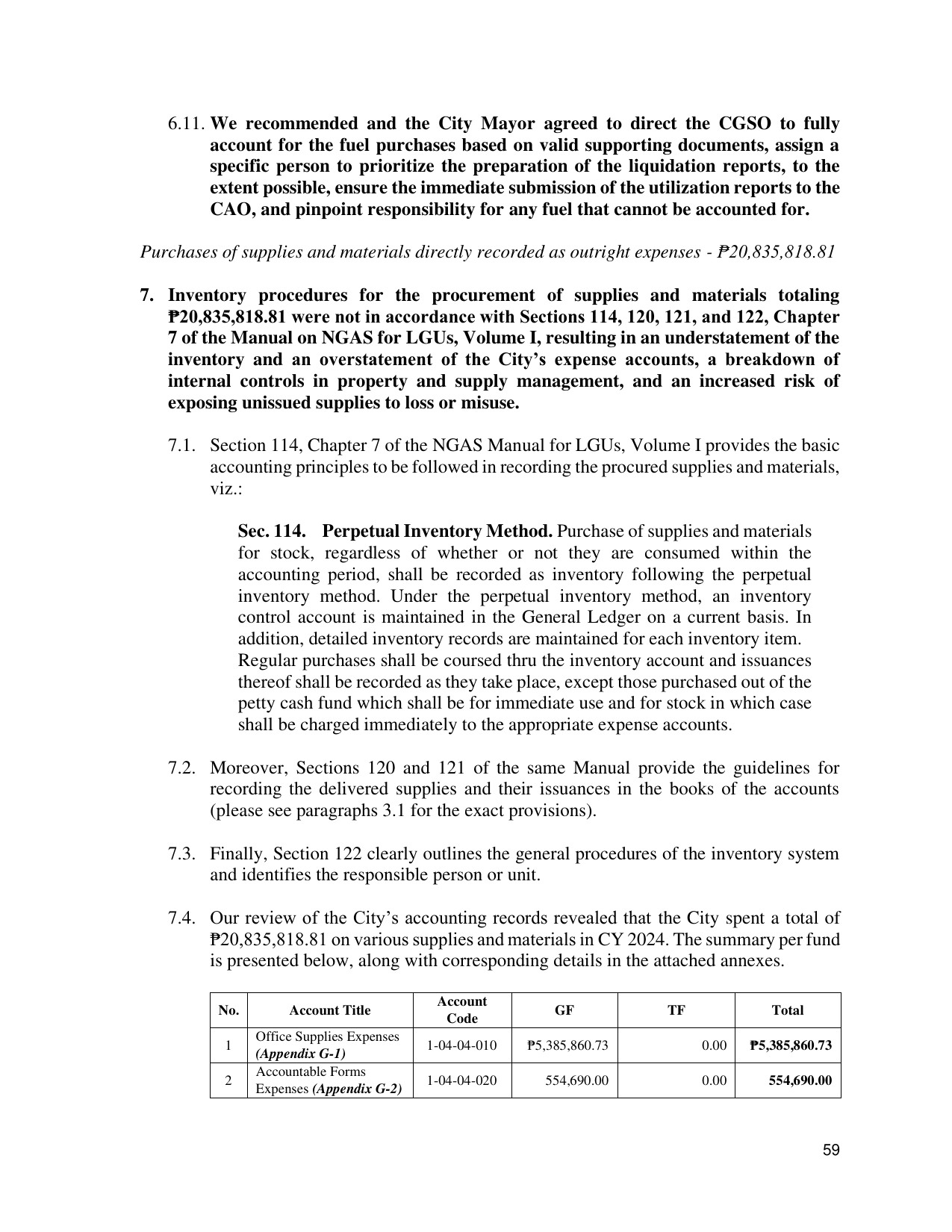

7.4. Our review of the City’s accounting records revealed that the City spent a total of

₱20,835,818.81 on various supplies and materials in CY 2024. The summary per fund

is presented below, along with corresponding details in the attached annexes.

Account

No. Account Title GF TF Total

Code

Office Supplies Expenses

1 1-04-04-010 ₱5,385,860.73 0.00 ₱5,385,860.73

(Appendix G-1)

Accountable Forms

2 1-04-04-020 554,690.00 0.00 554,690.00

Expenses (Appendix G-2)

59