Amount Number of

per Project Date of Years Since

Project Cost

Subsidiary Status Completion Completion

Ledger Date

Extension/Completion of BHS at

3 998,245.80 998,245.80 Completed 03/03/20 4.83

Barangay Pal-ew

SUB-TOTAL - CIP - BUILDINGS AND

14,281,247.86

OTHER STRUCTURES

II. CIP - INFRASTRUCTURE ASSETS (1-07-10-020)

Cluster II Concreting Brgy. Sto. Niño

Road (intermittent section) and

4 15,985,138.20 15,985,138.20 Completed 07/18/14 10.46

Concreting of Sitio Inolocan, Bahian

Farm-to-Market Road (FMR)

Cluster I Concreting of Bolon Pal-ew

5 16,947,545.72 16,947,545.72 Completed 12/14/14 10.05

Road (Intermittent)

Cluster II - Concreting of Barangay Road

6 3,990,100.64 3,990,100.64 Completed 12/03/14 10.08

at Barangay San Isidro

Cluster A FMR Projects (FMR Carsadang

7 2,910,700.70 2,910,700.70 Completed 08/04/15 9.42

Daan, Brgy. Luca), Tanjay City

Road Rehabilitation/Regravelling of Sitio

8 1,235,456.20 1,235,456.20 Completed 03/10/16 8.82

Banlas, Azagra

Cluster D II River Control at Barangay I

9 2,988,383.29 2,988,383.09 Completed 02/20/14 10.87

(₱3M), Tanjay City

Construction of Flood Control Dike

10 7,999,303.54 7,999,303.54 Completed 10/27/20 4.18

along Tanjay River

Construction of Flood Control Dikes along

11 7,997,429.35 7,997,429.35 Completed 01/09/20 4.98

Tanjay River, San Isidro, Tanjay City

12 Drainage Canal Project, Tanjay City 9,990,346.89 9,990,346.89 Completed 04/29/24 0.67

Single-storey Science Laboratory

13 Building at Tanjay National High 1,270,829.57 1,270,829.57 Completed 03/27/09 15.78

School, Opao ***

Construction of Evacuation Center at Sitio

14 1,796,299.15 1,796,299.15 Completed 03/03/21 3.83

Ling-ab, San Miguel, Tanjay City ***

SUB-TOTAL - CIP - INFRASTRUCTURE

73,111,533.25

ASSETS

TOTAL-CIP ₱87,392,781.11

*** Item Nos. 13 and 14, totaling ₱3,067,128.72, were erroneously recorded as CIP-Infrastructure Assets instead of CIP-Buildings and

Other Structures

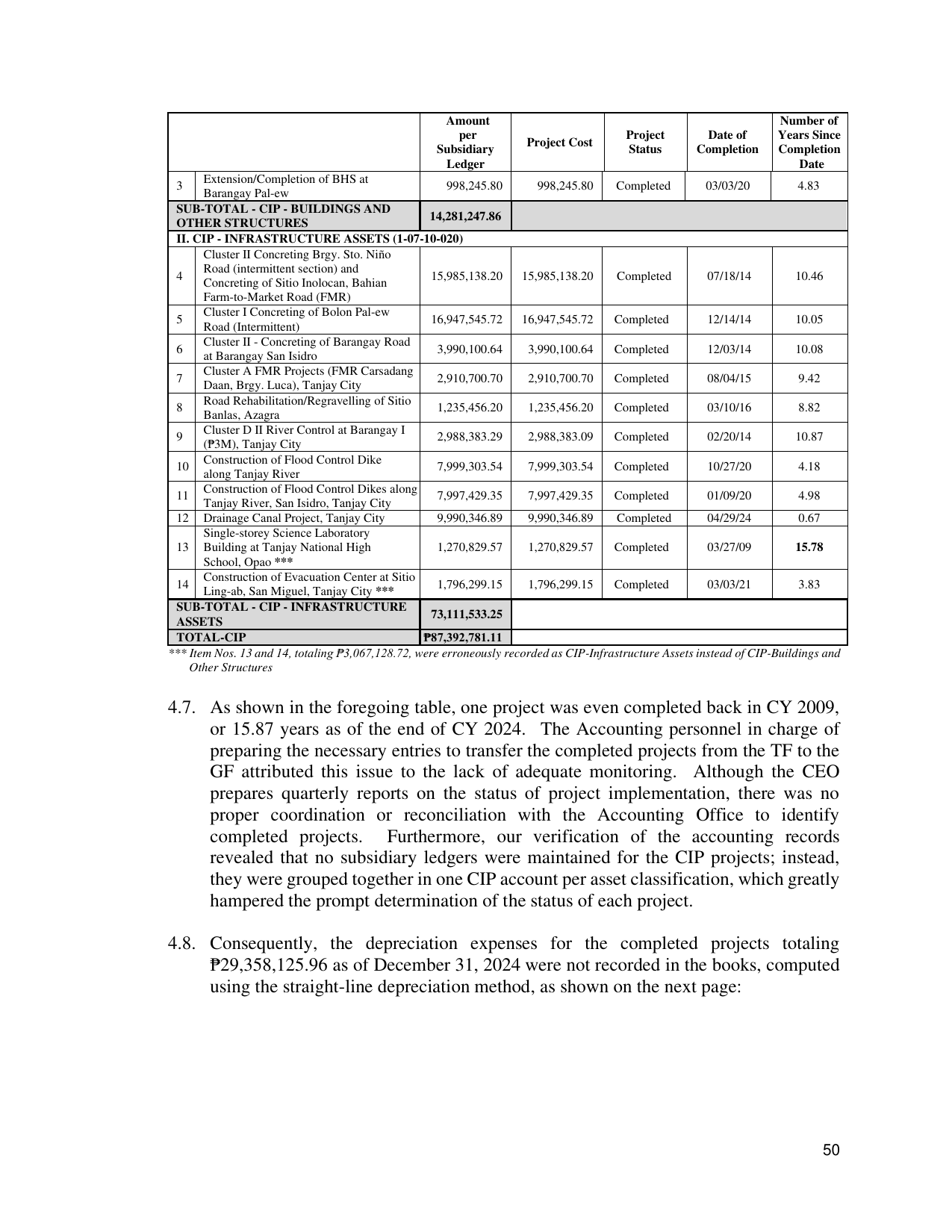

4.7. As shown in the foregoing table, one project was even completed back in CY 2009,

or 15.87 years as of the end of CY 2024. The Accounting personnel in charge of

preparing the necessary entries to transfer the completed projects from the TF to the

GF attributed this issue to the lack of adequate monitoring. Although the CEO

prepares quarterly reports on the status of project implementation, there was no

proper coordination or reconciliation with the Accounting Office to identify

completed projects. Furthermore, our verification of the accounting records

revealed that no subsidiary ledgers were maintained for the CIP projects; instead,

they were grouped together in one CIP account per asset classification, which greatly

hampered the prompt determination of the status of each project.

4.8. Consequently, the depreciation expenses for the completed projects totaling

₱29,358,125.96 as of December 31, 2024 were not recorded in the books, computed

using the straight-line depreciation method, as shown on the next page:

50